Occupier and investor demand in London: Savills

GUEST OBSERVER

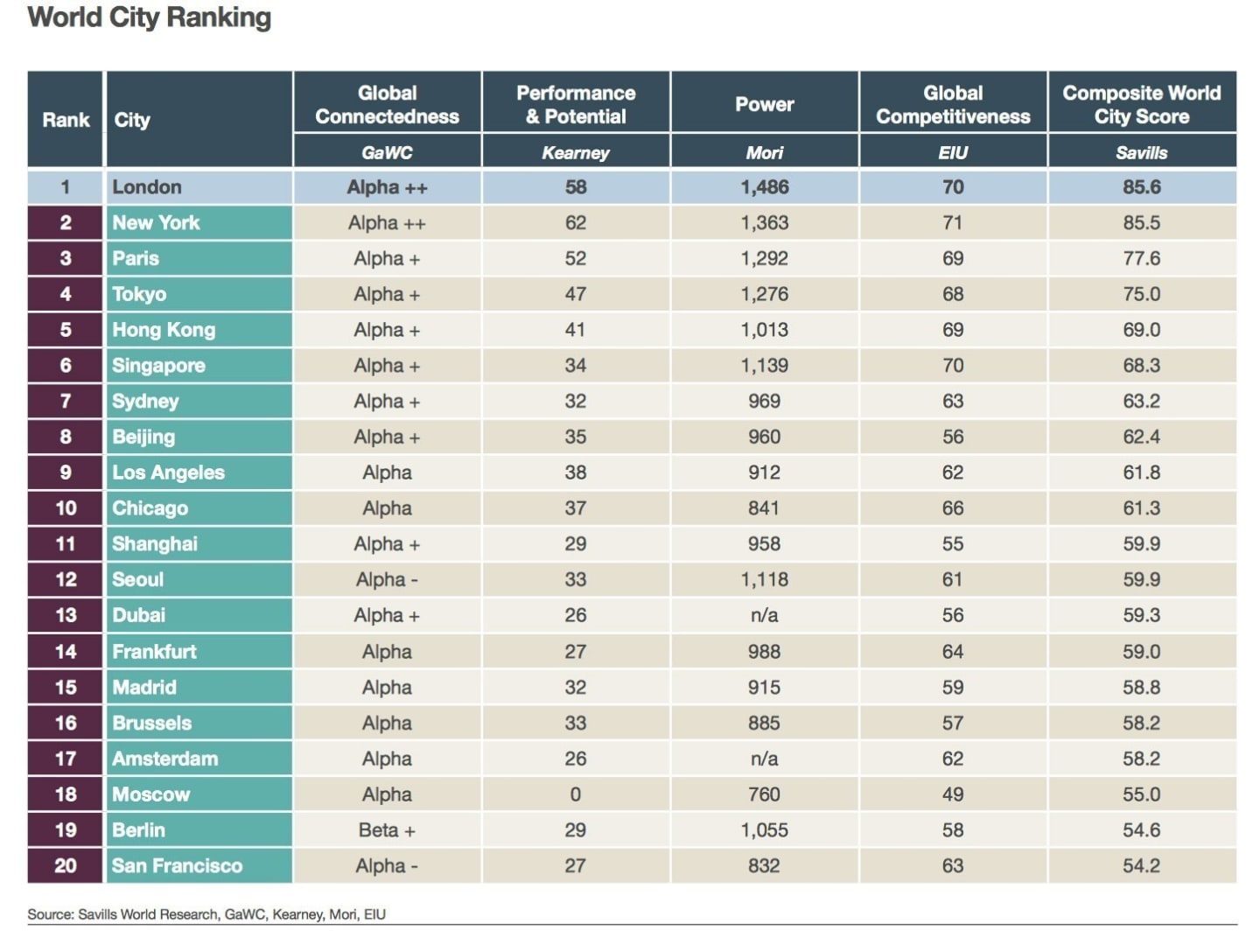

London is one of the most diverse, globally connected, competitive, high performing cities in the world, on a wide variety of measures.

We have combined four of the most widely quoted indicators of World City prominence. These measure global connectedness (gaWC), performance and potential (kearney), power (Mori) and global competitiveness (eIu). Together, these create the Savills World City Ranking.

London and New York stand out far ahead of other cities and illustrate how a unique combination of strengths marks them out as global powerhouses. We have dubbed London a ‘polymath city’ for being so pre-eminent in a wide range of aspects of city life.

It might be worth noting, however, that although ranking high economically, London, and indeed the rest of the world cities tend not to rate so high on the ‘softer’ social and environmental issues.

