Personal loans drive lift in lending: CommSec's Savanth Sebastian

GUEST OBSERVER

Lending: Total new loans (personal, business, housing & lease) rose by 0.7 percent in March after a 3 percent rise in February. Lending was just 3.9 percent shy of the 7½-year high recorded in November 2015.

Total lending is up 1.6 percent on a year ago.

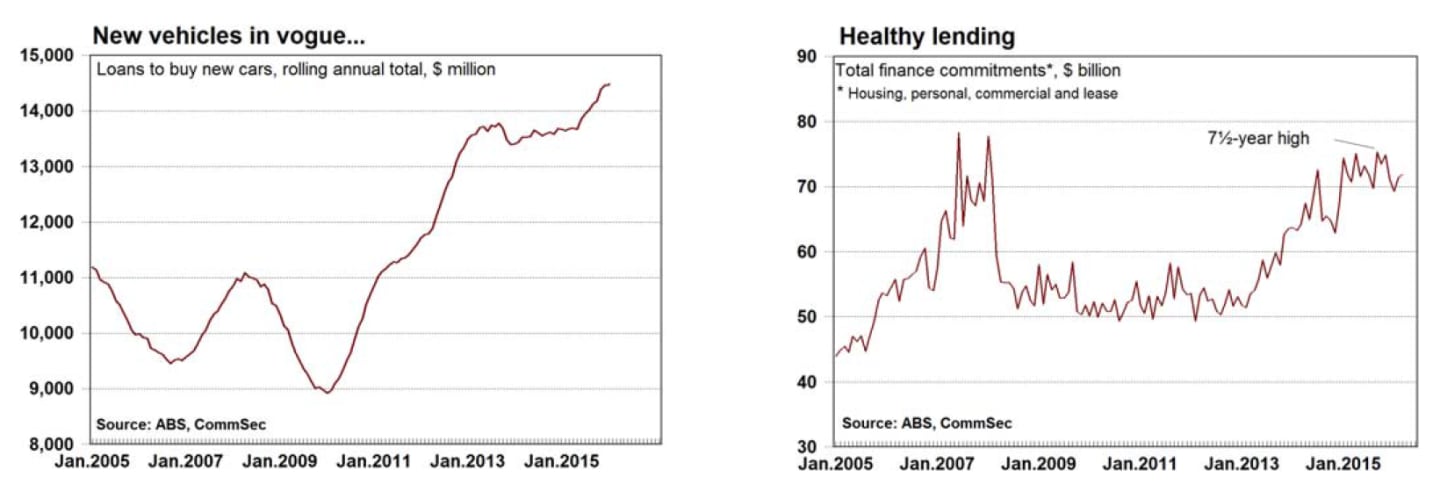

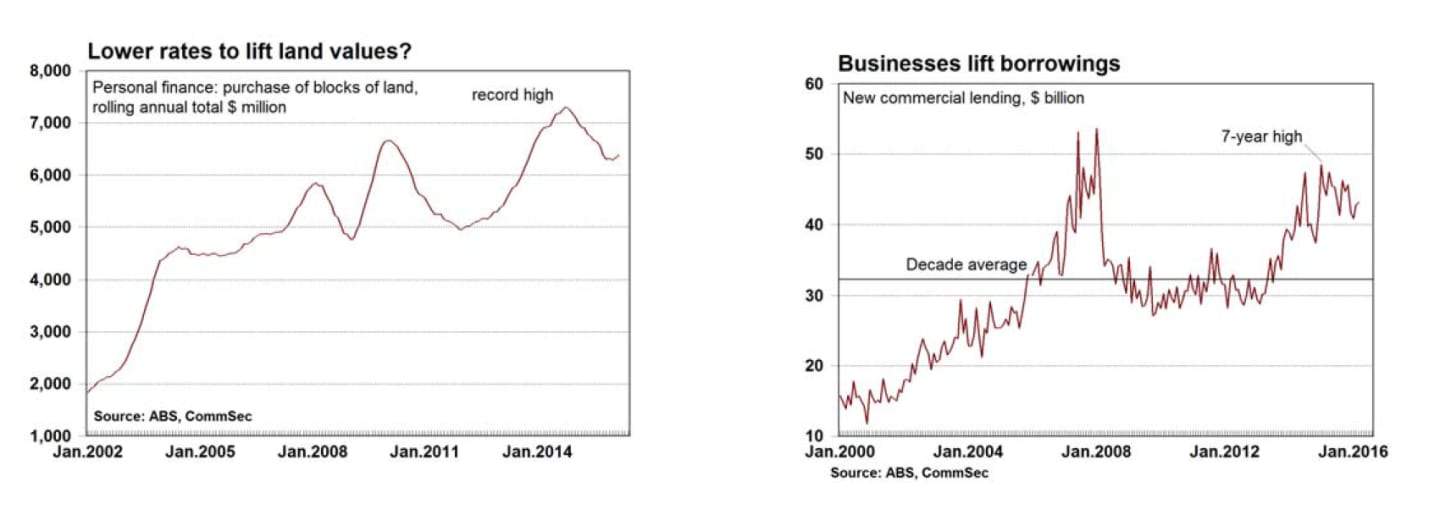

Within personal fixed finance commitments, loans for new cars were up by 20.4 percent on a year earlier while loans for used cars were up 15.5 percent. Loans for residential blocks of land were up by 9.1 percent on a year ago.

The lending figures have implications for finance providers, retailers, and companies dependent on consumer and business spending.

What does it all mean?

Similar to the housing finance data early this week, the lending statistics is essentially old news – pre Reserve Bank interest rate cut. In fact the shift in Reserve Bank commentary to a lower inflation profile suggests that further interest rate cuts are on the cards. And in that context very likely to support further lending not just in housing but across the business sector as well.

The lift in borrowing across the economy in March is encouraging coming of the back of solid gains in February.

Overall, total lending is just shy of 7½-year highs recorded in late 2015. While lending remains healthy the hope would be that business borrowings lift from here - driving investment and supporting medium term growth.

The generational low interest rates will be supportive of further borrowing – but there is no guarantee. While Reserve Bank policymakers would be hoping that the latest rate cut spurs another round of activity, they would be well aware that borrowers are cautious about taking on more debt. And lower interest rates compress bank margins, affecting profits and potentially investment, employment and shareholder returns.

Unfortunately elections cause consumers and businesses to hold back on spending, employment and investment plans, and that is the risk to the positive momentum that has built up in recent months. CommSec expects that the low inflation outlook will result in further cuts to the cash rate. Rate cuts have been pencilled in for August and November.

What do the figures show?

Lending Finance

Total new loans (personal, business, housing & lease) rose by 0.7 percent in March after a 3 percent rise in February. Lending was just 3.9 percent shy of the 7½-year high recorded in November. Total lending is up 1.6 percent on a year ago.

