Next three RBA meetings are live for a possible rate cut: NAB

The next three RBA meetings are clearly live for a rate cut, says the NAB's ALAN OSTER.

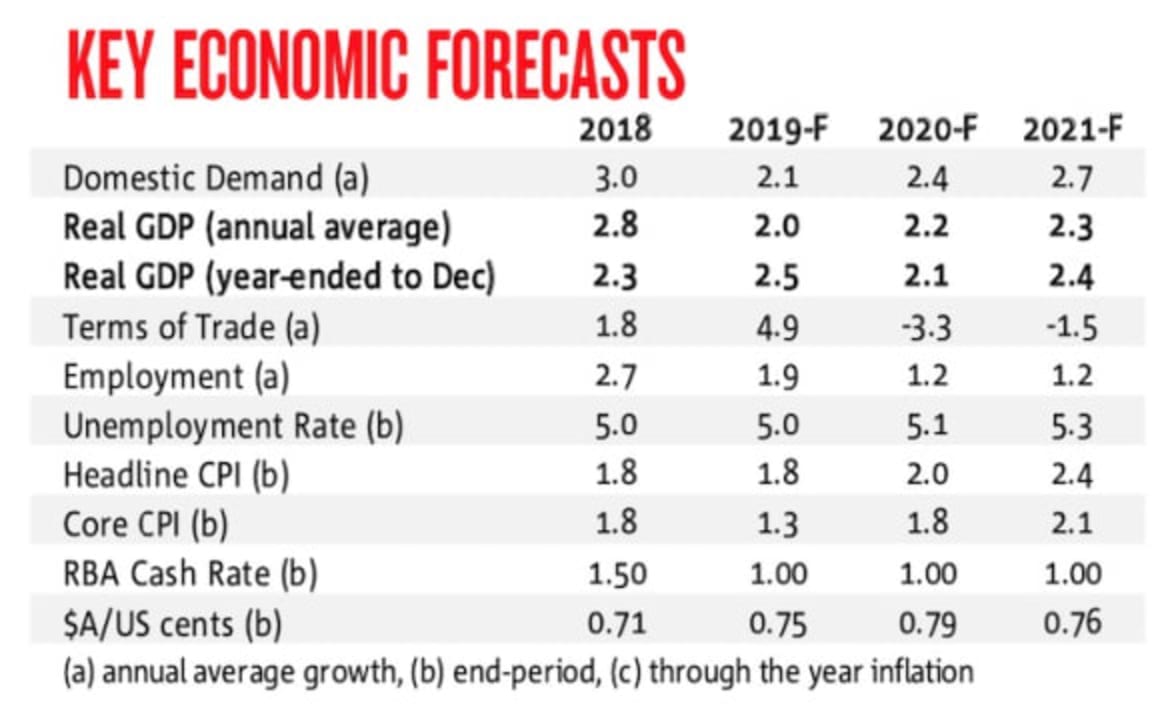

With its outlook for below trend growth, and below target inflation combined with little further improvement in the labour market, NAB expect the RBA to cut rates twice in 2019, taking the cash rate to a new record low of 1%.

"We expect a cut by at least August."

"We have left our call for the first cut as July, with a follow up in November."

However, with the RBA still looking for an improvement in the labour market and monthly figures often volatile, NAB recognise that the timing of the first cut will be especially data dependent.

"On the one hand a marked deterioration in upcoming labour market data as well as weaker national accounts partials, could see the cut brought forward to next month.

"Against that a cut could be delayed to August when the Bank will have observed another quarter of likely weaker GDP growth, a further update on the CPI and a revised set of staff forecasts ahead of the next SMP."

NAB noted labour market indicators should be closely watched, as a turn in the labour market could reasonably be 1.0 expected given the prior slowing in output growth.

