The three reasons why first home buyer numbers will be strong enough in 2014

Recently released figures implied that the percentage of first home buyers in the market fell from 12.5% in December 2012 to just 10.2% in December 2013, before bouncing a little to 11.2% in January 2014.

I could be proven wrong of course (it's been known!) but I'm pretty confident that the number of first home buyers will be strong enough in 2014. While we're all guilty of at times looking for evidence to support our own preconceptions, today I'll discuss why it is that I think that.

Data from AFG's mortgage index in January showed that the level of first home buyers (FHBs) was strong in Western Australia (up from 21.8% to 24.2%), pretty good in South Australia (15.5%) and increased in Victoria (up from 8.7% to 11.2%).However, the data showed that in states with no first home buyer grants the level of FHBs was exceptionally low; such as in Queensland (6.5%) and New South Wales (3.4%). The Reserve Bank's chart below shows how the market looks in historical terms, with the distorting impact of previous grants clearly evident.

Here are three of the reasons I believe that FHB levels will be strong enough in 2014.

1 - Finance won't get any easier than this

Loan products are now available from just 5.79% per annum interest for first home buyers with only a 5% deposit and with no Lenders Mortgage Insurance to be charged. I also just saw a TV advert for 95% first home buyer loans with parental guarantee. When stuff like this starts hitting the popular media, it's a sign of changing sentiments.Financing probably won't (perhaps I should rephrase that - probably shouldn't) get any easier than this.

Yes, 100% LVR loans were available to first home buyers prior to the financial crisis, but to date I haven't seen or heard any market commentator suggest that the widespread return of 100% FHB mortgages would be a good idea.

Declining lending standards add fuel to markets that are already inclined to be irrational and are likely to lead to financial instability. Encouraging buyers with no track record of saving to leverage up when interest rates are at generational lows, could easily lead to a proliferation of non-performing loans down the track.

In any case, while previously available 100% mortgages may have been great for those who used them, the appeal must have been somewhat diminished by being slugged by up to $15,000 (or on occasions even more) of lenders mortgage insurance (LMI), even if it was possible to capitalise the amount charged into the loan balance. This can leave buyers in an immediate negative equity position - not at all desirable!

2 - Cyclical markets

It may not feel it at times, but ultimately markets are cyclical. Over in Britain, we heard people over the last six years saying that an entire generation of younger buyers were in the process of being locked out of home ownership...and yet today an astonishing 44% of mortgage activity is for first home buyers. To all intents and purposes, this is as high a reading as we've ever seen.

Investors tend to be less in favour of buying into rising markets, while first timers are probably more inclined to buy into the market as it rises for fear of missing out. This is exactly what is happening in Britain in 2014, where first home buyers are now jumping aboard after prices increased by close to 9% in 2013.

As counter-cyclical investors, we were largely buying between 2010 and 2012 when sentiment was extremely despondent, and while it's not possible to consistently, median prices will race on to new highs in 2014.

There is, of course, ultimately a speed limit on asset prices. Property markets can't continue to appreciate in perpetuity beyond the capability of buyers to finance acquisitions. Therefore while it may take time for markets like London, Melbourne Sydney to come back to some kind of normality, over the medium term markets are likely to be to a certain extent self-correcting.

Article continues on next page. Please click below.

3 - Incomplete records

As I note below, the non-recording of first home buyers in states such as New South Wales, has been discussed for more than a year in various chat fora.

Having spent the Pommie summer (or at least, the short period of time which passes as an excuse for summer over there) in our London office, I've been a little out of the loop, but over the past six months I've now had dealings with a few first home buyers in Sydney. Clearly, with offices in Mayfair and Martin Place, our target clients are higher-income earners and investment funds. Nevertheless, I have had some FHB interaction.

Last month, I engaged with a first home buying couple and enquired out of interest whether they had registered as such when obtaining finance. Their response was along the lines of: "No, why would we do that?" Which pretty much sums up the current situation.

Before Christmas I worked with another first time buyer who had chosen to buy an investment property as their first move onto the housing ladder, and as such they weren't recorded as a first-time buyer either. Buying a rental property first also appears likely to be an increasing trend, as younger generations change jobs and careers far more quickly than has ever been the case before.

Now granted, the sum total of my experiences in NSW with first home buyers over the last half year – at only four – is not nearly enough to conclude anything with statistical significance. But given that in all four cases the data has not recorded the buyers as FHBs, it's enough for me to conclude that the system ain't working.

To be frank, I'm not even sure how this issue gets resolved, short of a directive to mortgage brokers from a regulatory body or other changes to the existing system? Answers on a postcard. However, for now, I can't see how a reading of above 24% in Western Australia and 3.4% in New South Wales makes any kind of sense to anyone who is analysing the data objectively.

Some observations of the first home buyer experience

One observation I have to add from my dealings with first homebuyers over the last six months is that today the real estate market dice are fully loaded in favour of dual income households.

Saving a 5% deposit seems to be an achievable enough task for a couple; whereby one of the incomes can be used to pay for rent, food, living costs and luxuries, and the second income can be socked away for a deposit. Clearly, this is not nearly as easy a prospect for a single income earner, particularly in the younger and lower income-earning years.

Another factor which has distorted the savings process in recent times has been a necessarily increased dependence on debt to fund higher education, leading potential first home buyers towards mixed priorities. Should one clear the tranche of liabilities related to education costs before embarking on the next level of indebtedness?

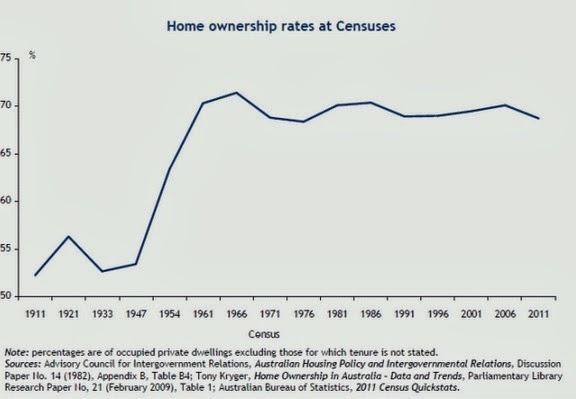

Home ownership rates have been remarkably stable in Australia for the past half century. However, it strikes me as very likely that our comparatively high rates of home ownership will begin to decline to levels seen in other developed countries, as Australia's population explosion continues and as people do practically everything later in life than they used to.

However, absent significant changes to the prevailing system (e.g. a major tax reform which makes ownership less appealing than renting) most Australians will likely continue to aspire to get onto the housing ladder one day. For that reason it seems probable that the market will remain robust in most well-located capital city suburbs over the longer term.

His new book 'Four Green Houses and a Red Hotel' is out now.