RBA weighs housing risks, Chinese prices lift: CommSec's Savanth Sebastian

GUEST OBSERVER

The Reserve Bank has given the Australian financial system a tick of approval although it is not without highlighting some of the medium term risks.

Generally policymakers believe that business and household balance sheets are in good shape and the financial system is sound. No doubt a lift in activity in the upcoming festive season would give the central bank more comfort.

When it comes to hot button issues, the central bank continues to monitor the housing market. In particular the stock of new apartments that are likely to add to supply across capital cities and the housing downturn in mining regions. In capital cities on the Eastern Seaboard, the amount of new apartments that will add to supply have the potential to depress prices. The downturn in mining towns has also resulted in a substantial pullback in property prices, resulting in “increasing financial stress among households, with non-performing loans rising, albeit from low levels”.

Commentary over the past couple of months suggests that while a low inflation profile is likely to be part of the medium-term landscape, the central bank is more reluctant to cut interest rates further. No doubt the question that is being debated is if rates are cut further, will it do anything to foster growth or just artificially inflate certain asset classes. Unfortunately there is not much more that the central bank can do to stimulate activity and that may be why the Reserve Bank has put the onus on the Government sector to also look at avenues to support growth.

The latest fall in lending finance is concerning – especially given the result follows the May and August rate cuts. Not only have total borrowings across the economy fallen for four out of the past five months, but they are down on year ago. The results are not just a one-month phenomenon. However it is important to keep in mind that late last year lending did hit a 7- year high. So it is not dire straits by any means, but the next few months will be more telling. It may also be the election uncertainty added to the weaker picture earlier this year.

In fact there are anecdotal signs of a lift in activity taking place over the past month. From a broader sense ultra-low interest rates have been part of the landscape for well over the past year and are providing support to consumer and business confidence. A lift in activity levels across the economy could be more telling in coming months – particularly in the lead up to Christmas.

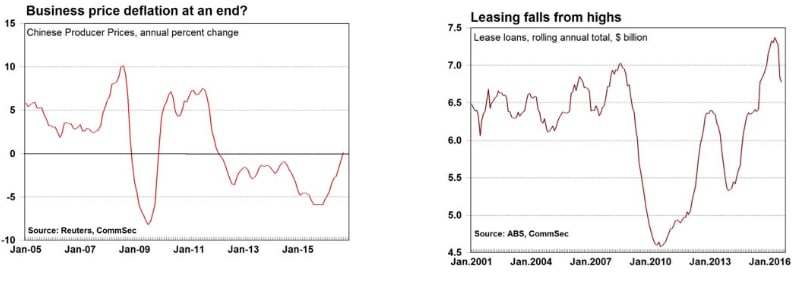

China isn’t seeing deflation of consumer prices, rather modest inflation. Where there has been deflation is in the business sector – producer prices. However even business inflation has now ended. In fact business inflation has posted its first annual increase in over 41⁄2-years. No doubt that has been influenced by higher mining and energy prices in the past couple of months, as is occurring elsewhere in the world. The ongoing deflation over the past couple of years reflected low capacity use in the factory sector. Encouragingly the shift to higher inflation (if sustained) is a positive from that perspective as well.

What do the figures show?

Lending Finance:

Total new lending commitments (housing, personal, commercial and lease finance) fell by 1.2 per cent in August, after rising by 4.8 per cent in July. Lending totalled $66.7 billion in August, down 3.4 per cent over the year.

All housing finance (owner occupier & commercial) fell by 1.6 per cent in August – the second consecutive fall.

Commercial finance fell by 0.4 per cent in August, after rising by 10.3 per cent in July. Within commercial commitments, fixed lending fell by 0.3 per cent while revolving credit fell by 0.8 per cent. Commercial loans are down 2.9 per cent on a year ago.

Personal finance fell by 4.3 per cent in August, after a 3.3 per cent rise in June. Fixed lending commitments rose by 0.8 per cent, while revolving credit commitments fell 12.3 per cent. Personal loans are down 0.1 per cent on a year ago.

Lease finance rose by 2.6 per cent in August after falling by 8.5 per cent in July. Lease loans are down 17.2 per cent over the year.

Chinese inflation:

Consumer prices rose by 0.7 per cent in September to be up 1.9 per cent on the year, against expectations of a 1.6 per cent lift. Consumer prices had lifted 1.3 per cent in the year to August.

Non-food prices rose 0.4 per cent in September to be up 1.6 per cent over the year.

Food prices rose by 1.7 per cent in September to be up 3.2 per cent over the year, up from the 1.3 per cent annual gain in August.

Producer prices rose by 0.1 per cent in the year to September, firmer than the 0.8 per cent decline to August and ahead of the market forecasts centred on a 0.3 per cent decline. It was the first annual rise in business inflation since January 2012 (41⁄2 years).

