Australia third most popular country for overseas students: Savills

Australia remains the third most popular country for international students, as the overseas student population continues to increase in both universities and other education sectors, says a recent Savills report.

Australia has a strong reliance on international students from a number of South East Asian countries, it says.

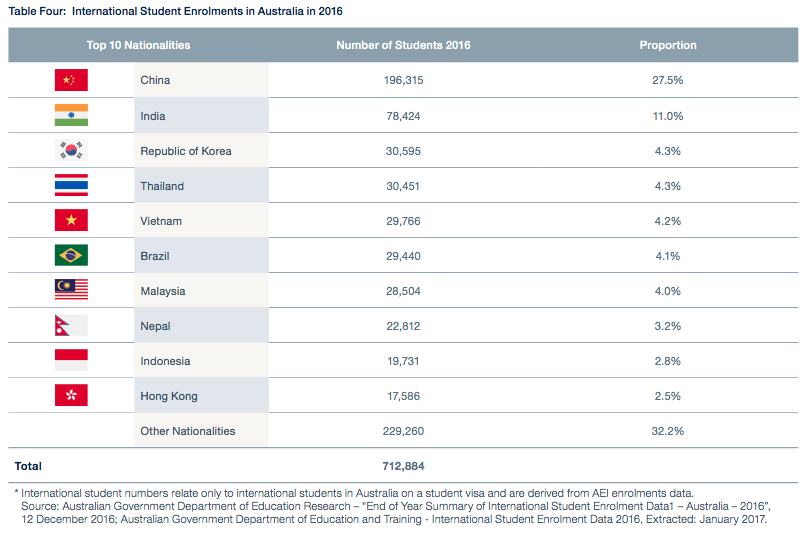

China (28%), India (11%), Republic of Korea (4%), Thailand (4%) and Vietnam (4%) are the top five countries of origin for international students studying in Australia, according to The Australian Student Accommodation Market Report by Savills.

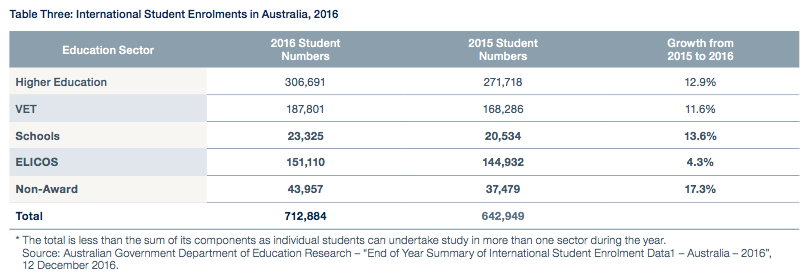

The latest demographic information available indicates that international student growth is stronger as evidenced by enrolments in higher education courses with student visas growing by 11% from 2015 to 2016.

In 2016, the strongest growth in international student numbers in Australia came from Brazil (20%), Malaysia (18%), Nepal (16%), Hong Kong (10%) and Colombia (22%).

{kind=link}

According to the report, universities across Australia also continue to be significant participants within the market, with 71,645 beds of Purpose Built Student Accommodation (PBSA) in the eight Australian capital cities. The existing supply in each city is less than 11% of the full-time student population with the exception of Canberra (28%).

Over the first three quarters of 2017, consistent with market activity throughout 2016, the key focus for the major developers in this sector has been the continued acquisition of sites and the construction and delivery of new Purpose Built Student Accommodation (PBSA).

“In Sydney, the University of Sydney, UNSW and Macquarie University are currently active in improving / extending existing residential portfolios,” said Conal Newland, director of Student Accommodation at Savills Australia.

“The University of Melbourne has been active with a number of projects in the last 12 months as have Deakin and Monash Universities. In Brisbane, the University of Queensland and QUT have also considered new projects.”

Newland added that there were only two institutional off-campus transactions in Australia in the first three quarters of 2017, though it was consistent with transaction volumes over the last five years.

In contrast, the more mature markets in the United States and the UK have been at near record volumes, he said.

Net initial yields in Australia have remained relatively static over the last 12 months, primarily due to the limited number of transactions.

Australia’s student population continues to grow at a steady rate, with total student enrolments increasing by 2.7% from 2014 to 2015, a rise of 36,903 students.

International student numbers increased by just less than 4.5% in 2015. All of this growth is attributed to full-time international students which increased by almost 5.5%. Part-time international student numbers fell by 0.8% in 2015.

Among the states, New South Wales, Victoria and Queensland showed the greatest number of student enrolments. Victoria achieving the largest increase in enrolment numbers year on year, with an increase of 4.4% compared to 2014. Of all the states, Tasmania saw the largest increase of 9.9% growth in 2015 with multi-state higher education providers increasing by 6.7%.

