High LVR loans have been declining for years: Pete Wargent

60 Minutes was an interesting talking point this week, wherein some American geezer claimed that he "could" have got a 95 per cent mortgage using a "fake income" by pretending to be a "gay couple".

OK. Given that he didn't actually get a mortgage written, it is a little perturbing how often people choose to believe what random punters say in preference to the actual data, but such is the nature of confirmation bias.

OK. Given that he didn't actually get a mortgage written, it is a little perturbing how often people choose to believe what random punters say in preference to the actual data, but such is the nature of confirmation bias.

Household debt is high, no doubt, and some lending has been reckless, particularly in mining towns, but by the same token not everything that is claimed on the internet or elsewhere is true.

For example, some years ago bearish commentators got sucked in to believing erroneous figures which claimed that an incredibly high percentage of lending was 100 per ent mortgages.

Of course, the data sources quoted advertised loans rather than actual loans written, a rookie error that surely wouldn't pass the sniff test.

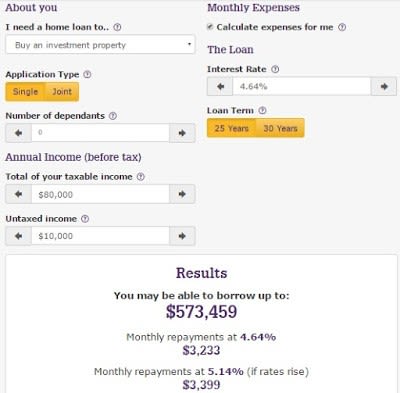

Another favourite trick is to tap a few notional numbers into a mortgage calculator and use this as "evidence" of irresponsible lending, conveniently neglecting to mention the key words "may be able to borrow". Clickbait ahoy!

It's one of the reasons I write blogs - not to get a readership, mainly just so I can stop annoying my missus by regurgitaing every blasted "fact" that I read in the media and on the internet.

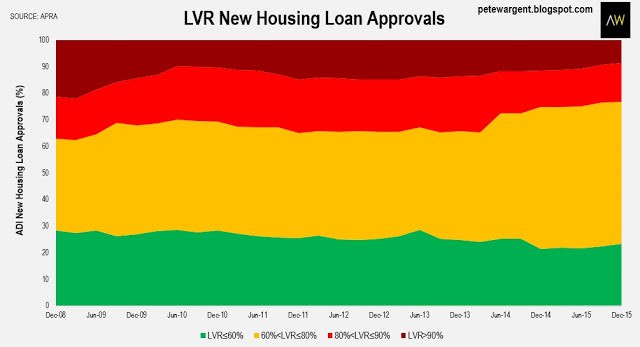

APRA exposures data

APRA exposures data

Back in the real world APRA released its latest ADI Q4 2015 property exposures data today, which showed that the share of new loans whereby lenders extended a 90 per cent or more loan-to-valuation ratio (LVR) has continued its long and steady decline from more than 18 per cent in the March 2008 quarter to under 10 per cent in the December 2015 quarter.

The share of loans whereby an 80 to 90 per cent LVR loan was advanced has also declined significantly over the last eight years from 20 per cent to only 14 per cent, meaning that the overwhelming majority of loans see a deposit of 20 per cent or more used.

I'll just clarify that.

In aggregate high LVR lending has been in decline for years, while low-doc loans and other non-standard now loans represent just a small and rapidly declining fraction of new loans and total residential mortgage market exposures.

In aggregate high LVR lending has been in decline for years, while low-doc loans and other non-standard now loans represent just a small and rapidly declining fraction of new loans and total residential mortgage market exposures.

Within the "big four" major banks 90 per cent plus LVR loans have fallen even more sharply from 21.6 per cent in 2009 to just 9.1 per cent, while 80 to 90 per cent LVR loans have declined from 22 per cent in 2011 to only 14.2 per cent.

Lending shifts to homebuyers

If there is anything suspicious in the APRA figures related to lending standards, I believe it is in the incredibly smooth transition from investment loans to owner-occupier loans.

If there is anything suspicious in the APRA figures related to lending standards, I believe it is in the incredibly smooth transition from investment loans to owner-occupier loans.

The market has barely skipped a beat in recording remarkably similar headline quarterly data while the percentage share of loans conveniently swings from investors to homebuyers.

Draw your own conclusions from that, but I'd hazard that some of these homebuyers may well be would-be investors sneakily veiled behind a Scooby-Doo mask.

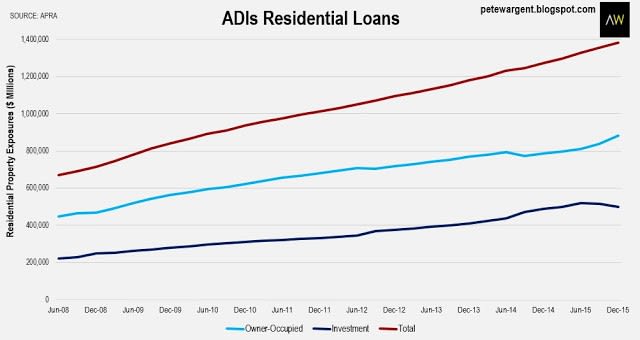

The 60 Minutes segment claimed that household debt is "exploding", and indeed the above chart shows that the total stock of outstanding credit has more than doubled since 2008.

However, the aggregate of outstanding household debt nearly always rises in an inflationary economy with rising household incomes and a strong population growth.

The truth is that after accounting for record high mortgage buffers and offset balances, the figures show that the household debt to income ratio is unchanged in Australia since 2008. Australia has a unique mechanism whereby loan repayments often continue at the same level when interest rates fall, as they have been since 2011.

60 Minutes also claimed that "half" of all loans are interest only.

The true figure as revealed in APRA's figures today is 39 per cent - still too high for comfort, granted, but this mostly reflects tax strategy rather than that people "can't afford to pay the debt back", and the interest-only loans figure should theoretically now decline following the crackdown on investor lending.

The truth according to the Reserve Bank of Australia (RBA) research is that on average homeowners are miles ahead on home loan repayments, by fully two years which is an unprecedented margin.

The 60 Minutes segment claimed that household debt is "exploding", and indeed the above chart shows that the total stock of outstanding credit has more than doubled since 2008.

However, the aggregate of outstanding household debt nearly always rises in an inflationary economy with rising household incomes and a strong population growth.

The truth is that after accounting for record high mortgage buffers and offset balances, the figures show that the household debt to income ratio is unchanged in Australia since 2008. Australia has a unique mechanism whereby loan repayments often continue at the same level when interest rates fall, as they have been since 2011.

60 Minutes also claimed that "half" of all loans are interest only.

The true figure as revealed in APRA's figures today is 39 per cent - still too high for comfort, granted, but this mostly reflects tax strategy rather than that people "can't afford to pay the debt back", and the interest-only loans figure should theoretically now decline following the crackdown on investor lending.

The truth according to the Reserve Bank of Australia (RBA) research is that on average homeowners are miles ahead on home loan repayments, by fully two years which is an unprecedented margin.

PETE WARGENT is the co-founder of AllenWargent property buyers (London, Sydney) and a best-selling author and blogger.

His latest book is Four Green Houses and a Red Hotel.

Pete Wargent

Pete Wargent is the co-founder of BuyersBuyers.com.au, offering affordable homebuying assistance to all Australians, and a best-selling author and blogger.