Housing finance: The seasonally adjusted measure of construction and new purchases fell by 1.2 percent in March while alterations & additions rose by 0.4 per cent. Home loans are up 11.9 percent on a year.

Commercial finance : The seasonally adjusted series for the value of total commercial finance commitments rose by 0.9 percent in March after rising by 4.8 per cent in February. Revolving credit commitments rose by 2.3 percent. Fixed lending commitments rose by 0.4 percent. Business loans are down 2.2 percent over the year.

Personal finance : The seasonally adjusted series for the value of total personal finance commitments rose by 6.3 percent in March after falling by 2.9 percent in February. Revolving credit commitments rose by 11.9 percent and fixed lending commitments rose by 3 per cent. Personal loans are down 1.9 percent over the year.

Within personal fixed finance commitments, loans for new cars were up by 20.4 percent on a year earlier while loans for used cars were up 15.5 percent. Loans for residential blocks of land were up by 9.1 percent on a year ago.

Lease finance : Lending fell by 7.7 percent in March and was up 0.8 percent over the year.

What is the importance of the economic data?

Lending Finance is released monthly by the Bureau of Statistics and contains figures on new housing, personal, commercial and lease finance commitments. The importance of the data lies in what it reveals about the appropriateness of interest rate settings, confidence and spending levels in the economy.

What are the implications for interest rates and investors?

At present the national economy is tracking ok. Economic growth is healthy and more encouragingly unemployment is at a 2½-year low. However the concern for policymakers is that the deflationary environment becomes more firmly entrenched in coming quarters. A sustained super low inflation landscape will lead to low inflationary expectations over time and in turn a shift in asset allocation.

The bottom line is that underlying inflation is undershooting the 2-3 percent target band and that suggests little risk in cutting rates a little further. CommSec believes there is a strong chance the Reserve Bank will cut interest rates twice more this year, taking the cash rate to a historical low of 1.25 percent by in November.

Savanth Sebastian is an economist for CommSec.