People seem to love the idea of "macro-prudential" measures.

It all sounds new and rather exciting, but in truth the term simply refers to financial regulation and approaches to managing systemic risks.

In respect of the housing market, the more popular ideas tend to include caps on loan-to-value ratios or restrictions on the level of debt that can be taken on by a borrower expressed as a multiple of income.

The Reserve Bank of New Zealand (RBNZ) has taken the approach of limiting lending to investors in Auckland, while investor loans will attract additional capital charges.

While such a targeted approach has seemed unlikely to date in Australia, lenders do already use similar methods to weed out high-risk loans, for example through restrictions on lending in mining towns, or on certain property types which are perceived to be of higher risk.

The Reserve Bank of Australia (RBA) has announced on multiple occasions that it is working with APRA in order to monitor lending standards, with APRA already having indicated an advisory 10 per cent cap on the growth of investment mortgage lending books.

Some banks are now insisting on 20 per cent deposits for investment loans. Others are tweaking borrowing rates, and others still have banned mortgage lending against property investments in self-managed superannuation funds (SMSFs).

Eventually these measures will begin to take hold of Australia's property markets, even if through perception alone.

whether or not more robust measures are taken to target specifically the rampant

Sydney market remains to be seen.

Let's take a look in three parts at the termination of the last

Sydney housing market boom in 2003/4 to see what we can learn.

1 - The "double tap"

Just as has been the case lately in this cycle, APRA began to discuss privately and publicly its concerns with the

Sydney housing market through 2003.

The regulator also took additional steps to collect data on mortgage lenders in order to identify the outliers, and held discussions with boards in order to seek assurance that prudent lending standards were being maintained.

This alone did not have the desired effect, and APRA consequently ramped up capital requirements and adjustments to mortgage insurance in order to moderate the market.

Arguably, however, a bigger factor in snapping off the

Sydney boom of just over a decade ago was the "double tap" on the brakes applied by the Reserve Bank, hiking rates from 4.75 per cent to 5.25 per cent through two rapid-fire tightening shots in November and December 2003.

Click to enlarge all charts

Given that Sydney dwelling price growth was all but cooked within the next quarter, this was arguably the most important factor, with the standard variable mortgage rate (SVR) thereafter remaining above 7 per cent all the way through until the financial crisis.

One troubling matter for the regulator this time around is that the odds of standard variable rates heading to 7 per cent again any time soon are nil, while new borrowers are able to fix borrowing rates at levels close to 4 per cent.

Futures markets are pricing an inverted yield curve for the remainder of this calendar year, and no rate hikes are priced for 2016 either, with the cash rate expected to remain at historic lows for at least the next 18 months.

Ergo, higher lending rates will not be the dampener.

Part 2 - Supply and underlying demand

Another factor which will be different through this

Sydney cycle is interstate migration.

In the year to September 2003, nearly 33,000 persons fled New South Wales for pastures new.

As you can see from my chart below, the mirror image movement in the line denoting Queensland in 2003 shows you that they were heading for a cheaper lifestyle in the Sunshine State.

However, interstate migration is not going to be a factor to slow the Sydney market in 2015.

In fact, interstate migration from New South Wales has fallen to its lowest level on record, and is set to decline yet further in the months ahead as Sydneysiders stay put for the superior employment prospects.

This is putting intense pressure on the Sydney property market, its rail, roads, public transport and infrastructure.

The below chart says it all. We are constructing far fewer houses than in decades gone by with the supply of shovel-ready land in Sydney falling to almost zero, but population growth in New South Wales has exploded higher.

My

chart packs have shown that rolling annual apartment approvals have ramped up to around 27,000 in Greater

Sydney, which is a start, but is hardly going to be enough in itself to pull up the property boom.

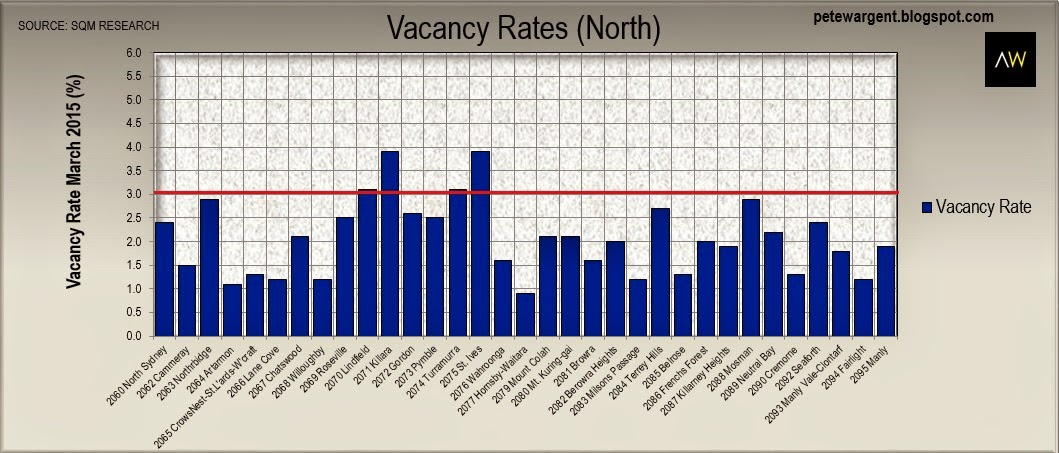

The Real Estate Institute of New South Wales (

REINSW) figures showed that at the end of the 2003/4 property boom

Sydney had a vacancy rate of 4.4 per cent, and 5.3 per cent on the outer.

If a property market "in equilibrium" is said to have a vacancy rate of 3 per cent, then

Sydney has got some building to do before we get back to that level, at least in the suburbs I visit, which are largely close to the city.

A handful of urban precincts are starting to become "well supplied", particularly to the north of the famous coat-hanger, but as I've shown here previously, the new supply is predominantly of the high rise unit variety.

With population growth in New South Wales tracking at above 105,000 per annum, there is a huge and growing demand for property in the harbour city.

Part 3 - The pipeline

One final point is that there is an enormous volume of pent-up buyers in the pipeline already, with record loan volumes written prior to the newly-announced lending measures.

In March, there were $5.9 billion of investor loans written in NSW, the highest figure ever recorded in Australia.

The clincher for mine, though, is that now this has become by no means an investor boom alone - owner-occupiers are piling into the market too, for fear of missing out.

Rolling annual lending to owner-occupiers in New South Wales has leapt to its highest ever level at more than $70 billion...and rising fast.

I note that some commentators have called "fading demand" in Sydney based on transaction volumes. I can see why you might think that if you haven't actually been here lately, or attended any viewings, or auctions, but this is to be wrong-footed by the data.

The principal reason for the diminished number of transactions is that vendors have held back in anticipation of higher prices.

The level of stock on market in Sydney is almost unthinkably low at the present time, and until this changes the number of buyers will continue to massively outweigh available stock, and prices will continue to rise, confounding the critics.

If you stop to do the numbers, you will see what I mean. In March 2015 $12.5 billion of mortgage finance was written in the state (as compared to less than $7.5 billion in March 2013). And there is hardly anything listed for sale; at least not for very long.

And this is before we begin to account for the impact of foreign capital, which every single auction I have attended this year leads me to believe is material, if not game-changing.

I have no doubt that macro-prudential measures will serve to slow the market eventually - and there may be many more tools deployed that we have not been made aware of - but not before

Sydney's median house price has been pushed up towards $1 million and investors have bid gross apartment yields all the way down into the mid 3 per cent range.