How will Australia be affected during these times of political and economic strain?

June, 2016 as I sat in our office in Singapore presenting a new residential off the plan project to our sales team, the announcement of Brexit was being announced.

‘British’ and ‘Exit’ is the withdrawal of the United Kingdom from the European Union. Also at the time, another major global event was occurring: ‘The 58th Presidential Election Campaign’. At the time Hillary Clinton was the ‘hot favourite’ to become and no one in the press gave Donald Trump a chance of becoming the 45th President of the United States.

How would Australia benefit from this?

I recall as the Brexit announcement came over the loudspeaker in our offices, it was like the world had suddenly stopped, everyone was in complete shock, disheartened to the extent it felt like the world was about to implode into a great depression. Why? The value for money proposition, the fear that the UK was going to go on a fire sale in the property market and the Chinese, South East Asian market were going to flood the UK market, to acquire extremely undervalued properties.

As our Chinese, Hong Kong & South East Asian offices were so reliant on investments into the UK; they felt UK investment values were going to drop dramatically. At the time, I did not appreciate the gravity and significance these global events were going to have on the Australian Economy or precisely the Australian Residential Project Market for new development sales.

These were significant times, that the world was about to change forever.

How does this impact the Australian economy in the future?

Why did I have these negative beliefs, towards such a buoyant economy?

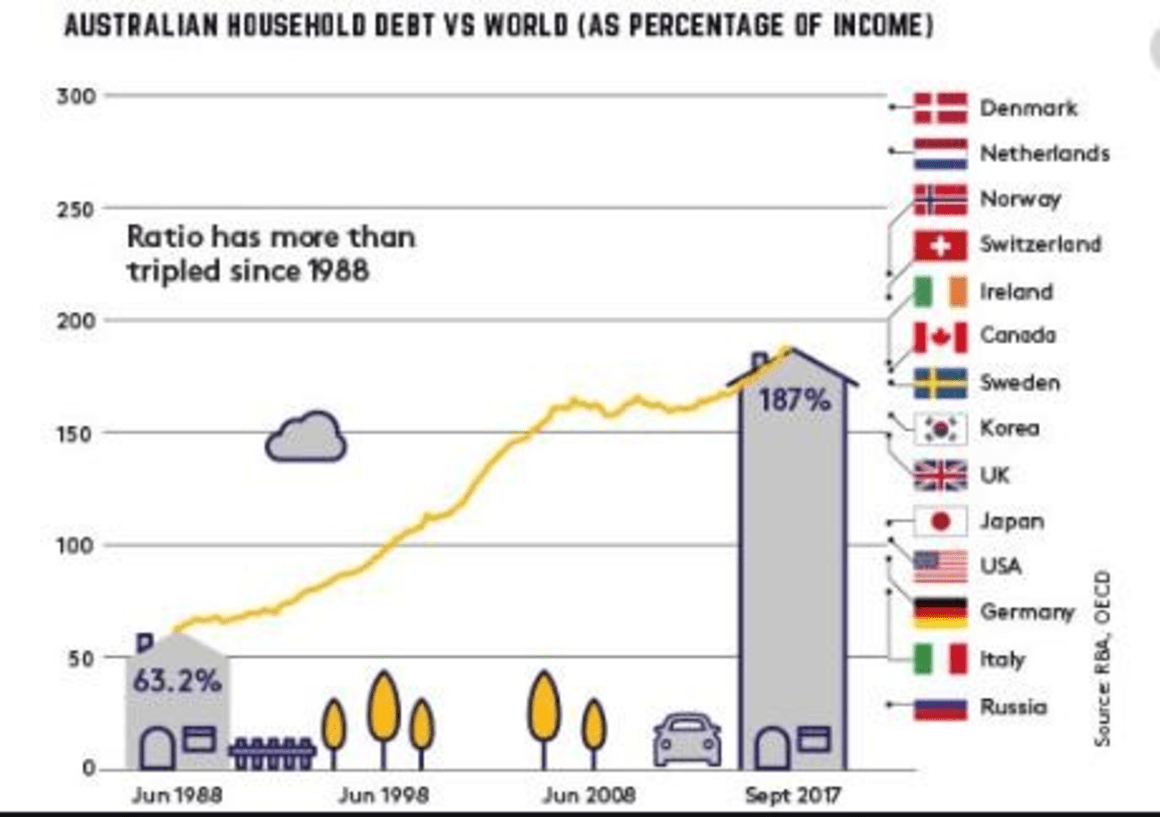

I felt we were heading for a property burst, as household debt was growing and property prices were increasing, beyond the serviceability of the average Australian Income. We were also restricting foreign investment, which had been the very reason why Australia was so strong economically, hence why we were hardly affected in 2008, post the global GFC.