It is also notable that none of the 20 cities rate in the top ten of the Economist’s ‘Liveability Ranking’, for example. Numbeo’s Quality of Life Index 2015 places London in 90th place out of 150 cities, ahead of Paris, Hong Kong, Shanghai, Moscow and Beijing but behind the other 14 cities (only Frankfurt makes it into Numbeo’s top 20).

It would seem that being a top performing world city comes at a price. Pollution can be higher (though London’s is slightly below average), and real estate costs in the 20 cities are significantly higher than in other global cities but, surprisingly, London’s are not among the highest when mainstream housing costs are measured against average household incomes.

This dubious honour belongs to Hong Kong, Beijing, Shanghai, Moscow and Singapore. Traffic congestion and long commutes are another side effect of economic success but London does not fare too badly here, in comparison to other world cities. If Numbeo is to be believed, London’s main downfall in the quality of life rankings (in common with most of the other 20 cities) is that the purchasing power of individuals is low, in relation to average incomes and consumer prices are high.

A rapidly expanding employment base is underpinning a new wave of expansion in London’s office markets. New records were set in the leasing markets in 2014, with 8.2m sq ft leased in the City of London. Reaffirming London’s status as one of the most important global centres for the creative, media, entertainment and tech industries, the capital has seen a general shift in occupier demand from west to east.

This in turn has been reflected in fast-rising office rents. The proportion of office take-up by creative and technology companies in the City of London was 17% in the year to June 2015, the same as the proportion taken by insurance and financial service companies.

However, it is worth noting that the banking sector has started to recover this year, and this means banking and finance companies currently account for 38% of current requirements across central London. A buoyant occupier market underpins record investment – London is the number one destination for cross-border investment into offices globally.

Rapid employment growth puts further pressure on London’s housing market. New housing supply has failed to meet the need and the pressure on living costs has continued to build. House prices in London have risen by 43%, and private sector rents by 19% over the last five years according to the ONS. Investment in transport improvements is essential to open up new parts of the city for housing development. Crossrail, an upgrade to Thameslink services and an extension to the Northern Line, is unlocking new development in the near term.

The focus of London government at present is ensuring that sufficient and affordable accommodation is provided to house London’s growing population. There is concern that a combination of high land prices, low industry capacity and a historic undersupply backlog will continue to thwart these intentions.

