Sydney's housing shortage is about a mismatch of supply: Pete Wargent

Property buyer's agent Pete Wargent gets a zinging from Michael Janda of ABC News today. No probs with that, I've been a long-time fan of Mike's work.

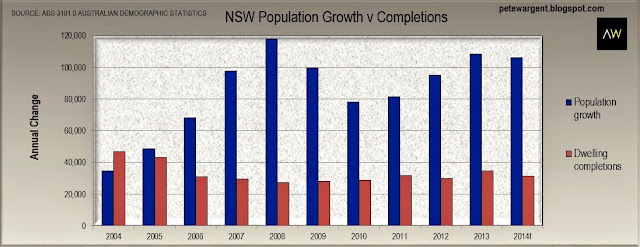

Below is my chart which initiated the debate on Sydney's housing shortage (or otherwise), which shows that over the past nine years, population growth in New South Wales has accelerated while dwelling completions have remained at or below their long run averages.

What Mike is arguing is that over the long run, New South Wales has built enough homes, and he has the data to back this up.

Of course, in one sense this is inarguable - there aren't tens of thousands of people living on the streets in Sydney, so by definition the market has coped, and there is no easily quantifiable "housing shortage".

Housing markets are complex beasts, however, and my point is rather more nuanced.

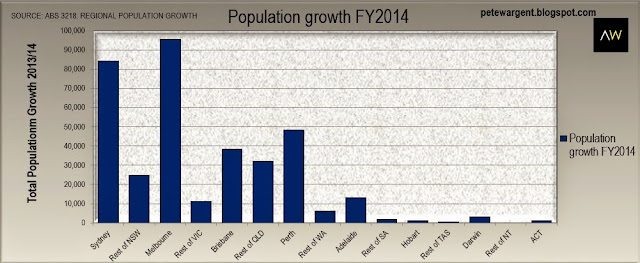

In the simplest terms if Greater Sydney's population growth continues as it has been of late (massively outstripping regional New South Wales), and as is projected, then based on historical dwelling completions data the market is likely stuffed, particularly at the granular level.

As I'll explore below, the reason is related to a mismatch of supply within Sydney's relatively confined boundaries.

As alluded to above, the notion of a housing shortage is something of a nebulous concept, but here are three shortages that I believe do exist.

Shortage 1 - Land available for development

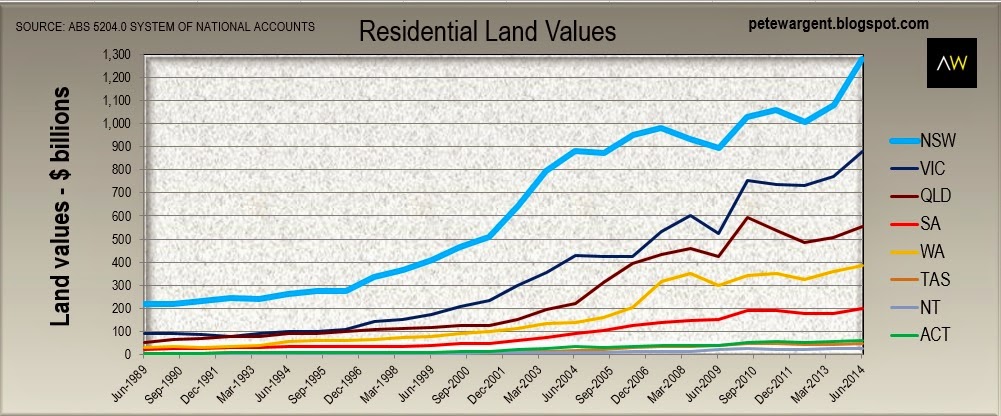

Over the past six years, in aggregate residential land values in New South Wales have increased by 37%.

But as Mike points out in his ABC piece, the use of averages can lead one to very average conclusions, and this figure disguises the intense pressure on Sydney's drip-fed land supply.

While regional Australia has generally only experienced benign land price inflation, lot prices in Sydney have been going ballistic, exploding 19.7% higher in 2014.

In some suburbs such as Kellyville land price inflation is bordering upon out of control, with prices rising 38.2% in 2014 alone, up to $912 per square metre.

Median prices in Glenmore Park rose by 30.6%, in Riverstone by 20.2%, and in Pitt Town 26.4%.

The median price of land in the south west soared by 25% to $350,000, while prices in Sydney's west, where lot sizes can be larger, rose by 8.3% to $410,500.

