Mining construction in sharp decline: What does it mean for our regional property markets?

The latest round of ABS Engineering Construction data for the third quarter of 2014 - a fair proxy for mining and resources project construction - showed another sharp decline.

Let's take a look at what we can learn in three short parts.

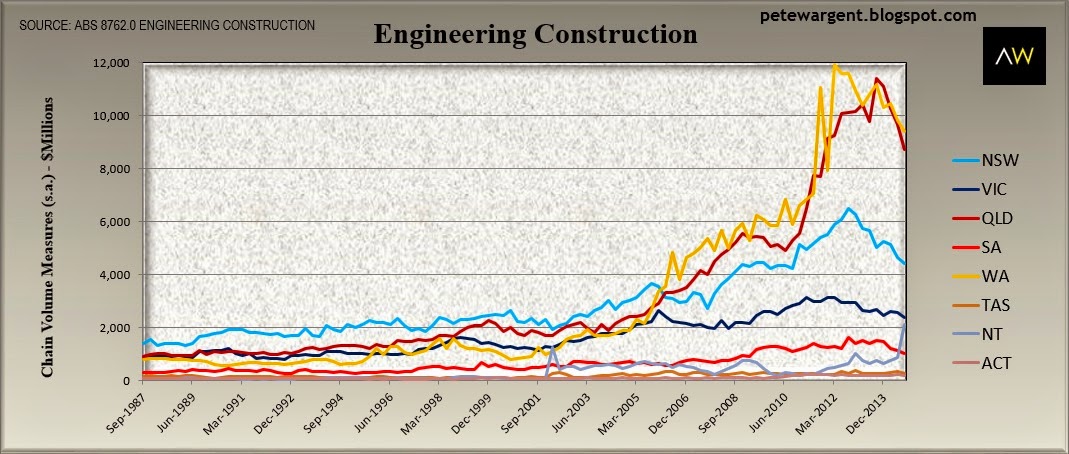

Part one - Engineering activity tanks

Engineering construction activity dived by 3.7% to $28,394 million in the third quarter in chain volume measures terms to be some 13.3% lower than a year ago.

After an extraordinary run mining construction is set to act as a material drag on the economy over the next few years as activity reverts back towards its long run average. Given recent market action in the commodities sector, the decline could be pretty rapid.

While Western Australia and Queensland are busily ramping up export volumes, at the same time construction activity is dropping off a cliff. In fact only the Northern Territory has seen a mining construction activity spike of late, partly due to some big spend on the Inpex Ichthys LNG project.

It isn't possible to forecast with any level of accuracy what will happen to mining construction in any given reporting period, but the first chart above shows that total activity is likely to have a long way to fall yet.

Capex intention surveys do suggest that there is likely to be an uplift in investment in other industries. However, the engineering construction work commenced figures, which are always necessarily wildly volatile by their very nature, show that work commenced in the third quarter was well down on a rolling annual basis.

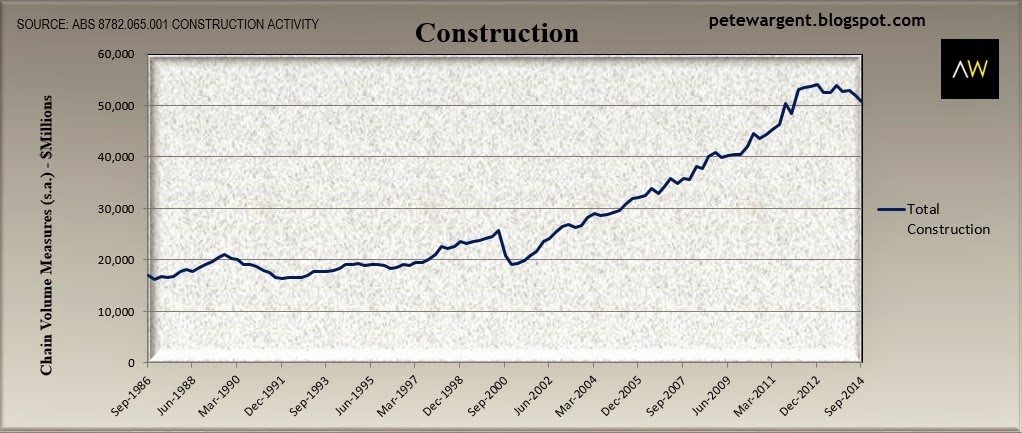

Part two - All change in construction sector

During the past week we already noted that the value of building activity for the third quarter came in at an underwhelming $22,287 million, although this did represent a moderate 5% increase over the past year.

The good news was that there were an all-time record 52,380 home starts in the September quarter, so there will surely be a marked uplift in residential building to follow in the year ahead.

The above chart shows that even if residential construction can ramp up by a couple of billion in 2015, this alone cannot offset the likely decline in mining activity and there will be more lifting to be done elsewhere in the economy.

Piecing this all together, total construction activity in the ABS data series declined by 2.5% over the quarter and 6% over the past year.

Article continues on the next page. Please click below.

Part three - Macro trends to watch in 2015

So what can we expect to see as a result of this? Here are three macro trends to watch out for.