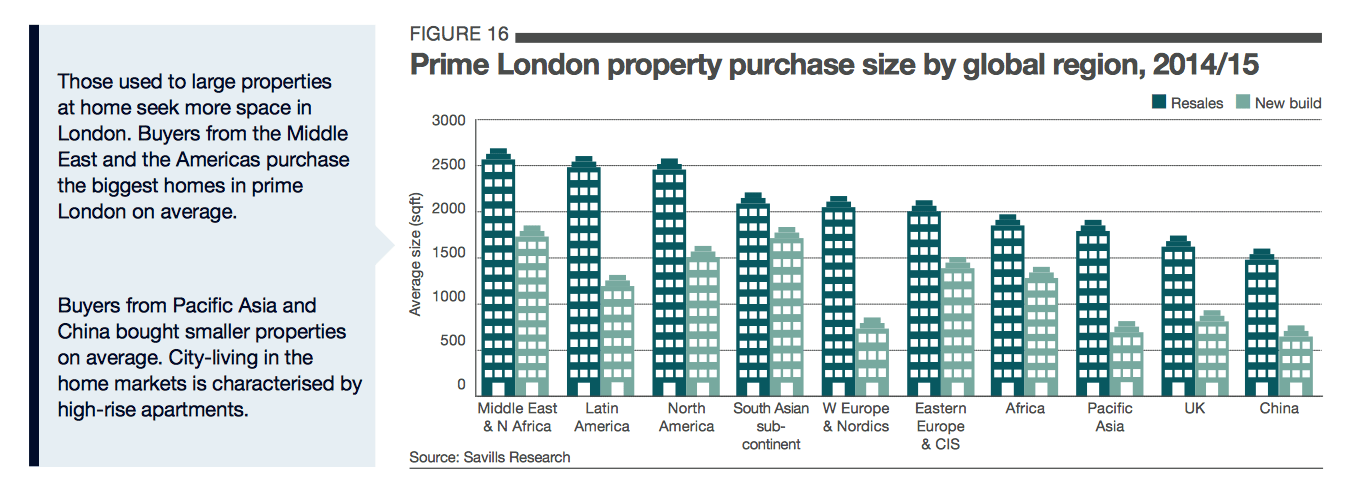

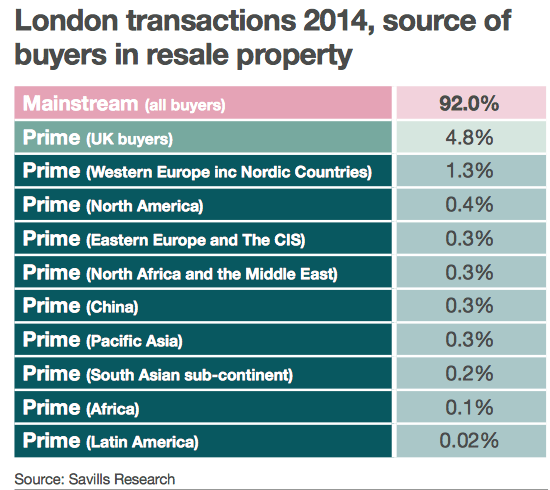

Global urbanisation and the focus by people on city living has meant that international investment activity has also been focused in this way. Worldwide, prime city property has appreciated in value but mainstream property has not grown by so much. This is as true of London as any other global city.

The impact of overseas investment by private individuals in world cities seems to have pushed up prices for wealthy people in the prime markets, but not so much for mainstream property in secondary markets.

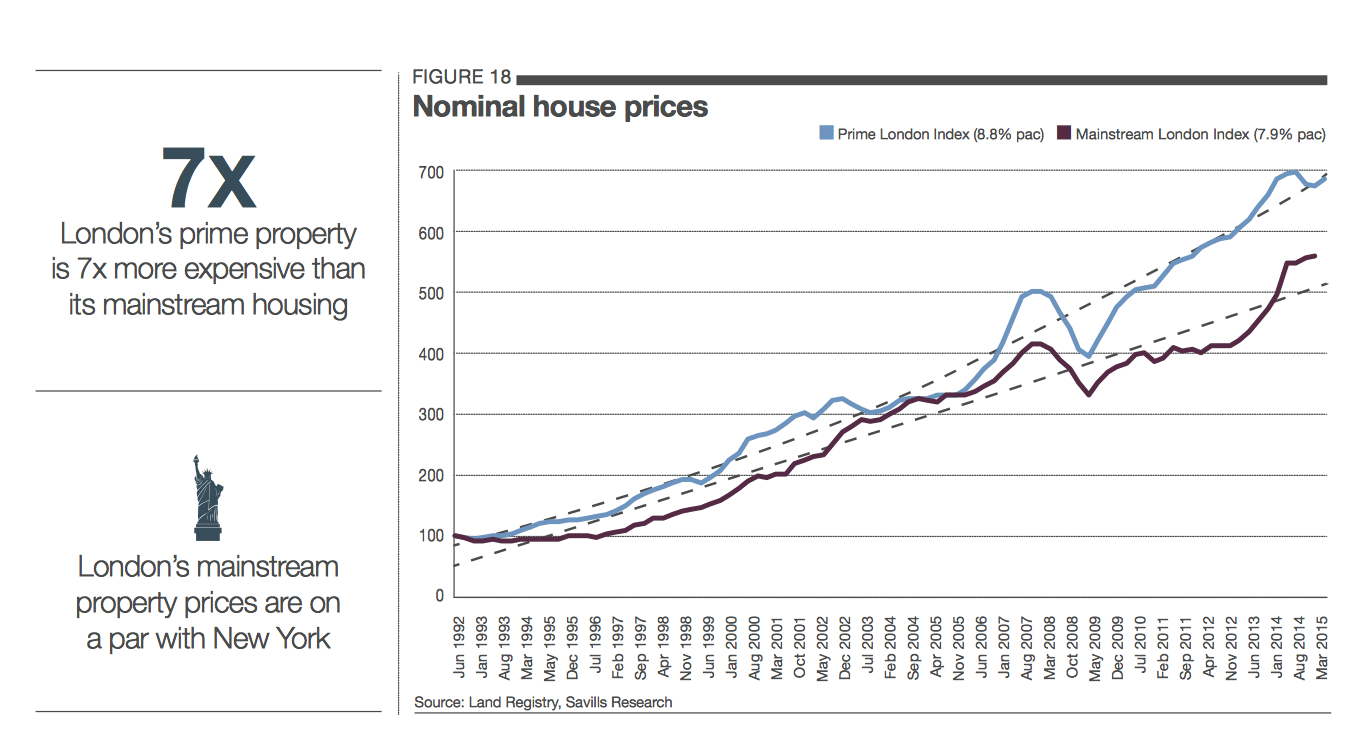

London’s prime residential real estate is seven times more expensive than its mainstream housing, compared to New York’s, for example, which is only four times the price. The higher incidence of overseas property buyers in London has created an international market in prime property but London’s mainstream property is about the same price as New York’s.