Reserve Bank Financial Stability Review

On the economy, the RBA noted: “Overall, the Australian banking system remains in good shape after a number of years of strong profit growth and efforts to strengthen bank resilience.”

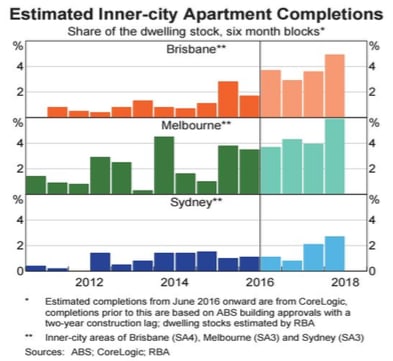

On residential property: “Risks around the projected large increases in supply in some inner-city apartment markets are coming to the fore, especially in Brisbane and Melbourne. There are signs that some settlements are taking longer and lending valuations are coming in below their contract price, though settlement failures to date remain low.”

“In residential property development, the risks in some apartment markets are closer to materialising, as the foreshadowed large and geographically concentrated increase in supply approaches. These risks appear greatest in inner-city Brisbane and Melbourne, where the new supply is largest relative to the existing dwelling stock. Developers face the risk that off-the-plan sales of apartments in these areas fail to settle due to tighter lending standards for buyers (particularly non-residents or those relying on foreign income) and valuations at settlement below the contract price. To date, settlement failure rates have remained low, although in some cases settlement has been delayed because the buyer has had difficulty accessing finance”

Commercial property: “In office property markets, while yields in Australia and abroad have fallen in line with the global ‘search for yield’, weak conditions in Brisbane and Perth stand in contrast to the stronger performance in Sydney and Melbourne.”

Banking sector: “Banks have recently tightened their serviceability requirements further by restricting lending to borrowers relying on foreign income; this might weigh on demand in some inner-city apartment markets. They have also taken steps to mitigate the associated risks by tightening lending conditions for new property developments. This could also help forestall future oversupply in some inner-city areas.”

“Australian banks’ domestic asset performance deteriorated slightly over the first half of 2016, after several years of steady improvement” .” To date, the pick-up in the non-performing housing loans ratio has been almost entirely in ‘past-due’ rather than ‘impaired’ loans, suggesting that, at current prices, banks generally expect to recover the full amount of their loans”.

Housing sector: “Risks to the household sector overall have lessened a little further since the previous Review.”

Business sector: “Businesses generally remain in good financial health, with aggregate levels of gearing arouir historical averages and the earnings of listed corporations broadly in line with prior periods.”

Mining regions: “ in areas reliant on mining there are clear signs of increasing financial stress among households, with non-performing loans rising, albeit from low levels.”

LVR’s & debt servicing: “ the tightening of lending standards in recent years has meant that the profile of this new lending is lower risk than it was a year or so ago. For both owner-occupier and investment lending, the share of loans at high loan-to-valuation ratios (LVRs; those greater than 90 per cent) is now around its lowest level since the series began in 2008.”

“Households’ debt-servicing ability remains well supported by the very low level of mortgage interest rates. Households are also less leveraged than in 2012, when debt-to-asset ratios peaked”.

Banks & developers: “ (bank) lending to developers is generally well secured and, as yet, the additional costs to developers associated with settlement difficulties have not resulted in losses to the banks.”.”

Property prices: “ any (residential) oversupply in Australia would be more localised to certain geographic areas, and potential price falls tempered as the population moved to absorb the new (and cheaper) supply of housing in these areas over time.”

What is the importance of the economic data?

Lending Finance is released monthly by the Bureau of Statistics and contains figures on new housing, personal, commercial and lease finance commitments. The importance of the data lies in what it reveals about the appropriateness of interest rate settings, confidence and spending levels in the economy.

China’s National Bureau of Statistics releases its monthly economic statistics around mid-month. Quarterly GDP data is released around the 19th of January, April, July and October. China’s Customs Office releases trade data, and the People’s Bank of China releases financial statistics, around the 10th of each month. China is Australia’s largest trading partner and changes in the Chinese economic have major implications for the Aussie economy.

The Financial Stability Review is published by the Reserve Bank every six months. The report is basically a health check on the financial sector but it also assesses the state of household and business balance sheets.

What are the implications for interest rates and investors?

The Reserve Bank has identified a couple of housing-related risks that it is watching closely. Banks remain well positioned to deal with any risks that may manifest into problems.

The bottom line is that Chinese inflation is not an issue but deflation is less of an influence as well. Chinese authorities still retain plenty of scope to ease monetary policy if that was considered useful to support economic growth.

Next Wednesday the key activity indicators are released in China – Economic growth, retail sales, production and investment.

Savanth Sebastian is an economist for CommSec