Reserve Bank muses on housing stress

The Reserve Bank of Australia (RBA) touches on some interesting points in its latest Financial Stability Review, including the paradox of low interest rates.

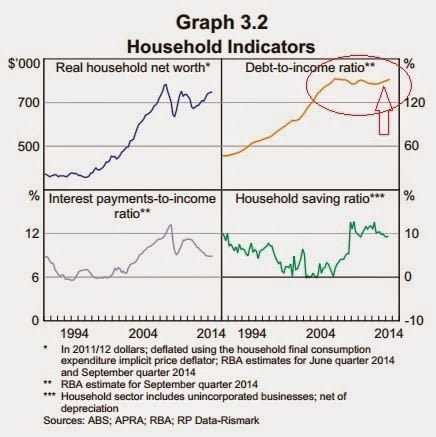

Household debt-to-income ratios have been flat for the past eight years, but the RBA quite rightly senses a risk that low rates could see this figure busting out to new highs and looks on cautiously.

The paradox is that low interest rates have made life pretty easy going for existing owners of property on variable rate mortgages, with the interest payments-to-income ratio falling from 13% to just 9%

Mortgage buffers

The RBA notes that aggregate mortgage buffers are at remarkably high levels, the equivalent of "more than two years" of scheduled repayments. A big reason for this, as I've experienced myself, is that banks have frequently left mortgage repayment amounts on auto-pilot despite declining mortgage rates:

"Households' ability to service their debt has been aided by ongoing low interest rates. The proportion of disposable income required to meet interest payments on household debt has stabilised accordingly, at around 9%.

"Households continue to take advantage of lower interest rates to pay down their mortgages more quickly than required. The aggregate mortgage buffer – balances in mortgage offset and redraw facilities – has risen to be around 15% of outstanding balances, which is equivalent to more than two years of scheduled repayments at current interest rates.

"Prepayment rates and the proportion of borrowers ahead of schedule on their mortgage repayments are also high according to liaison with banks. Part of this prepayment behaviour has been due to some banks' systems not automatically changing customer repayment amounts as interest rates have declined, while in many cases households have not actively sought to reduce their repayments.

"This might be a sign that household stress is currently limited. The household saving ratio, although trending down a little lately, remains high at just under 10%. Households' aggregate balance sheet position has continued to improve in recent quarters: real net worth per household is estimated to have increased by 4% over the year to September 2014."

Rental market

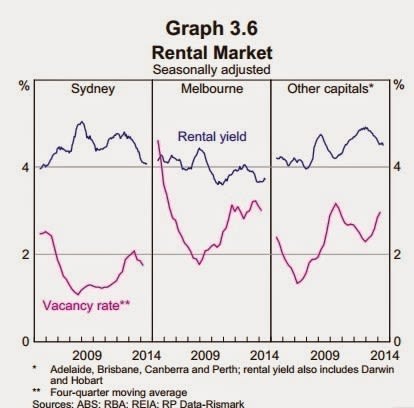

With dwelling prices rising we might expect to see rental vacancies increasing and yields declining. Historically speaking, however, Sydney's vacancy rate remains low despite pockets of forthcoming oversupply. RBA again:

"Despite the activity and housing price inflation in the Sydney and Melbourne property markets, rental yields have not declined to a significant extent and vacancy rates in these cities remain fairly low."

True, but vacancy rates are elevated and likely to rise in inner city Melbourne apartments as the RBA observes.

Household financial stress?

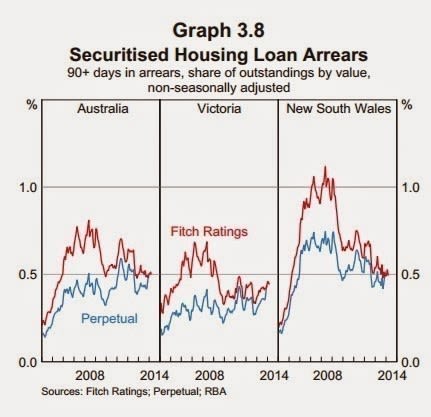

Generally 90 day+ loan arrears at now at very low levels at only 0.5 percent, but there are some indicators of household financial stress in Victoria. Back to the RBA:

"Aggregate indicators suggest that household financial stress is generally low, despite the increase in the unemployment rate over the past year. The share of banks' housing loans that are non-performing has declined for both owner-occupiers and investors since reaching a peak in the middle of 2011.

"Data on securitised housing loans show that the share that are 90 days or more past due has declined over the year for most states, coinciding with lower interest rates and rising housing prices. In Victoria, however, loan performance has deteriorated slightly."

The RBA notes instances of mortgage stress and arrears in "outer west and north Melbourne".

Interest rate rises?

So it's largely happy days for homeowners at present. But what about interest rate increases?

Previously we have covered off the possibility here that interest rates might yet fall further as the mining construction boom tails off.

So, what could lead to hikes? Mostly we'll be looking at inflation and the jobs market.

The TD-MI inflation gauge printed flat again for the month, leaving this particular measure sliding towards the bottom of the 2-3% range (now at just 2.2%) and suggesting little in the way of inflationary pressures or a pressing need to hike interest rates.

The declining Aussie dollar could well wash through a little more tradables inflation in due course, but sustained inflationary pressure would likely need the labour market to pick up, since there currently appears to be a fair amount of slack therein.

Some heartening news on that front today with ANZ job adverts recording its fourth consecutive monthly gain to hit its best reading in two years.

Could this suggest that the labour market is picking up as was suggested here by last month's figures? Maybe! The next round of Labour Force figures on the 9th of this month is very eagerly anticipated for all of the above reasons.

In any case, interest rates will be very much stuck on hold today at 2.50%. It seems likely that prudent households will have at least another year of low rates ahead to keep building up those mortgage buffers.