ABS building activity data revisions point to positive signs for the economy: Pete Wargent

It's well known that some commentators have been going on and on (and on) about the risk that Australia will sink into recession.

Australia's GDP growth is bumbling along at a trend of 2.6% per annum or a seasonally adjusted 2.5% p.a.

The bearish excitement reached fever pitch when in the last quarter Australia's GDP was again reported at just 0.6% for the 3 months to March, suggesting a possible forthcoming downward trend.

GDP growth:

Source: ABS

Not a great result, but monetary policy takes time to see its full results, and, after all, 0.6% is still growth, even if it is not considered to be strong growth.

The March GDP result of 0.6% was quite some way lower than had been initially forecast, but I remarked at the time that there remains every chance that the figure could be revised upwards. And if that were to be combined with a half-decent result for the June quarter, we could yet come in at closer to 3% per annum than 2.5% for the year to June 2013, thus leaving us wondering what all the fuss was about.

Furthermore, last week's inflation figures revealed one piece of gratifying news - the mining construction boom has not left Australia with an inflation problem, such as has been the case when booms have been experienced.

Strip out the effect of the carbon price, and annualised inflation actually sits below the targeted 2-3% range (and thus ultra-low interest rates may be maintained).

And so to the building activity figures released this month.

Again, not a great set of results, although dwelling units commenced increased over the past year for both houses (+5%) and units (+21%) implying that the Reserve Bank's stated plan to stimulate dwelling construction may be beginning to take some sort of shape.

Dwelling units commenced:

Source: ABS

In all the excitement of highlighting the soft year-on-year building activity figures, very little weight was given to the following note in the Building Activity release.

Significant revisions to this issue:

the total value of work done in Australia during December quarter 2012 has been revised upwards by $582.1m or 2.8%.

the total value of work commenced in Australia during December quarter 2012 has been revised upwards by $1,790.9m or 8.8%. This was driven by revisions to non-residential commencements ($844.4m) and new other residential commencements ($621.5m).

the number of dwelling unit commencements in the December quarter 2012 has been revised upwards by 3326 dwellings or 8.4%.

All revisions to the December 2012 quarter's figures and all of them in one direction: upwards.

It's also interesting to note that actual capital expenditure undershot expectations in the March quarter in falling by 4.4%, so it will be very interesting to see what is reported for the June quarter on August 29.

There may be implications for GDP growth which could result in upward revisions.

The Reserve Bank will have been heartened by a major correction to the currency, with the Aussie dollar having devalued markedly against the US dollar since the middle of April, as well as a decent rebound in the iron ore price.

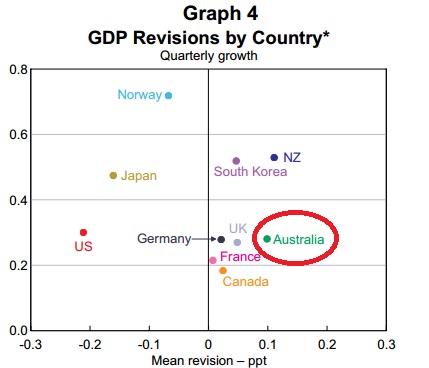

Detailed research by the Reserve Bank shows that over the past 15 years, Australia, just like our buddies from across the Tasman, has a tendency to revise its GDP figures in an upwards direction.

Source: RBA

While the biggest absolute revisions to GDP tend to be driven by the highly unpredictable inputs such as change in inventories (by its very nature an "extremely volatile series") and corporate profits (ditto), the RBA's research shows that drivers of revisions in the past have also included household consumption, dwelling investment, engineering and construction, and non-residential building.

The RBA has highlighted that its real time GDP prints can be subject to significant revisions and that early estimates of GDP tend to undershoot the 'final' results to some degree.

"Revisions to early estimates of GDP growth have tended to be sizeable and in an upwards direction, though these characteristics are not unusual by international standards."

Of course, some will continue to highlight every risk facing our economy and every negative angle they can possibly find until the day they drop off: it's their job; after all, gloom-peddling is a mini-industry in itself these days.

But keep any eye out for what happens over the next six weeks, especially now that we have seen building activity figures for previous periods revised upwards.

Could we end up with GDP for the financial year of closer to 3% than 2.5% when the National Accounts are released in early September?

There may yet be a surprise to the upside.

Pete Wargent holds a range of finance and property qualifications and is the author of Get a Financial Grip – a simple plan for financial freedom.