Residential construction boom tapering off: Pete Wargent

It looks as though 2016 is shaping up to be a year within which the residential construction boom, which has mostly served the demands of foreign investors, begins to tail off.

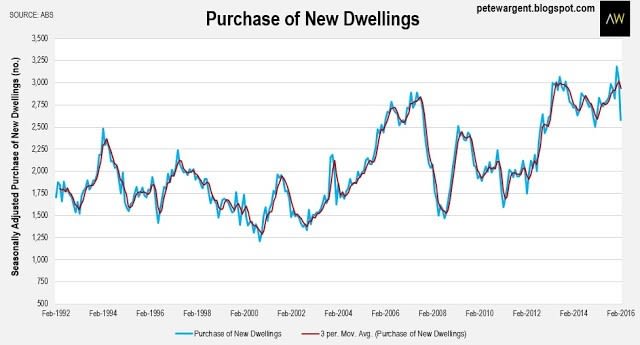

We should never read too much into the results of one month, of course, but reflecting trends that have already been reported by Housing Industry Association (HIA) finance for the purchase of new dwellings fell by more than 15 percent in February.

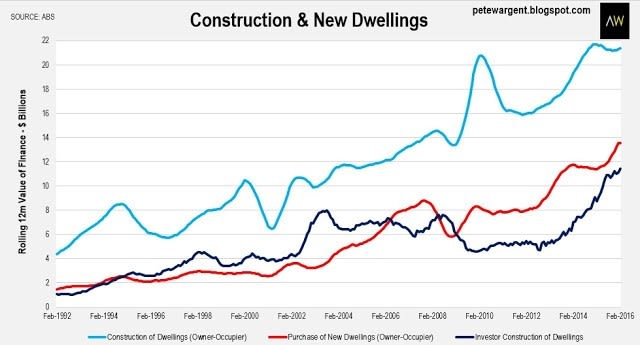

Although it is not yet much reflected in the rolling annual data below, finance for the construction of new dwellings also ticked back by -1.9 per cent in February.

It may or may not be too early to call the peak on finance for dwelling construction after a very solid run through this cycle, but market releases suggest that building approvals are now on a downslope, and construction will probably follow suit in time too.

Market shifting away from investors

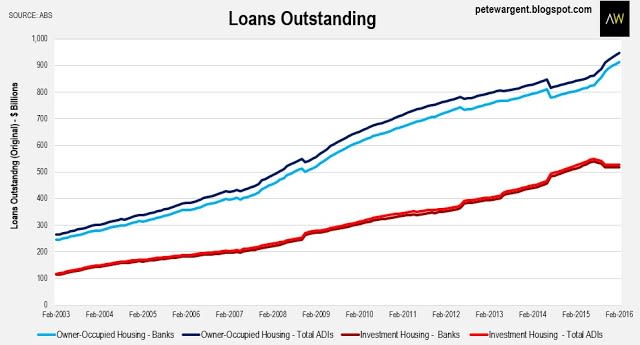

Figures showed investor lending steadying at around a seasonally adjusted $11.9 billion, which is still a historically high figure, but some way down from the August 2015 peak.

A quick glance at the chart for loans outstanding shows how banks and lenders have shifted their focus in favour of home loans, a direct response to APRA's regulatory intervention.

We know that there remain blurred lines between investor and home loans, but the February data shows that overall the balance has tilted back in favour of owner-occupier finance ($21 billion) over investment housing finance ($11.9 billion).

Overall, 2016 looks likely to be a steadier year for property markets, as investors are limited in their borrowing capacity.

It's worth remembering that owner-occupiers represent a greater share of the market, and as such have the potential to push prices up in the areas in which they are buying (think middle-ring suburbs, catchments for good schools, good transport links, appealing shopping and lifestyle locations).

Investors should now begin to account for about one third of the market, which is much more in line with historical averages.

It's worth remembering that owner-occupiers represent a greater share of the market, and as such have the potential to push prices up in the areas in which they are buying (think middle-ring suburbs, catchments for good schools, good transport links, appealing shopping and lifestyle locations).

Investors should now begin to account for about one third of the market, which is much more in line with historical averages.

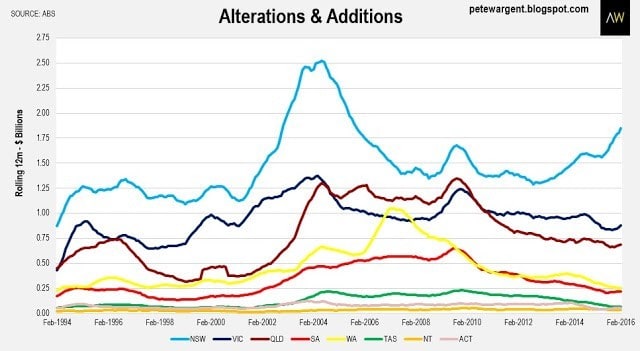

With returns from fixed interest accounts so low and mortgage repayments much lower than they were, many in the home ownership sector will look to improve the value of their own homes, or look to acquire renovation projects.

