RBA says risks to housing markets have increased

Risks to household balance sheets and housing markets have generally increased, the RBA's Financial Stability Review has noted.

In Sydney and Melbourne, housing prices are rising at a rapid pace and auction clearance rates are at high levels.

At the same time, there continue to be concerns about an oversupply of apartments in pockets of Melbourne and in parts of Brisbane, where apartment prices have declined in recent months, rental growth has been soft and the vacancy rate has trended higher.

In Western Australia and other regions with large exposures to the mining sector, overall housing market conditions remain weak.

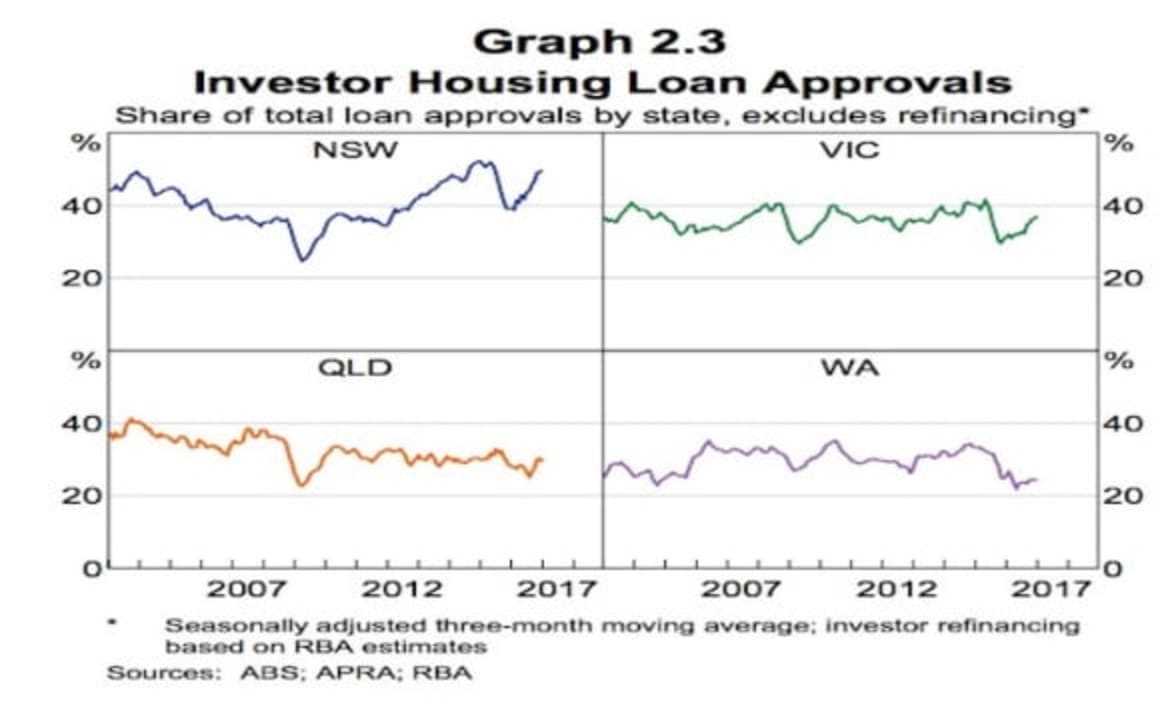

Investor credit has also risen noticeably over the past six months, with investor demand particularly strong in Sydney and Melbourne.

Overall household indebtedness has increased while income growth has remained weak.

Some types of higher-risk mortgage lending, such as IO loans, also remain prevalent and have increased of late.

APRA has recently taken measures to contain new IO lending.

The risks associated with strong investor credit growth and increased household indebtedness are primarily macroeconomic in nature rather than direct risks to the stability of financial institutions.

Some evidence suggests that investor housing debt has historically performed better than owner-occupier housing debt in Australia, though this has not been tested in a severe downturn.

Rather, the concern is that investors are likely to contribute to the amplification of the cycles in borrowing and housing prices, generating additional risks to the future health of the economy.

Periods of rapidly rising prices can create the expectation of further price rises, drawing more households into the market, increasing the willingness to pay more for a given property, and leading to an overall increase in household indebtedness.

While it is not possible to know what level of overall household indebtedness is sustainable, a highly indebted household sector is likely to be more sensitive to declines in income and wealth and may respond by reducing consumption sharply.

A further risk during periods of strong price growth is that it may be accompanied by an increase in construction that could result in a future overhang of supply for some types of properties or in some locations.

In this environment, as well as amplifying the upswing for such properties, any subsequent downswing is likely to be larger and more likely to see prices and rents fall if the vacancy rate rises.

This poses risks to the whole housing market and household sector, not just to the recent investors.

Prudent mortgage lending standards help to offset these risks. Over the past six months, lenders have further tightened lending terms, in part to keep investor credit growth within the 10% benchmark set by APRA at the end of 2014.

Recent non-price measures introduced by banks include tighter serviceability and maximum LVR restrictions on new residential projects or postcodes considered to be riskier.

Overall, the share of new lending with LVRs greater than 90% has fallen.

The price of mortgage finance has increased of late, and loan pricing is becoming more granular.

For example, the major banks’ advertised margin between investor and owner-occupier lending rates has risen to around 50–60 basis points after narrowing during 2016.

All of the major banks will have introduced higher IO pricing by April, resulting in an average IO premium of 18 basis points for owner-occupier loans and 15 basis points for investor loans.

Regulators continue to scrutinise lender compliance with broader regulatory expectations.

ASIC’s 2015 review of IO home loans uncovered a range of weak practices that led to a subsequent tightening of industry standards.

ASIC recently lodged a case with the Federal Court alleging contraventions of the National Consumer Credit Protection Act 2009 by one lender over a three-year period to early 2015.

In March 2017, ASIC completed a review of the mortgage broker market, which outlined conflicts of interest and other unsound practices such as lax assessment of consumer expenses and a propensity to direct consumers towards some higher-risk types of loans.

ASIC’s review recommended improvements to commission payment models, greater disclosure requirements for brokers, and improved governance and oversight of brokers by lenders and aggregators.

APRA and ASIC have also recently announced a range of measures that are designed to strengthen mortgage lending practices.