RBA cuts the cash rate to a new record low of 1.5 percent: Shane Oliver

GUEST OBSERVER

The RBA has cut the official cash rate by 0.25 percent taking it to 1.5 percent, a new record low.

Money markets had priced in around a 70 percent probability of a cut and economists were split roughly 80 percent/20 percent in favour of a cut.

In justifying the move the RBA stated that “prospects for sustainable growth in the economy, with inflation returning to target over time, would be improved by easing monetary policy at this meeting.”

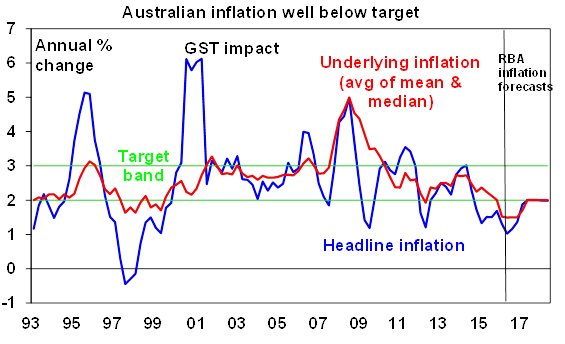

With the RBA seeing growth “continuing at a moderate pace”, the latest rate cut is all about adding to confidence that inflation will head back to the 2-3% target zone within a reasonable time and to help maintain downwards pressure on the value of the $A in the face of ongoing delays in Fed rate hikes.

In terms of inflation the RBA is trying to prevent a further fall in inflation expectations that could push wages growth to new record lows and make it even harder to get inflation back to target. The longer inflation remains low and below target the greater the risk that it will become entrenched as we have seen in several other developed countries in recent years.

Source: ABS, AMP Capital

In relation to the $A, the RBA is clearly keen to see it continue to help trade exposed sectors like tourism, manufacturing and higher education. The problem though is that “easy for longer” monetary policy globally – particularly in the US with seemingly endless delays in Fed rate hikes – is putting upwards pressure on the $A. Following the rate cut the $A is actually up slightly – highlighting the upwards pressure that it faces. If the RBA had not cut it would probably be on its way to $US0.78 or maybe $US0.80 – which as the RBA indicates “could complicate” the adjustment in economy.

Finally, after the full pass through of the May rate cut it looks like we are only seeing partial bank pass through to mortgage rates this time around with a couple of major banks passing on just 0.1-0.13 percent this time around. This may reflect ongoing pressure on the major banks to hold more capital (which is a more expensive source of funding) and competition amongst major banks to offer more attractive term deposits. That said some small lenders may pass the cut on in full in order to expand their market share.

Will there be another cut? As always after a move the RBA’s guidance doesn’t give much away and often leads many to conclude that it has reverted to a neutral bias on future rate moves. However, we are allowing for one more rate cut in November based on our expectation that the September quarter inflation data (due in late October) will remain much lower than desired and that upwards pressure on the $A will likely remain.

Implications

For the economy the RBA’s latest rate cut is positive in that it will help support household spending power (albeit it will be muted by the only partial pass through of the latest cut to mortgage rates) and help keep the $A lower than otherwise would be the case. While low bank deposit rates are bad news for those relying on income from bank deposits it’s worth recalling that the value of household debt is more than double that of household bank deposits.

Quite clearly, there is a risk that the latest RBA rate cut reinvigorates home price strength in Sydney and Melbourne. However, the RBA is clearly now less concerned given more cautious bank lending attitudes and a considerable supply of apartments set to come on stream. If this is not the case then it can clearly work with APRA again to make sure that it is.

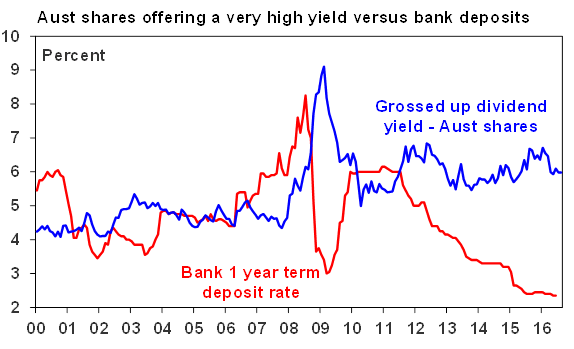

For investors relying on bank interest, the decision by the RBA to cut the cash rate is not good news. That said competitive pressures have seen some banks raise their deposit rates a bit lately.

The trouble is that the they are still very low. Beyond day to day cash requirements, the key for investors currently in cash or term deposits is to work out what is most important to them: absolute certainty regarding the capital value of their investment or obtaining access to a higher more stable income flow at the cost of volatility in the value of their investment.

In this, there are several alternative investments to cash, including shares offering high and sustainable dividend yields, commercial property, corporate debt and infrastructure investments

Source: RBA, AMP Capital

SHANE OLIVER is head of investment strategy and economics and chief economist at AMP Capital and is responsible for AMP Capital's diversified investment funds.