WA home loan arrears still problematic for CBA: Pete Wargent

EXPERT OBSERVER

The Commonwealth Bank of Australia reported its full year results last week.

Cash profit for FY2018 of $9.41 billion was down 4.7 per cent.

But overall this remained a solid underlying result with a fully franked dividend of $4.31 per share heading the way of investors (up 2 cents or +0.5 per cent...thanks!).

Increased funding costs impacted net interest margins adversely as expected.

However, the group more than made these costs back in the financial year through changes in the funding mix and the repricing of investor and interest-only loans.

In fact, the net interest margin was up 5bps over FY2018 to 2.15 per cent.

Group loan impairment expense was also very low, at just 15bps.

Note that the Group will adopt AASB 9 from 1 July 2018, and therefore total provisions will increase to reflect forward-looking factors as required by the standard (this adjustment will will pushed through opening retained earnings and therefore will have no impact on the current year income statement).

'As if' earnings

A number of one-off items including the $700 million AUSTRAC penalty reduced the statutory NPAT and cash NPAT.

Excluding one-off items, cash profit was up by 3.7 per cent to above $10 billion.

From the slide deck

There were so may great slides in the full year preso that's it's impossible to know where to start, but here are just a select few.

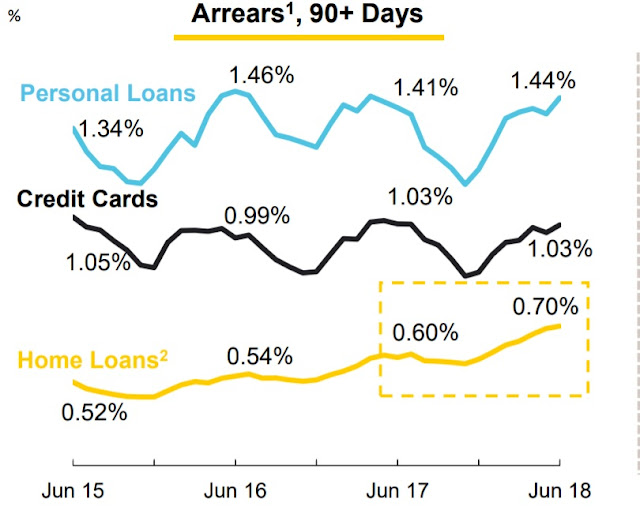

90+ day home loan arrears were notably up a bit year-on-year from 0.6 per cent to 0.7 per cent.

Click to enlarge

(Source: ASX: CBA)

The year-on-year increase in arrears was mainly due to Western Australia and the Northern Territory, with changes elsewhere relatively benign.

The switching of interest-only (IO) loans peaked in September 2017.

There is still plenty of scheduled IO expiry over the next two financial years, however, with the blue bars arguably representing the loans most at risk of arrears (being IO loans to investors).

Home loan repayments in advance remain popular, though not for all borrowers.

Finally, CBA optimistically notes that outside recessions or global financial crises modern housing downturns generally only last about 8 months on average (so on that basis, this one should be about done).

PETE WARGENT is the co-founder of AllenWargent property buyers (London, Sydney) and a best-selling author and blogger.

Pete Wargent

Pete Wargent is the co-founder of BuyersBuyers.com.au, offering affordable homebuying assistance to all Australians, and a best-selling author and blogger.