How my 2014 property market forecasts fared

A lot of water has flowed under the bridge since we issued our calendar year 2014 property market forecasts in November 2013.

To re-cap these were for various reasons generally softer than those projected by most analysts, alphabetically as follows:

No forecast was made for Darwin - as a former resident of the "Top End", personally I remain fairly unconvinced as to whether worthwhile forecasts are even possible in such a market.

Regular readers will be aware that we have been tracking progress throughout the year against RP Data's Home Value Index. Let's take a quick look how many hits and misses we'll score for 2014 and the reasons for them.

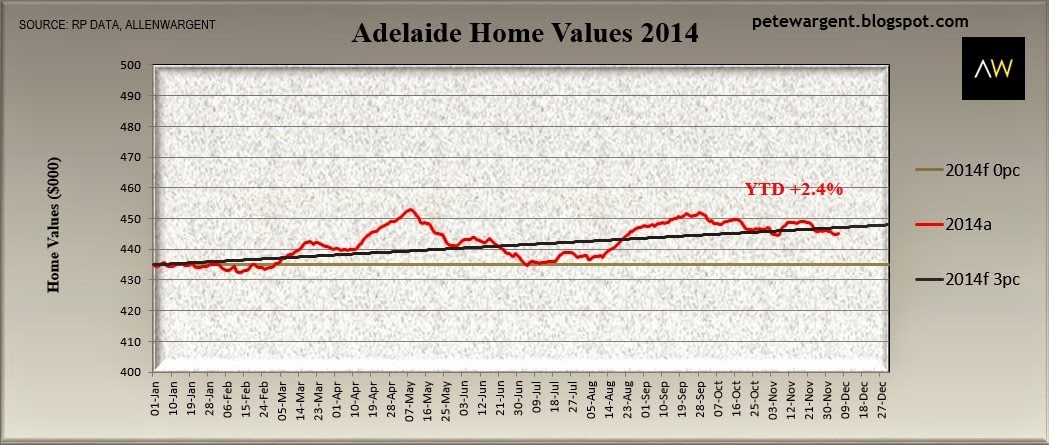

Adelaide (Forecast 0-3%)

Adelaide (Forecast 0-3%)

I've taken an increased interest in Adelaide since working down there in 2008.

Adelaide is usually a favourite pick for many property analysts, and continues to be, but our 2013 chart packs again pointed towards a struggling local economy with ongoing flat employment growth and only a tiny positive momentum in owner-occupier housing finance, while investor activity has remained fairly muted in South Australia over the longer term also.

Adelaide has relatively weak population growth and is comparatively speaking a less dense city, and thus should comfortably be able to manage a responsive supply. Wages growth has been solid but concerningly the local economy also faces some serious headwinds too as the car manufacturing industry closes.

The lowest interest rates in a generation could yet shunt prices a little higher, and sales volumes have certainly improved during this year, but land release new building should also easily be able to prevent booms in prices. Year to date price growth of 2.4% is well within our forecast range.

Verdict: Hit. Brisbane (Forecast 2-5%)

Brisbane (Forecast 2-5%)

Our owner-occupier housing finance chart packs showed Brisbane identifiably turning a corner in Q3 2012 on a rolling annual basis, and momentum building steadily but surely ever since.

This trend was clearly consistent with a gradually recovering market, which is exactly what we've seen play out this year.

Our latest 2014 chart packs suggest more of the same in 2015 too, with investor finance also now steadily picking up over a long period of time to its strongest level since 2007, and, importantly, at a slightly faster clip since Q3 2013 on a rolling annual basis.

Population growth will be slower in Brisbane in 2015 largely due to net interstate migration as the mining construction boom unwinds but this is likely to be offset by further interest from interstate investors.

A word of warning, though. There is a large volume of construction in the pipeline for attached dwellings and asset selection will be vital in this era of low inflation. If you buy generic new or off the plan high apartment stock without due consideration, then you will do so at your own risk.

Year to date growth in Brisbane has been within our forecast range.

Verdict: Hit.

Article continues on the next page. Please click below.

Canberra (Forecast -1 to -4%)

Canberra (Forecast -1 to -4%)

Our forecast range for Canberra of negative growth was a reflection of expected trends in the labour force due to projected rationalisation.

RP Data's index does not provide us with daily data to provide the picture through the year, but year to date growth up to November has been stone dead flat at 0%.

The Canberra market is now clearly in decline, posting a drop of 0.5% in November to record a horrible 3.3% loss over the quarter.

This is consistent with what other data providers such as Residex have seen playing out for the Australian Capital Territory over the past year and with the market now in decline this strongly suggests that by the end of the 2014 calendar year we will have seen a negative result for Canberra.

In many respects Canberra is an artificial property market. High average disposable incomes and an artificial land scarcity due to restrictions and constraints on zoning.

Verdict: Hit.

Hobart (-1% to +2%)

Hobart (-1% to +2%)

Tasmanian property markets have faced ongoing challenges, including a near total absence of meaningful population growth and a weak labour force and the faltering of some local industries.

We did note in our forecasts that despite the weakened local economy and labour force there were plans already in place in 2013 to stimulate the property markets, including a substantial first home builders grant.