- i) Interest rates to fall to 2%

We have had two strong employment reports over the past two months - at least, we have on a dubious seasonally adjusted basis - but it would be a brave call at this stage to suggest that interest rates are not heading lower in 2015 given the collapse in engineering construction work in the pipeline.

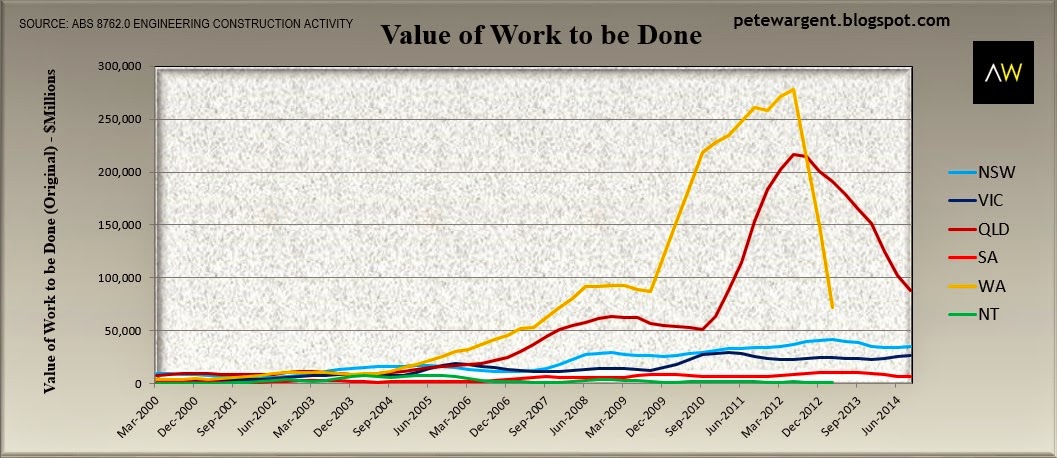

There are no complete and up-to-date figures available for Western Australia (or the Northern Territory for that matter) but the underlying data available for categories such as roads and highways points towards an ongoing decline.

Futures markets are therefore all but pricing in two interest rate cuts by H1 2016 which may well give a few of Australia's floundering property markets a timely boost.

- (ii) Mass migration back to capital cities

Recent demographic studies have shown that a migration back towards the capitals is already well underway with both population growth and employment growth increasingly focussed around the centre of our four largest capital cities, and regional population growth in most locations well below the national averages.

The construction phase of the mining boom is the labour-intensive phase - labour required for new mines and LNG projects is typically only a third of that needed through the project construction stage.

This need not all be doom and gloom. For one thing resources export volumes are punching out record highs by the month (albeit with diminished commodity prices) which is, after all, the point of the preceding mining and resources construction boom.

The Reserve Bank of Australia has also released detailed research to outline its rationale for believing that mining construction employment skills are directly transferrable to residential property construction - and remember 2015 and 2016 will be record years for the building of housing.

The RBA's figures show that the number of construction workers alone in the resources sector leapt from around 15,000 in the mid 2000s to around 90,000 by 2013. We can expect to see an equivalent retrenchment as resources projects are completed, with some 60,000 resources construction positions to be terminated between 2014 and 2018.

Offsetting this around 20,000 operational positions were created in 2013 and 2014 with another 10,000 to come ove rthe next few years. Totting that up net resources employment is set to decline by about 40,000 between 2014 and 2018.

Residential construction boom

The good news is that the latest residential building approvals hit their highest ever level at nearly 200,000 on a rolling annual basis up to November 2014.

The ensuing residential construction boom will be predominantly a capital city affair, with the capital cities approvinga combined record 74,397 houses and 75,320 units over the past year. Thus more than 75% of dwellings constructed will be in the capital cities and more than two thirds of them in only Greater Sydney, Melbourne, Brisbane and Perth.

This is important for the respective economies of those four cities since residential construction has such as healthy economic multiplier effect.

- (iii) Regional property markets to underperform in aggregate

"Location, location, location" is one of the greatest cliches in real estate, but like many such mantras it has a grain of truth in it.

Over the long-term, well located capital city property will generally outperform regional centres where economic growth and the expansion of household wealth tends to be less robust or diverse.

For a while it was claimed that regional centres could even record the same average price growth as landlocked capital city suburbs - and indeed, as Australian households went on a one-off debt binge as interest rates fell this was true for a while, although the debt expansion binge ended fairly abruptly around 2007.

There are some exceptions to this rule, of course - Queensland has been home to a number of thriving regional centres, for example. But generally studies have shown that our large capital cities are the wealth-creating engines of Australia's growing economy and house price growth tends to be stronger close to the centre of cities.

It is the case that many parts of regional Australia have benefited from a surge in employment during the once-in-a-century mining construction boom - one which lasted much longer than many of us expected.

However that boom has now officially ended and less of the economic value from the export phase of the boom will be captured by the regions as employment levels fall into decline.

Instead as export tonnages ramp up vast sums accrue into state-level royalty offices, while dividend returns frequently leak to overseas shareholders or head office executives back in the capital city ivory towers, wolfishly raking it in from their latest ZEPOs.

PETE WARGENT is the co-founder of AllenWargent property buyers (London, Sydney) and a best-selling author and blogger.

His new book 'Four Green Houses and a Red Hotel' is out now.