An interesting speech from Dr. Christopher Kent, Assistant Governor of the Reserve Bank of Australia (RBA) in Canberra.

The speech noted that household consumption has responded to low interest rates since 2013, but in a less strong manner than might have been expected.

Let's take a look at three of the main observations raised...

Part 1 - The balance sheet and wealth channels ("aka. Equity withdrawal, mate")

Let's take a look at three of the main observations raised...

Part 1 - The balance sheet and wealth channels ("aka. Equity withdrawal, mate")

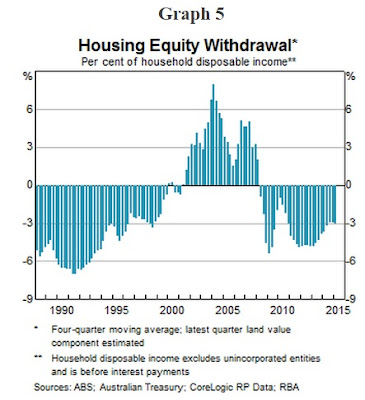

One of the drivers for a less strong consumption response through this cycle has been the diminished role of housing equity withdrawal.

In the first half of the 2000s households withdrew significant equity to finance their consumption, but this no longer appears to be occurring on such a widespread basis, according to the Reserve Bank's data.

In fact in recent years household net spending on assets has exceeding borrowing.

The evidence here suggests that the so-termed "wealth channel" - rising household wealth boosting consumption - has not been as effective to date as in cycles past.

Part 2 - The cash-flow channel - household balance sheets and buffers

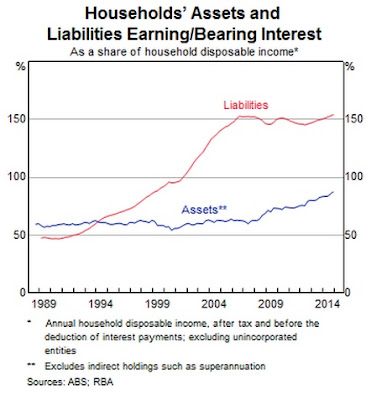

Of course, it is well known that Australian households are net borrowers on average.

However, the RBA's figures also show that while households' interest earning assets (such as bank deposits) have risen strongly as a share of disposable income over recent years - even exclusive of superannuation - interest bearing liabilities have not.

In fact, household liabilities as a share of household disposable incomes have been steady for some years now.

How so? This is thanks in part to record low borrowing rates, with aggregate mortgage buffers apparently soaring to record levels and many households evidently electing to pay down their debt faster, known as "deleveraging".

I believe that this is in part due a mechanism whereby mortgage repayments are held steady even in the event of downward adjustments to interest rates on variable rate products, something which is perhaps unique to Australia.

Average mortgage prepayments are rapidly approaching an incredible 30 months, while as a share of housing loans outstanding aggregate mortgage buffers have soared to well over 15 per cent, which is remarkable if true.

In short, through this interest rate easing cycle more households appear to have moved further ahead on their mortgage repayments.

It is often said that Australians are holding "record high" household debt, but the Reserve Bank charts claim that this fails to acknowledge the increasing role of offset accounts and investor credit.

When offsets and credit are included in the statistics household credit as a percentage of household income has actually declined by 4 percentage points over the past half decade, noted Dr. Kent.

Part 3 - The supply side

As is typical, dwelling construction, being the most interest rate sensitive sector of the Australian economy, is responding strongly to easier monetary policy, with building approvals now at their highest level on record and dwelling investment up by 9 per cent over the past year.

This will likely put downward pressure on apartment rents and prices in some regions.

However, one eminent challenge is that the supply of greenfield land in the Sydney region (inclusive of Newcastle and Wollongong) in particular, and also in south-east Queensland (Brisbane, Gold Coast, Sunshine Coast), has plummeted to extremely low levels, which is putting significant upwards pressure on land values.

In Sydney the stock of suitable sites for apartments has been depleted too in recent years.

With a dearth of suitable sites to build either houses or apartments, the Reserve notes the risk of a material spike in dwelling prices caused by the inadequate supply.

With a dearth of suitable sites to build either houses or apartments, the Reserve notes the risk of a material spike in dwelling prices caused by the inadequate supply.

A parallel challenge is that with the residential construction industry pushing towards full capacity, this is likely to result in inflation of land and construction work, potentially "pushing up the prices of new and existing dwellings, via increases in land prices, construction wages, developers' margins or some combination of all three".

While labour shortages have not bitten particularly hard to date despite some skills shortages arising, rising demand for building materials has already pushed the rate of inflation for new dwelling costs fully two points above its average for the inflation-targeting period (i.e. since 1993).

This is somewhat agitating since the residential construction boom is still in its infancy, relatively speaking.

Furthermore, alterations and additions (i.e. major renovations work) could easily pick up further, further accentuating materials shortages.

The wrap

Dr. Kent's speech concluded that consumption has picked up in Australia since 2013, and monetary policy is working as it should, to some extent.

However, many households are also electing to pay down their debts faster, and this is having some dampening effect on the strength of the consumption response experienced to date.

PETE WARGENT is the co-founder of AllenWargent property buyers (London, Sydney) and a best-selling author and blogger.

His latest book is Four Green Houses and a Red Hotel.