Extrapolating existing trends Dr. Andrew Wilson of Domain Group expects Sydney's median land prices to increase by another $40,000 in 2015 until "the chronic undersupply of residential development land is effectively addressed".

The system is not functioning as it should. Land supply in Sydney is in dire straits as I considered in more detail here.

Shortage 2 - Appropriate dwelling stock

Over FY14 Greater Sydney saw a measly 6,793 dwelling approvals in its inner suburbs, and only 18,610 in the middle ring suburbs (5 kilometres to 20 kilometres radius from the Central Business District).

There were a further 13,670 approvals in the outer and fringe suburbs, but as highlighted by the Reserve Bank, job density is increasing faster in the inner city areas, and thus so too is demand for residential property.

The Grattan Institute has arrived at similar conclusions highlighting how although nearly 60% of jobs are created with 10 kilometres of Australia's CBDs, the percentage of jobs which can be reached within 60 minutes by public transport quickly evaporates as one travels outward, making outer suburban living ever less desirable as traffic congestion increases.

The result, as found by both AHURI and the Reserve Bank, is that the gradient of house price growth has remained skewed towards the inner Sydney suburbs, both over the long term and over the past decade.

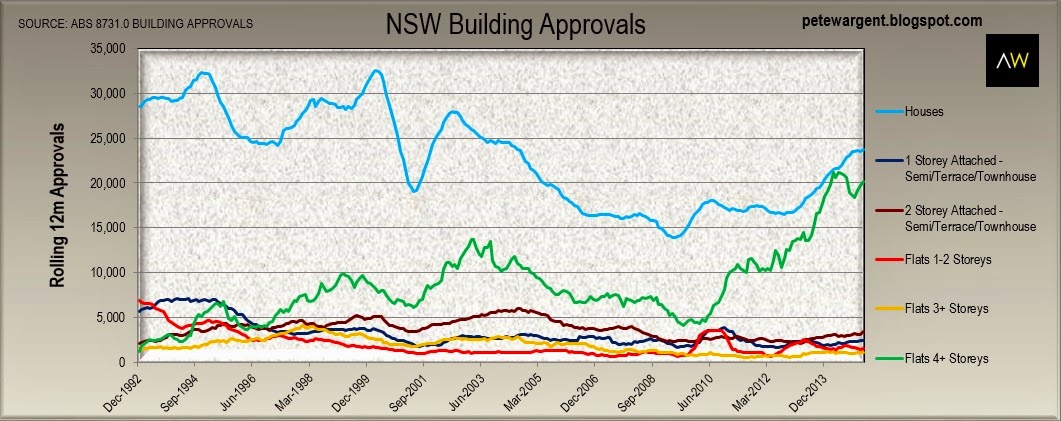

Moreever, while there may be "enough" dwellings in aggregate, all that has really happened in terms of the supply response is that since 2010 we have been approving previously unthinkable volumes of "shoebox apartments" in high rise complexes (see the green line in the graphic below).

Much of this stock is sold offshore to Asian investors, and in my opinion the underlying demand for it domestically is likely to be weak, both from tenants and home buyers. Meanwhile we are building far fewer houses, two-storey dwellings or stock which is actually like housing than was ever the case before.

The recent experiences of Melbourne suggest that this dynamic may not impact housing markets or housing affordability in the positive way that many expect.

Shortage 3 - A shortage of ideas

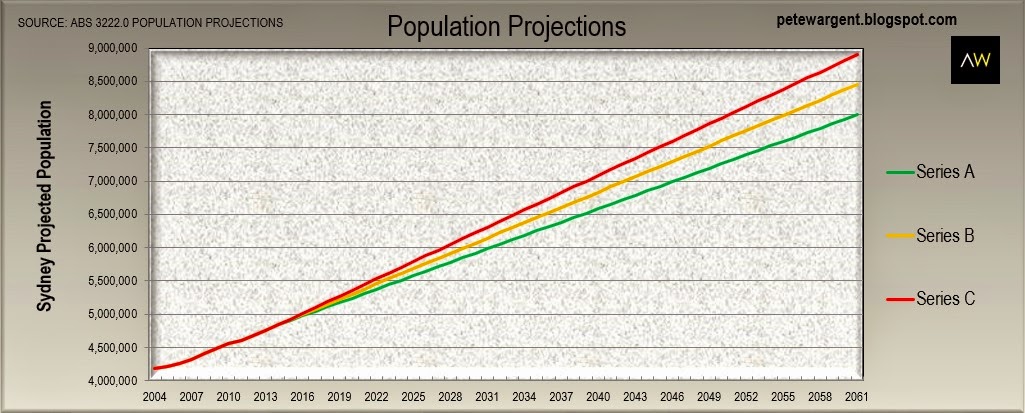

What I haven't seen any compelling evidence of is how Sydney is planning to absorb its projected 8 to 9 million population of 2061 effectively.

