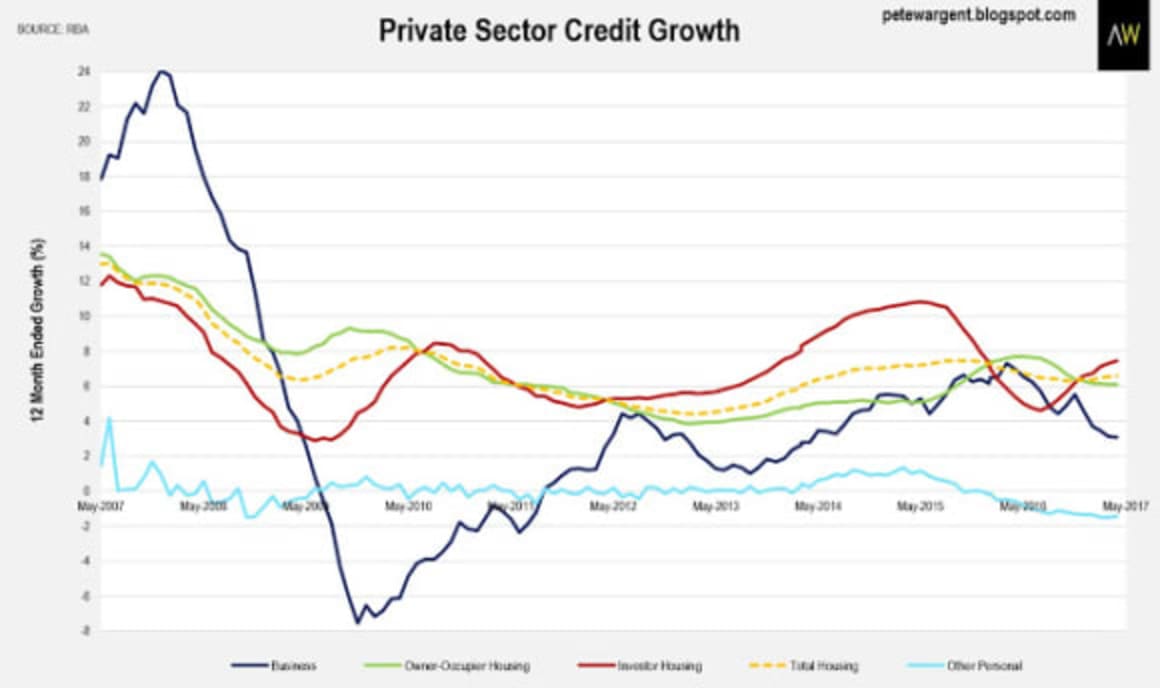

Drilling into the components of credit growth, housing credit had a stronger month, meaning that the annual rate of housing credit growth has continued to pick up speed from 6.32 per cent in November to 6.59 per cent in May.

Investor credit grew by 7.5 per cent over the year, but the trajectory up growth looks to be calming as banks jack up investment loan rates to encourage more owner-occupier loans.

Despite being inherently 'riskier', at least on a historical basis, business credit growth is considered by many to be vital.

However, stock exchange (ASX) market data records three consecutive months of strong aggregates in initial and secondary capital raisings totalling more than $12.5 billion, showing that business lending is far from the be all and end all for investment.

Business surveys also saw conditions hit multi-year highs early in 2017, while job surveys point to a broad-based improvement in hiring.

In other words, you can't just look at total outstanding business credit increasing by 3.1 per cent over the year and dismiss growth as weak.

Since July 2015 the purpose of some $53 billion of loans has been switched from investment to owner-occupier, following the introduction of an interest rate differential.

Thus, investor credit may be slowing, but the way the figures dovetail these days, the lines between what is an investment loan and what isn't seem to be increasingly blurred.

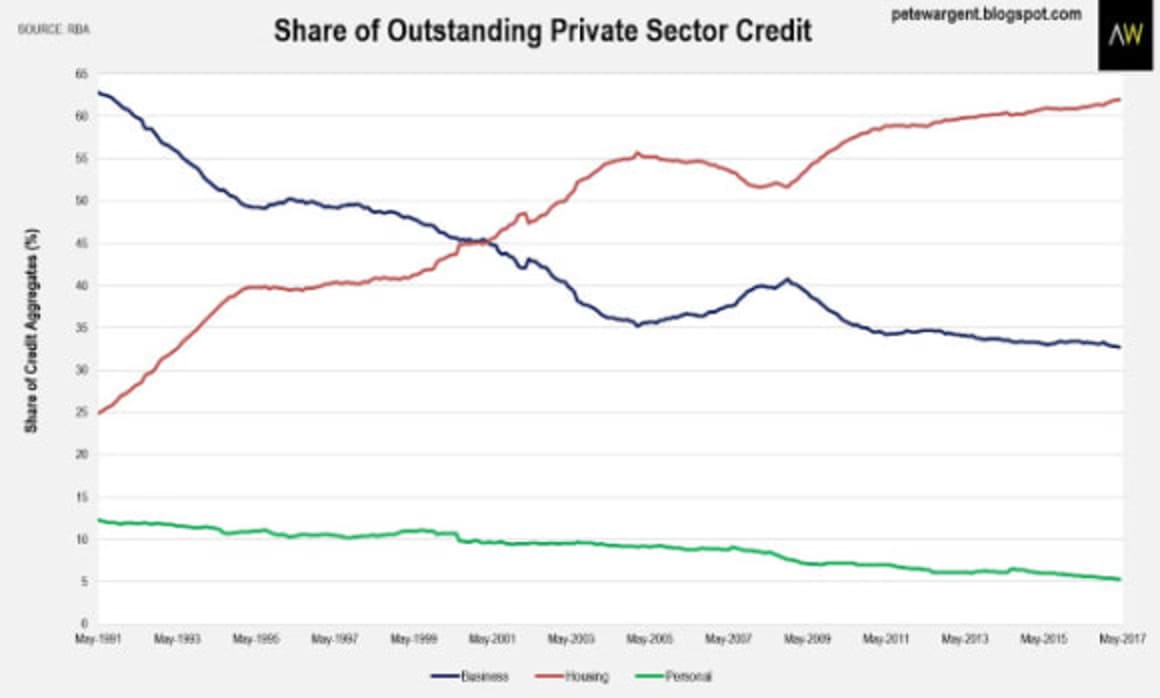

In any event, reported as a total housing now accounts for a record 62 per cent of outstanding credit.

Finally, and not too surprisingly, through netting off the results we can see that non-bank lending has picked up some of the slack to grow by a faster pace in May.

Total housing lending now sits at some $1.67 trillion.