Unemployment remains high in the regions of Tasmania, although there have been some marginally more promising indicators and data sets flowing through our chart packs in respect of the capital city of Hobart (including e.g. more robust retail trade figures, healthier state final demand, and since Q3 2013, an improvement in wages growth).

RP Data provides no daily figures for us to chart for Hobart but over the year to date the Emerald Isle capital has recorded 0.7% growth, which is in the middle of our forecast range.

Verdict: Hit. Melbourne (Forecast 2 to 5%)

Melbourne (Forecast 2 to 5%)

Forecasting property markets in Melbourne and Sydney at times feels like one of the old "incomplete records" questions from an accountancy exam.

Our chart packs contain hundreds of data sets from which it should theoretically be possible to build a fairly robust macro housing market model, although naturally plenty of unforeseen events can occur through the course of year to reverse a trend which existed at the beginning of the period.

The established uptrend in owner-occupier finance for Melbourne as at Q4 2013 was broadly reflective of a similar gradient to that of Brisbane, that being indicative of a solid, recovering market.

Investor finance in Melbourne in Q4 2013 was demonstrably stronger still, but working against this Melbourne already had elevated vacancy rates, surfeit of stock on market (double that of Sydney) and a significant volume of dwelling supply in the pipeline at that time.

On balance, a full 12 months looked to be a very long time for growth to be sustained in Melbourne as dwelling completions ramped up, and our moderate 2-5% growth forecast for 2014 reflected that view.

What our chart packs do not adequately capture or pick up, of course, are shifts in sentiment from overseas buyers and the impacts of foreign capital. Indeed our housing finance data series do not record even the loans written for offshore Australian buyers by domestic banks, let alone the effect of those buying residential property with funds sourced from overseas.

In other words, like an accountant who is missing an entire section of documentation, we're working from incomplete records and thus there must exist a very real element of guesswork to be factored in.

At various points in the year, we were left scratching our heads as the Melbourne dwelling price data seemed to defy the law of gravity, but anecdotally the two largest property markets in Australia have been significantly impacted by the increased role of foreign investors and capital which is likely to account for some of the discrepancy.

The Melbourne chart now appears to be finally coming back down to earth with a noteworthy 2.6% drop in November, and with a few weeks left in the year the final result may yet just sneak into the 5% range.

RP Data's index has seen home values increase by approximately $37,000 from $635,000 to $672,000 or 5.8% with a few weeks left in the year to go.

Verdict: {TBC - it looks likely to be very close}.

Article continues on the next page. Please click below.

Perth (Forecast 0-3%)

Perth (Forecast 0-3%)

The trends in both Perth owner-occupier finance and investor loan finance in late 2013 were solid enough, but the city is pulling against a softening state economy as the mining construction boom unwinds.

Our chat packs also suggest that a looming glut of apartment supply will impact the market in the years ahead. Detached housing, particularly that located close to key transport links, appears likely to be the better performer in Perth.

Price growth in Perth in 2014 has been well within our 0-3% expected range.

Verdict: Hit. Sydney (Forecast 6-9%)

Sydney (Forecast 6-9%)

The Sydney market had an enormous momentum behind it at the end of 2013, with panic buying clearly evident to us in the market "on the ground", particularly at the back end of the year.

Here's what we wrote way back in November 2013 on Property Observer about our forecasts for the calendar year ahead:

"And finally, the problem child...Sydney. After years of weak supply in the harbour city, SQM Research put the cat among the pigeons when it forecast in its base case scenario that Sydney would record housing price growth of 15-20% in 2014, and 20-30% should Australia experience a strong economic recovery and interest rate rises by mid-2014.

"Being a Sydneysider, I'm a vested interest in the Sydney market, but there has never been reason to doubt SQM's integrity (they correctly forecast market price falls in 2011, for example) and their forecast is based on some sound price-to-income logic. Sydney's housing markets were relatively more expensive in 2003 and early 2004 than they are today and thus there is certainly a chance that prices could continue unabated at the growth levels seen in 2013 until the market hits its next irrational peak.

"There is a plenty of new apartment stock due to come online in certain sectors of the Sydney market (inner south, Central Park) but this is unlikely to be enough to halt the present cycle in its tracks in my opinion. However, 12 months is a long time and a lot might happen to slow the present exuberance."

In the event we opted for a conservative 6-9% growth and scored a clear downside miss here with our projection, the Sydney market holding its momentum throughout the entire year, which was clearly a risk we acknowledged given that we don't hedge by providing a wide range of scenario-based forecasts.

Significantly net population growth into the harbour city has accelerated in 2014 as net interstate migration from NSW to the mining and other states has declined to the lowest level on record.

Investor finance has continued to rise, and in the absence of regulatory intervention the Sydney market appears likely to carry some of its momentum into 2015, although the volume of auctions has increased to record levels which should keep an effective lid on rampant price growth.

The Wrap

We scored hits on five cities and a downside miss for Sydney which looks set to record ~12% growth according to RP Data's index. The Melbourne forecast will be close but the result will go right down to the wire over the next few weeks.

Stay tuned for our 2015 forecasts.

You can visit AllenWargent property buyers (London, Sydney) or Pete's blog.

His latest book is 'Four Green Houses and a Red Hotel' .