Why the November RBA meeting may be live: Pete Wargent

EXPERT OBSERVER

Market mispricing?

If you'll kindly indulge a Tuesday night blog post after an evening talking, um, Australian monetary policy at the Clock Hotel (n.b. soft drinks only!), then herewith it follows.

One week ago the October 2019 RBA Minutes were released, and they stated that, if needed, policy would be eased further to achieve full employment and the inflation target.

Source: RBA

Then on October 18 the RBA Governor delivered a designedly upbeat speech to the IMF in Washington, which justifiably highlighted Australia's record unbroken stretch of economic growth among other Antipodean successes (including the floating currency, which often - though not always - moves in harmony with commodity prices).

I didn't listen to the audio live, but while we don't need to link to all of the media pieces, across the board we saw a rash of articles suggesting that the RBA is done with cutting and has hosed down the prospect of further cuts.

A bit odd, it seemed.

A bit odd, it seemed.

I'll come back to this point, but I broke one of my own golden rules here: at the risk of sounding like an episode of Yes, Prime Minister, always listen to what was actually said, not what was said about what was being said!

Inflation smoked

The latest employment figures were modestly positive, but the leading indicators are weakening and there was no indication that labour force slack will be reduced significantly, or that full employment will be on the horizon any time soon.

Unemployment was still uppish at 5.2 per cent, and the underemployment rate remained way high at 8.3 per cent.

Looking towards next Wednesday's inflation figures for the September quarter, it's hard to see where any inflationary pressures at all are going to come from, except for - yet again - smokes.

There may well be some food price inflation due to the drought (which itself drags further on economic growth), but rental price growth will be at or close to record lows, and there may be some other offsetting factors.

Crunching through the numbers, with a hat tip to the ever-brilliant Justin Smirk at Westpac, spits out trimmed mean inflation of, say, 0.3 per cent, and the weighted median may well be even lower still.

So that gets you to annual core inflation of about 1½ per cent for trimmed mean, and just 1.2 per cent for the weighted median, which is so far below the mandated target you could drive a truck through the gap (or an attractively priced new SUV the way new car sales have been tracking!).

If all of this proves to be the case - and, by the way, the mid-point of the inflation target is 2½ per cent - why wouldn't the RBA be cutting with bells on?

Financial markets have effectively priced out a November cut - and almost any further cuts at all - as far as I can tell because some people said that's what the Governor said...but is that what was said?

What's the French word for nuance?

To recap briefly, we have a 'no' to full employment, and a resounding 'no' for being close to achieving the inflation target, which market expectations see as a distant dream.

Now let's go back to the IMF speech, and more specifically the very brief Q&A segment.

And then to a question from the floor!

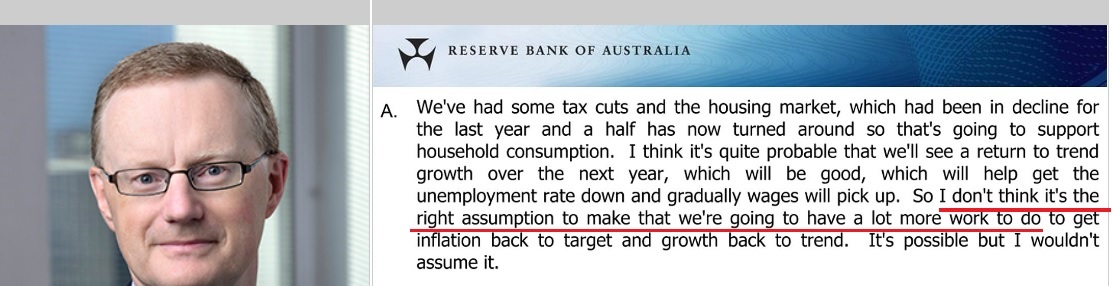

Question: has the RBA got 'a lot of work to do' in terms of delivering monetary easing (the cash rate is at 0.75 per cent), and should we assume negative rates or other unorthodox policies?

Question: has the RBA got 'a lot of work to do' in terms of delivering monetary easing (the cash rate is at 0.75 per cent), and should we assume negative rates or other unorthodox policies?

Source: RBA

To my mind, there's only one way that a central bank Governor could've answered that question given the circumstances, and here it is:

Source: RBA

November live

Now I could be off beam here - it's happened on this blog at least once before! - but this answer, and perhaps some of the remainder of the transcript might have been misinterpreted...and the market pricing may in turn have been led astray.

No central banker could have reasonably responded 'we have lots more to do' on easing, and the question on negative interest rates was always going to be batted to the fence, which it quite rightly was.

The consensus view is that there will be no further easing this year, but if inflation is as low as it looks to be - essentially a sin tax on tobacco and a bit of drought-related food price inflation - then the November meeting could be a live one.

I've leaned heavily here on the analysis of Sophia Rodrigues of Central Bank Intel (if you're an institution you should subscribe to her forthcoming content), and another prominent markets analyst in Sydney (well, it's the Clock Hotel, you can work it out).

I've leaned heavily here on the analysis of Sophia Rodrigues of Central Bank Intel (if you're an institution you should subscribe to her forthcoming content), and another prominent markets analyst in Sydney (well, it's the Clock Hotel, you can work it out).

Pete Wargent

Pete Wargent is the co-founder of BuyersBuyers.com.au, offering affordable homebuying assistance to all Australians, and a best-selling author and blogger.