Interest-only loans running at 70 per cent down on 2015 peak: Pete Wargent

EXPERT OBSERVER

OK, first things first.

I am indeed a so-termed vested interest: I would like to see full employment, stronger wages and household income growth, the Aussie economy growing at least at trend or ideally above trend, and I don't want to see the housing market getting zinged unnecessarily.

Yep, you got me on that one.

With these formalities out of the way, I saw APRA's latest ADI exposures today described as 'red alert lending data', very 'concerning', a 'loosening' of lending standards, that should be 'ringing alarm bells' to APRA due to lenders 'breaking their own rules', among various other remarks (source: Digital Finance Analytics).

For the record, while blog-flaming isn't really my bag, I must wholeheartedly disagree on each and every point!

Whatevs, I'll post a few deets and you can make your own mind up...

Whatevs, I'll post a few deets and you can make your own mind up...

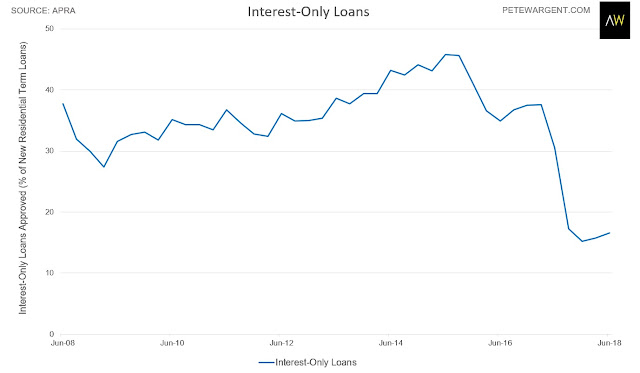

Stock of IO loans plunges

Firstly, the flow of new interest-only (IO) loans in Q2 2018 was a meagre 16.6 per cent of residential term loans, absolutely miles below the initially proposed cap of 30 per cent (and a world apart from the 45.6 per cent record high of Q2 2015).

With far fewer loans written overall from a year earlier in spite of a strong increase in the Aussie population, this represented a modest increase in percentage terms from the preceding quarter.

However, the actual number of interest-only loans was some 52 per cent lower than in the corresponding quarter of the prior year - and almost 70 per cent lower than the number written at the peak of IO lending in 2015.

A 'loosening'? Hardly.

But even if more IO loans were to be written henceforth I personally don't believe that would be a bad thing.

But even if more IO loans were to be written henceforth I personally don't believe that would be a bad thing.

The last thing we need is $½ trillion of IO mortgages being reset with undue haste - unless you actually want to see the housing market get stiffed, which of course many people do - and some breathing space would surely be welcomed by a portion of existing IO borrowers.

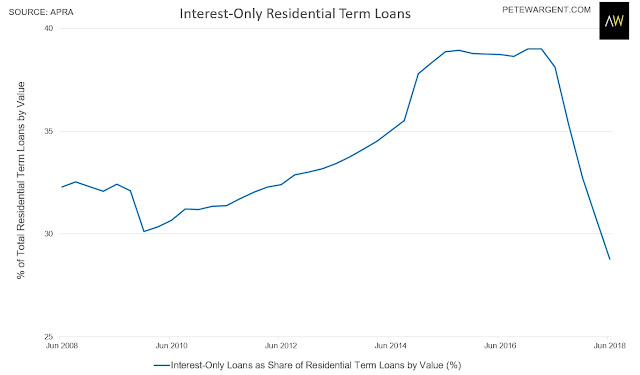

Regardless of your views on that, there was another enormous decline in the stock of IO loans in the June quarter, with IO loan balances outstanding now having plunged some $119 billion lower over the past five quarters.

The share of IO loans outstanding through June 2018 was thus by some margin at the lowest level across the entire data series at about 29 per cent, down from close to 40 per cent in late 2015.

Note that these numbers only run to the end of the 2018 financial year; at the current trajectory the share of IO loans will likely be around 26.9 per cent by the end of this month, a figure that was truly unthinkable only last year, and the lowest level in decades.

A loosening...very droll.

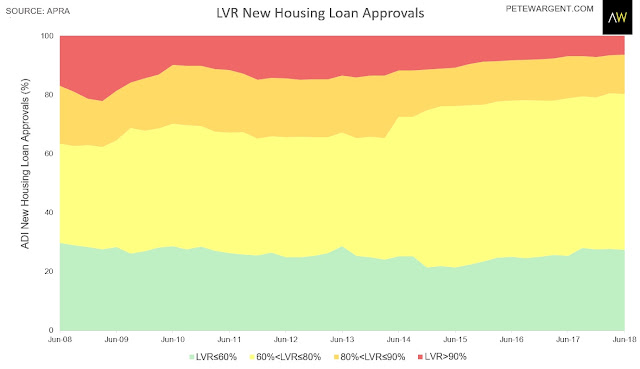

Less and less and less high-LVR lending

Secondly, in relation to DFA's 'red alert' on lending standards, the loan-to-value (LVR) ratios on new loans have been tightening incrementally for the better part of half a decade now.

Secondly, in relation to DFA's 'red alert' on lending standards, the loan-to-value (LVR) ratios on new loans have been tightening incrementally for the better part of half a decade now.

Loan volumes are down, there was a miniscule change in Q2 for the share of new loans written at 80 per cent LVR or above, while loans written above 90 per cent LVR or above have never been as low as they are today since the available records began.

'Red alert'? You must be having a giraffe, surely - we've literally never seen lending standards remotely like it!

Thirdly, low-doc and other non-standard loans are also tracking at the lowest level on record.

Fourthly, the quarterly flow of new investment loans plunged by the best part of $5 billion year-on-year, so how you conclude a sudden loosening of standards from that I can't fathom (automatic red card for anyone directly comparing volumes from Q1 to Q2).

And fifthly, a word that is devilishly hard to spell at the best of times, DFA cites loans approved outside serviceability, noting that these should be ringing 'alarm bells' to the regulator.

Fair suck of the sauce bottle, mate, but this almost certainly represents a timing issue and reflects tighter lending standards, not looser.

You can't tell me with a straight face that banks are blithely waving through marginal or borderline applications and then willingly reporting them as such in the current lending environment. Not happenin'.

'I could go on...', as Jon Culshaw's impersonation of Russell Crowe might drily observe.

Due apologies for the apparent curtness, but this stuff has a tendency to be uncritically reported by rote, so someone needs to chime in with a few of these inconvenient actualities.

Much obliged. As you were :-)

Much obliged. As you were :-)

Pete Wargent

Pete Wargent is the co-founder of BuyersBuyers.com.au, offering affordable homebuying assistance to all Australians, and a best-selling author and blogger.