I don't even know where to start with this as the numbers are mind-blowing.

Are there realistic plans for public transport or infrastructure? Any encouragement for corporates to relocate their headquarters to regional centres? Or indeed, any genuine investment in regional employment growth at all?

I have believed for years that Sydney will end up as a housing affordability disaster zone, and while the property crash warnings keep coming as regularly as the tides at Bondi (or the traffic congestion reports from the Harbour Bridge), over the longer term I haven't yet seen anything to change my view.

That said, it's not all doom and gloom.

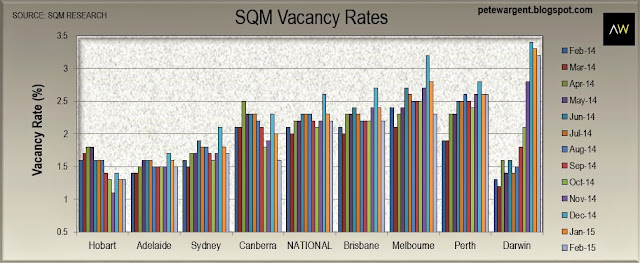

It's not so fashionable now that markets are so much tighter than they once were, but in times past it be said that a market "in equilibrium" should have a vacancy rate of 3% - and Sydney doesn't have anything like that yet, sitting at just 1.6%.

However, vacancy rates are finally being nudged higher around a few key construction hubs, which will ultimately put upwards pressure on apartment vacancy rates and an equivalent downwards pressure on unit rents.

These include certain suburbs in the inner west (Erskineville), the inner south (Mascot, Green Square), north Sydney (Chatswood, North Sydney), and the surrounds of Olympic Park (Homebush Bay, Rhodes), to name a few.

In that sense, then, there is no actual "shortage" of dwellings, which I think on balance is Mike's point - in a downturn some of these investor hotspots could get clobbered, leading in turn to unanticipated adverse outcomes through the wider market.

The wrap

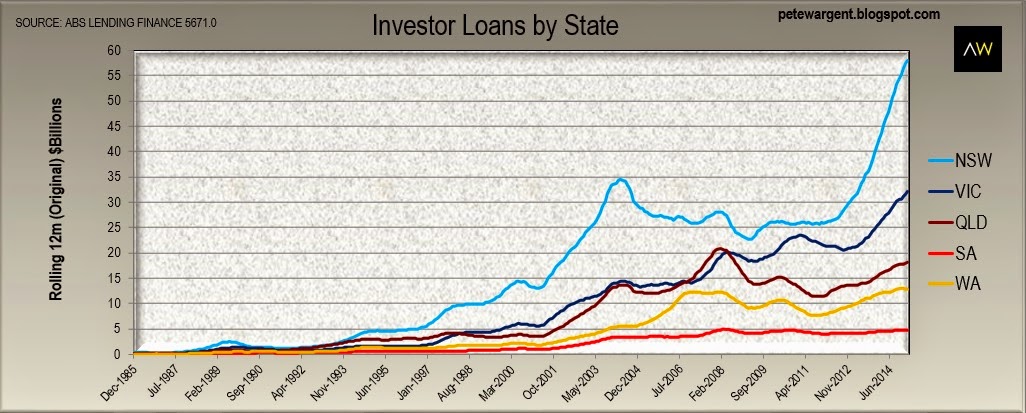

Mike is also correct that the current boom is now being led by demand. No arguments there, it's been largely an investor-led phenomenon through this cycle, although the latest data suggested that owner-occupiers are now gearing up due to a fear of missing out.

Supply can tackle housing affordability over the longer term, though I'm not convinced of how effective this will be. Over the shorter term only restricting credit and curbing or discouraging demand can work quickly. Over to APRA.

PETE WARGENT is the co-founder of AllenWargent property buyers (London, Sydney) and a best-selling author and blogger.

His book 'Four Green Houses and a Red Hotel' is out now.