Indeed major renovations activity is now at long last trending up in all three of the most populous states, with Sydney leading the way by a margin. Renovation activity is presently less popular in Melbourne, with considerably more modern housing available following a strong decade of construction and dwelling supply.

First homebuyers subdued

While 2016 looks set to be the year of the homebuyer, much of the activity is being driven by refinancing and existing home-owning folk looking to trade up or down, rather than by new market entrants.

Even if the ABS data is not quite complete or accurate, it seems fair to surmise that the share of dwellings financed by first homebuyers is tracking some way below the long run averages.

The wrap

2016 therefore seems likely to be a year wherein markets are increasingly moved by homebuyers ahead of investors.

It is worth reiterating here that in part due to high transaction costs, whether bought as a home or a pure investment, property works best as a long term play.

The internet and financial media is largely - though, of course, not absolutely - a fusion of noise, short-termism, misinformation and guesswork when it comes to property market commentary. You only need to look back to 2012 for some classic examples of that.

In my opinion there is very little value in comparing returns with the share market over a one or two year timeframe. Each asset class has its merits and place in a portfolio, but generally speaking property needs at least a ten year time horizon in order to justify the transaction costs.

The data yesterday confirmed that home loan activity levels - although not necessarily aggregate mortgage values - are rising solidly in Queensland, and this is readily visible in some of the family-friendly middle ring suburbs of Brisbane. Investor hubs are considerably patchier, and many of the resources regions are an absolute disaster zone.

A final point of interest for today is that markets had increasingly been lining up bets for an interest rate cut as soon as May, though I personally didn't like the odds of that happening.

I don't spend hours deliberating over monetary policy wording, but clearly the Reserve Bank (RBA) noted in its most recent decision release that "continued low inflation would allow scope for easier policy, should that be appropriate...".

There are probably three things that would need to be in place for an interest rate cut, being a cooling of property investor lending (tentative tick), confirmation that hiring is weakening, and evidently confirmation of continued low inflation.

The Labour Force figures for March are due out on Thursday, and the market consensus sees a fairly moderate result as likely, with some clear risks to the unemployment rate reading, while the March inflation data is due out towards the end of the month.

There's a bit of water to flow under the bridge between now and then, but a nice bump in key commodity prices overnight and an incredibly strong result from NAB's Business Survey really don't point towards a rate cut at this stage.

A cracking NAB survey showed a surge in business conditions at their highest level in fully eight years since 2008, and while the employment gauge jumped to a five year high. Business conditions are now showing a reading of +12, absolutely miles above the long run average of +5, and capacity utilisation has improved strongly (I do note here, though, that the outlook for mining remains dire).

The RBA has arguably been a reluctant cutter through this cycle, so I reckon that rules out a May cut. In fact, interest rates could be on hold for as far as the eye can see.

As ever, happy to be proven wrong on that, though.

In my opinion there is very little value in comparing returns with the share market over a one or two year timeframe. Each asset class has its merits and place in a portfolio, but generally speaking property needs at least a ten year time horizon in order to justify the transaction costs.

The data yesterday confirmed that home loan activity levels - although not necessarily aggregate mortgage values - are rising solidly in Queensland, and this is readily visible in some of the family-friendly middle ring suburbs of Brisbane. Investor hubs are considerably patchier, and many of the resources regions are an absolute disaster zone.

A final point of interest for today is that markets had increasingly been lining up bets for an interest rate cut as soon as May, though I personally didn't like the odds of that happening.

I don't spend hours deliberating over monetary policy wording, but clearly the Reserve Bank (RBA) noted in its most recent decision release that "continued low inflation would allow scope for easier policy, should that be appropriate...".

There are probably three things that would need to be in place for an interest rate cut, being a cooling of property investor lending (tentative tick), confirmation that hiring is weakening, and evidently confirmation of continued low inflation.

The Labour Force figures for March are due out on Thursday, and the market consensus sees a fairly moderate result as likely, with some clear risks to the unemployment rate reading, while the March inflation data is due out towards the end of the month.

There's a bit of water to flow under the bridge between now and then, but a nice bump in key commodity prices overnight and an incredibly strong result from NAB's Business Survey really don't point towards a rate cut at this stage.

A cracking NAB survey showed a surge in business conditions at their highest level in fully eight years since 2008, and while the employment gauge jumped to a five year high. Business conditions are now showing a reading of +12, absolutely miles above the long run average of +5, and capacity utilisation has improved strongly (I do note here, though, that the outlook for mining remains dire).

The RBA has arguably been a reluctant cutter through this cycle, so I reckon that rules out a May cut. In fact, interest rates could be on hold for as far as the eye can see.

As ever, happy to be proven wrong on that, though.

PETE WARGENT is the co-founder of AllenWargent property buyers (London, Sydney) and a best-selling author and blogger.

His latest book is Four Green Houses and a Red Hotel.

Pete Wargent

Pete Wargent is the co-founder of BuyersBuyers.com.au, offering affordable homebuying assistance to all Australians, and a best-selling author and blogger.