The demographics of dual income couples

While it's an interesting exercise to draw property market charts back to the middle decades of the 1800s, it doesn't really help us to draw any logical conclusions about the future.

There is little comparison to be drawn from the slums in The Rocks of the 1900s where an outbreak of the bubonic plague was killing residents and the modern housing of today.

That would be like comparing Ken Rosewall to Rafa Nadal and concluding that Rosewall was rubbish. He wasn't, of course, but the rules have changed.

Perhaps a more useful starting point for housing market data would be 1986, which is when lending markets in Australia were deregulated in a sweeping move which won't be reversed.

A few other things have changed since then too.

I was reading a book on commercial property yesterday written in 2003, which anticipated that Australia's population could "swell" to 25 million by 2051.

Well, we're well past 23.5 million already in 2014 and heading towards a projected 40 million or so by the middle of the century.

That's one major shift.

Another has been the huge change in borrowing rates. Today it's possible to borrow for housing a rate close to 4.50%, which is unfathomably low as compared to 25 years ago.

Anyway, we've looked at the role of lending deregulation before.

Today let's consider...

Gender

Another major demographic shift in the last few decades has been the increasing role of females in the workforce.

This impacts property markets because there has been a dramatic increase in the number of dual income households which boosts purchasing power and loads the dice in favour of the couple with two incomes and over the single income household.

This is where it's important to consider some specifics if you are looking at buying a property.

Phrases like "many young people want to live near the city" and "many young people look at apartments" may indeed be true, but they are so generic that they don't really tell you a lot.

Similarly, saying that "there are many more dual income households" may also be correct, but it doesn't really tell you much about the impact on property markets unless you drill down to a localised level.

Demographics by suburb

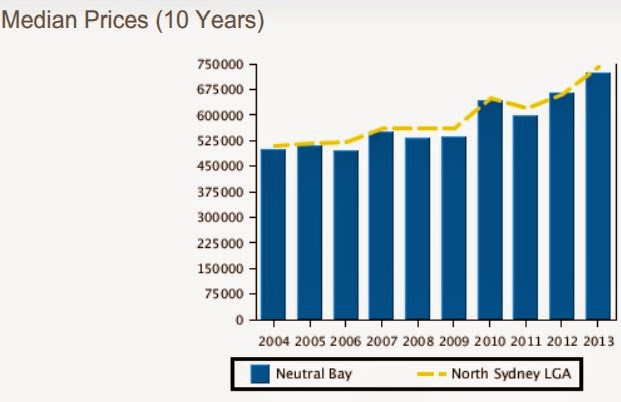

Let's say I'm looking at buying an investment property in a prestige leafy harbourside suburb in Sydney such as Neutral Bay, which is one of the locations I bought in last year. That's around 10 minutesto the Opera House and Circular Quay on the ferry.

First, I'd take a look at the demographics of the suburb. The data below is from RP Data, but you can use other sources if you prefer.

This gives me a good idea of my target tenant.

Intuition already tells me that it would most likely be a professional couple in a similar age bracket to myself, and the data says...yep, pretty much, 25-34 year olds are probably the go.

Source: RP Data

Note the impact of the dual income household in Neutral Bay, where the most households are in the $130,000-$180,000 household income bracket.

If you live in central Sydney, a lot of this is stuff is partly intuitive. In the type of inner suburb apartment blocks I've lived in over the years, the overwhelming majority are let to young two-income couples who work in or near the city.

What the demographics of the suburb also tell me is that the target entry price for an apartment would likely be $650,000 to $750,000.

That way, even couples with heavily geared 80% loans should still be able to service their mortgages in the unlikely event that standard variable borrowing rates return to 10% any time soon.

In that price bracket you'd likely be looking at a quality two bedroom apartment on a quiet street with parking, and ideally harbour or district views.

Prolonged high levels of unemployment is a different issue for housing markets.

The longer term data tells me that the population of Neutral Bay has not increased at all between Censuses (it actually fell a little last time around) because the supply of new dwellings has been almost totally capped.

The demand for housing in a glistening, prestige harbourside suburb will easily outstrip the available supply over the long term simply because there is very little new supply.

Median apartment prices have not done anything particularly spectacular, moreover they have simply tracked the growth in housheold incomes over the past decade, appreciating at around 4% per annum on average.

There will certainly be downturns in a suburb like Neutral Bay as there are anywhere, but they are unlikely to be severe in the price range identified above. The replacement cost of apartments is high, and a downturn in prices would likely quickly be met by new demand.

Naturally, you could alternatively look at a house in the suburb but the entry point would likely be very high at $1.5 million plus. The long-term capital growth outcome would likely be great, but the ride would be more volatile and the holding costs more painful.

Clearly, we're looking at a prestige Sydney harbourside suburb scenario here. If you were looking at investing in a distant location somewhere west of Narromine rather than Neutral Bay, you would be looking at different demographics and income profiles, and therefore a necessarily lower entry price.

You can visit AllenWargent property buyers (London, Sydney) or Pete's blog.

His new book 'Four Green Houses and a Red Hotel' is out now.