Refer to graph below:

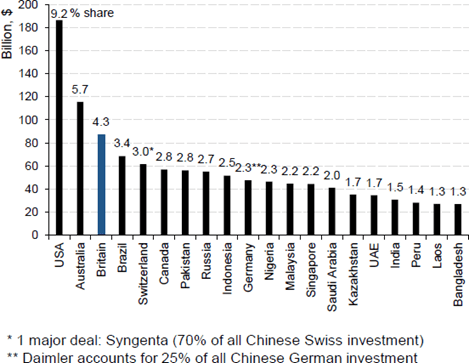

The forecast post this pandemic is that China will be the strongest economy in the world. Australia should relish the relationship, as they will be the only ones that will be able to afford our products and we can simply not ignore the Chinese market for our own economic gains.

See below the following graphs, these show where the money has moved from to where the money is moving too. Australia will be the one of the biggest beneficiaries of the movement of money from the West to the East of the world. China will be the monopolist as their currency will continue to get stronger as other currencies around the world will continue to decline.

Meanwhile, as the world was changing by the day in 2015 to 2019, Victoria, Australia we were going through our own changes for Residential off the plan projects.

- Town planning Laws, as the Victorian Government introduced minimum apartment sizes and set back laws.

- Influence of our Tax System: The main tax incentives include tax deductions for losses on investment properties, even those that have been negatively geared, and the 50% discount on capital gains on sale of investments properties. - Investors using their superannuation for property investments have a tax advantage compared to 'savers' who are effectively taxed up to 45% (the top marginal taxation rate) on income from bank interest or bonds, as superannuation contributions are normally only taxed at around 15%.

- Influence of the Financial Institutes, the criteria for lending to first home buyers, and investors had suddenly changed, making it more difficult for you to be able to get a home loan for an off the plan residence. Adding salt to the wound, the local banks were turning away foreign investors for residential loans on off the plan projects,

- The State Revenue Office introduced new stamp duty laws for local and foreign investors to pay more stamp duty, suddenly investors were paying more for property.

- Immigration to Australia, as our economy had 28 consecutive years of economic growth, there was a direct correlation between population growth, tourism, international students and migrants coming to Australia. As we will not see this influx of foreigners for a period of time, this has had a dramatic negative impact on our economy and ability to attract investors into Australia.

Australia federally and domestically, introduced changes to foreign visas, taxes and banking policies, that did not make it as appealing to invest into Australia in comparison to America, UK and Canada. On a per capita basis, we were extremely appealing to foreign buyers; our natural resources, medical, legal and education system and falling Australian dollar and rising Yuan, makes us very appealing for foreign investment.

See the graphs below:

- The property prices were growing at a rapid rate and this was beginning to be a cause of concern for our future. We had problems starting to appear back in 2015, yet we all believed these good times were going to continue for many years to come. However, we failed to see history repeating, as we were in a false economy based on the foreign influx of investment.

- In 2015, the International Monetary Fund sends an economic team to Australia to examine "the risks posed by property speculation and record-high household debt as part of a broad health check-up of the sagging domestic economy."[58]

- The head of the Federal Treasury Department, and the Federal government's most senior economic adviser, John Fraser publicly warned that Sydney and more expensive parts of Melbourne were experiencing a bubble. This was disputed by members of the government including the Prime Minister and Assistant Treasurer.[59]

- June - APRA 10% investment credit growth limit introduced.

- October - Macquarie Bank, a major Australian investment bank forecasted an end to property prices with "quarter-on-quarter house prices to fall from the March 2016 quarter before beginning to recover from June 2017, with a 7.5 per cent fall from peak to trough".[60] Westpac Bank independently raised the rates on its standard variable mortgage by 20 basis points against the Australian Reserve Bank. This was the first rate rise by an Australian bank in five years.[61][62]

2016

- May - From July 1, "Foreign buyers will have to provide citizenship and visa details, as well as Foreign Investment Review Board clearance, through the stamp duty process." "The ATO will match data to ensure foreign buyers have paid a $5000 fee for any property sold for less than $1 million, and $10,000 for properties over $1 million." [63]

- June - "In NSW, foreign buyers will be hit with a 4% stamp duty surcharge from June 21 and 0.75 per cent land tax surcharge starting in 2017. Victoria will raise its existing 3% stamp duty surcharge and 0.5% land tax surcharge to 7% and 1.5% respectively on July 1, while Queensland's 3% stamp duty surcharge kicks in on October 1." [64]

- August - The Official cash rate drops to 1.5%, the lowest cash rate on record.[65] The cash rate remains at 1.5% as of 1 July 2018.

