Investment loans power on: Pete Wargent

APRA released its latest property exposures figures for the June 2015 quarter today, which confirmed an ongoing surge in new housing loans.

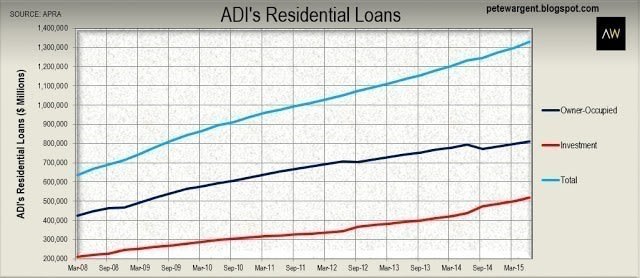

As at June 2015 the total of residential term loans to households held by all institutions (ADIs) was $1.33 trillion.

In total this represented an increase of +$31.8 billion (+2.4%) from the prior quarter, and a solid increase of +$97.1 billion (+7.9%) over the year to June.

There were a total of 5.4 million loans outstanding, with an average balance of $243,000.

Investment loans surging higher

Investment loans totalled $518.3 billion, an increase of +$17.7 billion (+3.5%) from the March quarter and massive +$81.1 billion (+18.6%) from one year ago.

That's huge, and well ahead of the rate that the regulator would or should be comfortable with.

Interestingly while loans held by the major banks increased by +7.5% over the past year to $1,076 billion, loans held by other domestic banks increased by a much faster +18.8% pace to $155 billion.

The major banks still accounted for close to 80 per cent of the domestic new housing loan market, however, with the remainder of the market comprising other banks, credit unions and particularly building societies.

It should be noted that there have been a few issues relating to the reclassification of loans between owner-occupied and investment loans, with material revisions (>10%) pushed through for the September 2014 to March 2015 quarters relating to ANZ and National Australia Bank.

You can see the jump in the chart below.

This has had the impact of accentuating the rate of increase in investment loans while dampening the growth in owner-occupier loans.

You can see the jump in the chart below.

This has had the impact of accentuating the rate of increase in investment loans while dampening the growth in owner-occupier loans.

In any case the trend in total loans outstanding since March 2008 has been more than clear, with total residential term loan exposures captured by this data more than doubling over that time.

This is at least partly because the investor segment of the market often opts to amass new debt rather than paying loan balances down, particularly because Australia has prevailing tax legislation which encourages this behaviour.

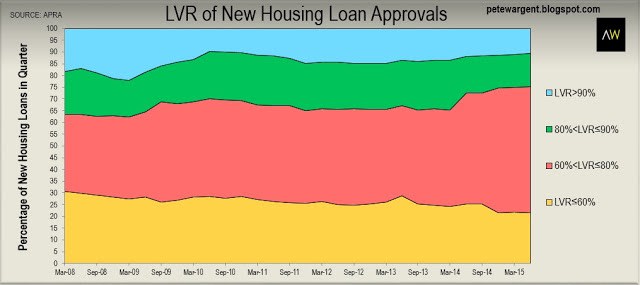

The data revealed that the overwhelming majority of new housing loans in the quarter at 89.3 per cent of new loans were of a loan to value ratio (LVR) of 90 per cent or lower.

As denoted by the pink area in the chart below there has been a surge in the number of borrowers using 20 to 40% deposits, now accounting for more than half of new housing loans in the last quarter.

This may imply that "cashed up" property owners with deep pools of equity are buying investment property at the expense of first time buyers who must save their deposits.

This may imply that "cashed up" property owners with deep pools of equity are buying investment property at the expense of first time buyers who must save their deposits.

More than one fifth of new loans in the quarter had a very low loan to value ratio of just 60% or lower.

Higher risk "low doc" loans continued to represent only a tiny fraction of the Australian mortgage market in the June quarter at 0.4 per cent.

Market risks

With very few low doc loans written and the overwhelming majority of loans being written with deposits ranging from 10 to 40 per cent, where lies the risk?

After all, it is hardly as though the market is highly leveraged in aggregate with around ~$1.4 trillion of debt sitting against a stonking $6 trillion residential housing market.

For my money, in terms of the residential mortgage market the answer is that the risk lies in the very high percentage and concentration of interest only loans, whereby typically no repayments are made against the principal in the first five years.

It is true that loans with offset facilities are continuing to flourish, but nevertheless a whopping 45.8% of new housing loans written in the June 2015 quarter were of the interest only variety.

Although only 4% of new housing loans in the June quarter were written outside serviceability, it would not be a surprise to see APRA looking more closely at the elevated percentage of interest only loans with renewed interest.

PETE WARGENT is the co-founder of AllenWargent property buyers (London, Sydney) and a best-selling author and blogger.

His latest book is Four Green Houses and a Red Hotel.

Pete Wargent

Pete Wargent is the co-founder of BuyersBuyers.com.au, offering affordable homebuying assistance to all Australians, and a best-selling author and blogger.