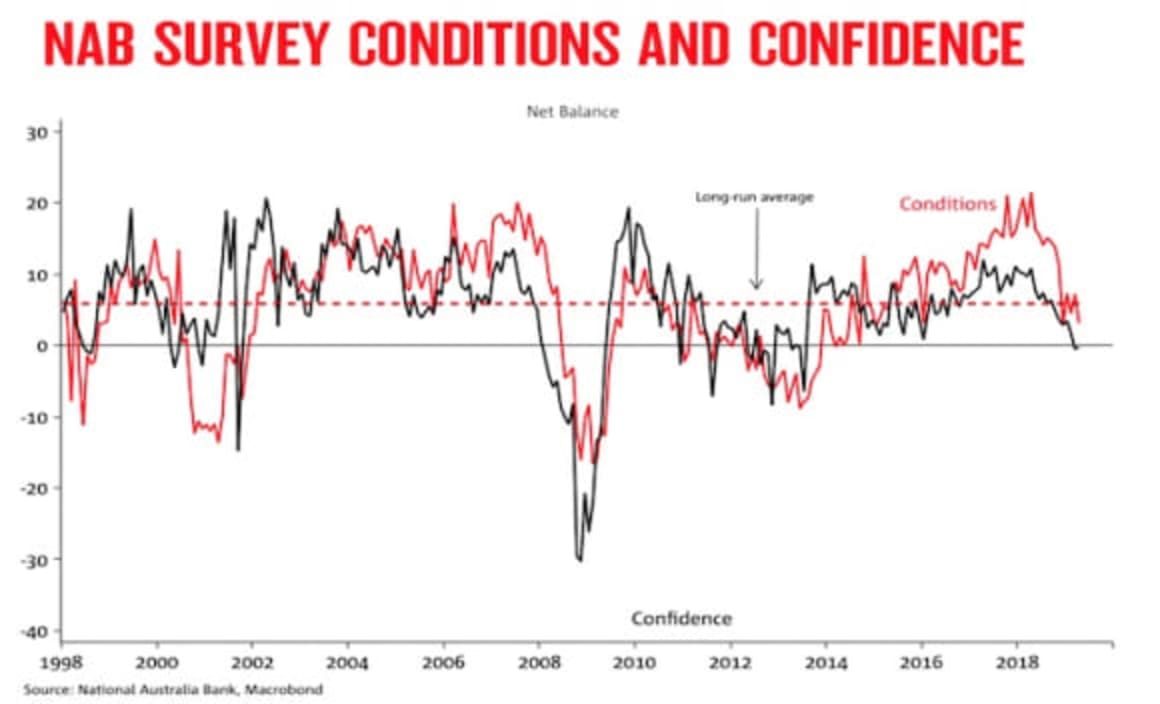

The NAB Survey measure of employment weakened in April and job ads appear to have fallen.

The NAB reported the impact of the downturn in the housing market was "affecting both output and inflation data.

"The cooling appears to be ongoing, with prices continuing to decline and building approvals continuing to trend down."

NAB expect dwelling investment to record another decline in Q1 following the relatively sharp fall in the last quarter of 2018.

"Overall we expect dwelling investment to decline by around 20% over the next two years.

"Alongside this, we expect house prices to decline by another 5% nationally over 2019 and early 2020 before levelling out for a period."

The report noted capital city house prices have now fallen by almost 10% since peaking in late 2017.

"These declines have been led by Sydney (down 15%) and Melbourne (down 11%) where the role of investors is much larger and prices saw a much more significant rise.

"That said, recent months have seen price declines broaden to the other states, with Brisbane and Adelaide having now declined over the year in addition to the ongoing weakness in Perth. In Hobart growth has slowed, but the city remains the standout, with prices remaining well up on a year ago," ALAN OSTER said.

On the activity side, building approvals continued their trend decline in March, unwinding the spike a month earlier.

Over the past year approvals are 27% lower and are now 37% below their peak in 2017.

The decline in approvals is evident across both houses and apartments down 19% and 57% respectively from their peaks in 2017.

The decline in approvals suggests that activity in the sector will weigh on growth overall as the pipeline of outstanding work is completed.

NAB noted alongside the cooling in the market, housing credit growth has continued to slow.

Investor lending slowed to just 0.7% y/y in March 2019, while growth in credit extended to owner-occupiers is tracking a little higher but has slowed to 5.7%.

Overall housing credit has risen by 4.0% over the past year.

ABS data on the value of new loan approvals has continued to trend down suggesting that credit growth will likely weaken a little further over coming months.

"To date, the adjustment in the housing market appears to have occurred in an orderly fashion – and may have served to reduce the prior build up of risk in the sector," ALAN OSTER said.

"We see the weakness in prices as having been driven by the earlier tightening driven APRA restrictions, a waning in foreign investor demand as well as affordability constraints themselves.

"In addition it appears that there are some pockets of oversupply.

"Going further, we see the cooling in the market continuing with prices declining a little further and also a notable downturn in the construction cycle.

"Beyond this, we are closely watching for any additional spill overs from this sector to other sectors."