Genworth mortgage insurance update: Pete Wargent

Given that APRA's crackdown on investor lending has skimmed so many high loan-to-value ratio (LVR) investors out of the property market, it was always going to take a super-human 1Q 2016 investor update from Genworth Mortgage Insurance (GMA) to keep its share price buoyant.

In the event, GMA reported statutory net profit after tax (NPAT) of $67.3 million and underlying NPAT of $61.8 million for the quarter ended 31 March 2016.

Overall this was a solid set of results given that Gross Written Premium was down by a thumping 33.4 per cent from 1Q 2015, having declined dramatically from $127.7 million to $85 million.

This statistic is a fabulous measure of the impact of the regulatory intervention - the riskier loans have largely been crimped out of the property market.

Delinquencies

Genworth's portfolio delinquency rate was marginally higher at 0.40 per cent, up from 0.36 per cent in 1Q 2015.

Overall mortgage delinquencies remain remarkably low, and can realistically only move in one direction from here, particularly given that numerous resources towns in regional Queensland have effectively become ghost towns.

Unfortunately many investors were sucked in to buying in mining towns and regions lured by superficially "stronger" yields, but unfortunately in many cases there is now nobody to rent the houses to, and as equity turns negative foreclosure rates will inevitably rise.

The lesson here is that "yield" and "income" are not the same thing, and that as an abstract spot calculation yield is largely useless as an indicator of future returns. This applies to all asset classes.

Even in some of the larger conurbations there are likely to be some severe challenges ahead, with unemployment in Townsville having risen to a 13 year high last month.

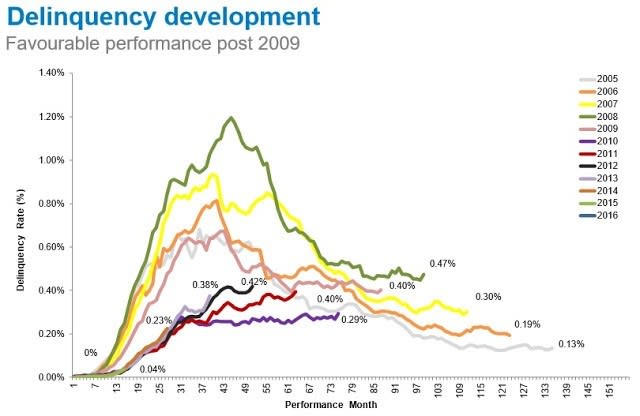

Despite these bleak statistics, overall delinquency developments have shaped up quite favourably since 2009, with mortgage delinquencies by book year having cascaded lower over time.

The 2008 book year saw heightened mortgage stress among self-employed borrowers as a result of the financial crisis (0.98 per cent), while flooding in Queensland saw elevated delinquency rates in the 2011 book year.

At the state level delinquency rates are incredibly low in New South Wales (0.29 per cent).

Delinquency rates are notably higher in Queensland (0.55 per cent), in part due to mining town foreclosures, and largely related to the literal wash-up from the severe 2011 flooding in the state.

The largest year-on-year rise in delinquency rates of 16 basis points was seen in resources rich Western Australia, where portfolio delinquencies have increased to 0.53 per cent.

Nevertheless, Genworth sees the mortgage market remaining strong in aggregate, reporting in its investor update:

"The outlook for the Australian residential mortgage market remains strong, supported by sound fundamentals including low unemployment, record-low interest rates and a continued focus by regulators on lending standards."

And notably Genworth expects further constraints on high LVR lending in 2016 and beyond:

"The high LVR market continues to be constrained in 2016 and Genworth continues to expect GWP to decline by approximately 20 per cent due to these market conditions."

Share market analysts were fairly unmoved on the news, the share price steady at around $2.39.

PETE WARGENT is the co-founder of AllenWargent property buyers (London, Sydney) and a best-selling author and blogger.

His latest book is Four Green Houses and a Red Hotel.

Pete Wargent

Pete Wargent is the co-founder of BuyersBuyers.com.au, offering affordable homebuying assistance to all Australians, and a best-selling author and blogger.