Why did the government tinker so much, with an industry that was going so strong?

2017

- March - APRA limits interest only lending to 30% of new loans.

The four major banks, NAB, Westpac, ANZ and Commonwealth Bank increase home loan rates despite

Reserve bank rates citing the rising costs and regulatory responsibilities. These four banks control more than 80% of the $1.6 trillion mortgage market. Owner-occupier customers repaying principal and interest experience the smallest rise while investors with interest- only loans get the largest hike. The changes effective in April–May.[66]

- April - The governor of the Reserve Bank of Australia Phil Lowe states that increasing debt and rising house prices were risking the future health of the Australian economy. He noted that slow wage growth was making it harder for people to pay down their debt and attacked banks for lending to people with too little income buffer after interest.[67]

- July - Stamp duty abolished for first home buyers in Victoria, Queensland and Western Australia. Investor tax deductions for depreciation and travel abolished.

- September - The market reached its most recent peak in September 2017, according to Corelogic data.[68]

- December - Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry established.

2018

- March - hearings into the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry begin.

- July - Since the previous peak in September 2017, the combined capital 5 city property market has declined by -1.3% according to Corelogic.[68]

- July - It is estimated by Digital Finance Analytics that there are approximately 1 million households in mortgage stress. These households risk defaulting on their mortgages in the event of interest rate rises of as little as 0.15%.[69] APRA chairman Wayne Byres announced that the "heavy lifting on lending standards has largely been done", and that there was unlikely to be any further tightening of macroprudential policy.[70]

- July - Pressure is growing on the big four banks to follow smaller lenders (including ME, AMP, Suncorp, Bendigo Bank, Macquarie Bank, Bank of Queensland, ING, Pepper Group, IMB, Auswide and Teachers Mutual Bank) who have been raising interest rates on mortgage products from April 2018 onwards.[71] This is due to a rise in the inter-bank Bank Bill Swap Rate (BBSW). It is speculated that the causes for BBSW changes include the US Federal reserve's increases in US rates and poor returns on Australian deposits drawing funds away to international markets and Australian equities for better returns, as well as income repatriation of large American companies following tax changes of Donald Trump.[72] The funding gap between deposits and funds lent in Australia is estimated to have grown to A$457 billion in the first quarter of 2018.[73] This is putting pressure on bank wholesale lending and profit margins, raising the likelihood of interest rate rises independently of the Reserve Bank of Australia by the big four banks, despite the ongoing Royal Commission.

2019

- January 2019 - RBA releases a research discussion paper 'A Model of the Australian Housing Market', which concludes that the lower interest rates explain much of the rapid growth in housing prices and construction over the past few years. [74]

- February - Home prices across Sydney and Melbourne continue to fall as the RBA keeps rates on hold at 1.5 % for a record 29th month.

- May - The Liberal Party wins the election and Scott Morrison is elected as the Prime Minister of Australia, economic confidence returns and the property prices started to rise again.

- June - The RBA drops interest rates to a record low of 1.25 %, suggesting further cuts were to come later in the year [75], as the economy is not in as good a position as we thought.

- July - RBA drops rates to another low of 1% .[76]

- October - The RBA announced a further interest rate cut to 0.75%

2020

At the start of 2020, the world watched the Chinese city of Wuhan (11 million residents), and then the province of Hubei (60 million residents) going into full lock down. The hope was that the newly emergent coronavirus – later renamed formally as the Novel coronavirus (COVID-19) – would be contained.

Price Waterhouse; observe that countries (like Australia):

- with relatively higher service sectors and high consumption suffer relatively more under the coronavirus pandemic scenario

- that rely on imports for consumption goods, and exports that are inputs into producing those goods, can suffer through not being able to get the imports (or only at higher prices), and not being able to produce them domestically and facing a loss in demand/ lower prices for their exports.

Hence, we project that Australia’s household consumption will decline by A$37.9 billion over the forecast year.

The community impact - while our analysis focuses on the narrow economic cost of a potential coronavirus pandemic - and the broader social cost of such a loss of life should not be overlooked.

At times the human element is missed.

Stay isolated and stay safe.