“The number of international students enrolled in Higher Education courses and utilising study visas in Australia has grown by 10.9% from 2015 to 2016, a marginally higher increase than the year previous” he said.

There were 554,179 international students studying on a student visa in Australia in 2016 which represents an 11.3% increase over 2015 figures (498,155 student visas). The top five nationalities are China, India, Republic of Korea, Thailand and Vietnam. China is the largest international student country of origin which contributed over 27% of the total number of international students in Australia in 2016. The country with the highest percentage of growth is Columbia with growth rate of 22.4% from 2015 to 2016.

Sydney is biggest drawcard for investment into the student accommodation sector. The significant supply and demand imbalance, world class universities and status as a global city are contributing factors, according to the Savills report. The total development pipeline in Sydney has increased from 3,665 beds in 2016 to 5,435 beds in 2017.

In Melbourne, the pipeline for delivery of new student accommodation has increased significantly in the last 12 months.

Savills 2016 research indicated a total pipeline of 9,651 beds, which has increased to 16,295 beds in 2017. This has been driven by the availability of development sites and the University of Melbourne's 2020 strategy to increase the pipeline of student accommodation bedrooms to 6,000.

After a period of two years when the PBSA development pipeline in Brisbane increased significantly, the activity has slowed in the first three quarters of 2017. There was a minor acceleration towards 30 June 2017, the date that Brisbane City Council’s infrastructure levy reductions ceased, and these projects must commence construction by the end of October 2017 to receive the concession. Analysis indicates that the total combined PBSA pipeline has increased from 8,930 beds in 2016 to 10,682 in 2017.

The development pipeline in Adelaide has grown to 2,159 in 2017 from 1,480 in 2016. In 2018, three projects are programmed for delivery including developments by Blue Sky, Kyren Group and Urbanest. In 2019 a further 380 beds are programmed for delivery.

There has been significant interest in the Perth student accommodation market in the last 12 months. The total development pipeline has increased to 3,621 beds from 2,000 in early 2016. This includes projects being promoted by Stirling Capital and Cedar Pacific. The development pipeline also incorporates the first stage of the Curtin University procurement – a mixed use project incorporating student accommodation.

It is clear when comparing both the existing supply and development pipeline across the major Australian capital cities, with the comparative cities in the UK that in general Australia has a much lower base of supply.

However, according to Rachel Coates, associate director of Student Accommodation at Savills Australia, one critical difference between the Australian and UK market is the propensity of domestic students in the UK to move away from home for university education – and therefore demanding PBSA.

“Australian domestic students are much more likely to live at their parent’s home while studying at university. Cultural drivers and specialisation of course offerings from UK universities has led to much higher rates of students leaving home and travelling to attend university studies,” she said.

It is interesting to note that the record level of UK transactions contributed to global student accommodation investment of over USD $14 billion in 2015. The US market also achieved record levels of USD $5.5 billion for the year and Western Europe USD $2 billion, again a record.

“The US and Western Europe continued to break records in 2016, with the UK having a slower year transaction wise, before being projected to reach close to 2015 levels in 2017. Sales activity in the first quarter of 2017 has been somewhat more subdued with a total of USD $1.95 billion of transactions,” Coates said.

“Analysis of recent transactional activity within the UK demonstrates how the Australian transaction market is still at an early stage, both in terms of the volume of stock that has been traded analysed in terms of the number of beds, and the total value of transactions. There is a substantial amount of trading in the UK forecast for the fourth quarter of 2017, indicating that transaction volumes could total close to £5 billion for the year.”

Coates went on to say that political reform of the Australian Higher Education Sector remains on the agenda, as continued government funding of the Australian university sector seems less likely, and competition between universities is set to increase.

“Savills expect that the provision of high quality purpose built accommodation will become an important consideration for a number of Australian universities. The levels of development activity among universities is already increasing,” she said.

“Sydney will continue to be the most attractive, but the most difficult market to access. Despite a rapid rise in the number of projects over the last 12 months, Melbourne continues to attract a number of new pipeline projects.”

Debt funding for new development led projects has affected a number of property asset classes through the first three quarters of 2017, including student accommodation. Accessing debt finance for new projects is anticipated to remain challenging.

Record numbers of investors are looking to access the Australian student accommodation market. However, whether development led or investment led, opportunities are at this stage limited.

“Looking to the start of 2018, the delivery of new pipeline accommodation, particularly in Melbourne and Brisbane is going to be closely watched by market participants and observers in terms of the occupancy uptake and stabilisation of new assets, particularly towards the top end of the rental price range. And accessing debt finance for new projects is anticipated to remain challenging.

“Savills anticipate at least one new developer entering the market either late 2017 or early 2018. We also see an opportunity for more competition in the independent third party management of student accommodation” said Newland.