At a global level, mainstream London property prices are on a par with Singapore and New York and cheaper than Hong Kong’s (all of these cities have growing populations and constrained land supply). This still makes London one of the most expensive locations in which to buy property globally, but the issue seems to be one of high demand against near-static supply, rather than the weight of money pressing on prime markets.

It is when new development is overly concentrated in prime markets that these supply problems are exacerbated. London has been able to grow the size of its prime stock but has been less successful at growing its mainstream housing supply. London has several possible solutions to its issues of high home prices:

- Densify and make better use of land, especially in central and transport- accessible neighbourhoods

- Open up new areas with new transport infrastructure

- Regenerate low-grade and low-density land, both publicly and privately owned

- Intensify neighbourhoods by mixing residential into low-intensity retail and workspace uses

- Expand beyond political boundaries, a significant proportion of London’s workforce lives outside greater London already.

Until most or all of these solutions start to change the supply of housing in London, the city is likely to remain among the world’s most expensive.

London, unlike many former hosts of the Olympic Games, saw both visitor numbers and spend increase in its post olympic year, a trend that has continued. London is expected to welcome 18.8m international overnight visitors in 2015, and has topped the Mastercard’s global destination Index in four out of five years, except 2013, when bangkok held the lead position. London also topped the rankings for tourist spend at $20.2bn, with a significant chunk of this spent shopping.

London’s world famous shopping streets and its variety of international brands, including home grown ones such as Burberry, have helped to increase international tourist spend. But it has been London’s ability to attract high spending tourists that has really established it as a Global retail destination.

The biggest spenders have been those coming from the UAE and China. They each have an average spend per transaction of over £900 (US$1,400). The fact that China is now the largest consumer market of luxury products globally, with an increasing proportion of this spend taking place overseas, means that they are an attractive target consumer group – particularly for luxury brands.

At present Chinese tourists account for only a small proportion of total overseas spend in the UK. According to official data from the ONS 233,000 mainland Chinese tourists came to the UK last year with a total spend of £559m. This represents only 2.6% of total overseas spend.

In contrast France attracted over 1 million Chinese visitors. The difficulties experienced by Chinese visitors in obtaining visas has been cited as an issue contributing

to these lower visitor numbers. Improvements to the visa application process, introduced last year, are expected to improve these numbers.

VisitBritain is hoping it will help to attract 650,000 Chinese visitors by 2020, with spending power of almost £1.1bn (US$1.7bn).

London’s position as one of the largest city markets for international tourists, and the potential upswing in Chinese visitor numbers, has attracted increasing numbers of international brands.

Since 2012, 98 international brands have opened their first UK store in London with another 11 expected by the end of the year.

New entrants

The majority of these new entrants have come from Europe (64%), with another 25% originating from North America are now also, largely reflecting the existing international mix of retailers on London’s key shopping streets.

However, retailers from Asia Pacific and South America have established a presence in London, reflecting the increasing globalisation of London’s retail landscape and

its visitor profile. This influx of new retailer entrants, combined with availability constraints on the traditional key pitches, have helped to open up new retail ‘destinations’ within London.

Historically, any new retail brands to London would have tended to concentrate within a relatively narrow selection of pitches. The scale of new entrants and existing demand, combined with improvements and enhanced ‘curation’ by a number of existing and emerging landed Estates within Central London has widened the variety of retail ‘destinations’ available to both occupiers and shoppers.

The top locations of choice for new overseas retailers to London since 2012 are Westfield (West London and Stratford), Covent Garden and Bond Street.

This influx of international spend has not been solely confined to consumers and occupiers. Investment by international investors into Central London retail property has also intensified.

Total acquisition activity by overseas investors totalled £1.5bn in 2014. This represented 59.2% of total activity levels. This investor behaviour is changing the ownership landscape of some of London’s key shopping streets. And it is not just international investors that have become increasingly acquisitive. International retail brands themselves have also been on their own shopping spree.

Overseas ownership

Close to half (45.2%) of all retail units on Bond Street are now owned by overseas entities, up by 10% in January 2013. But around a third of these international owners are in fact international retailers, not investors. While retailer owner-occupation is nothing new on Bond Street, the change has been the increase in acquisition by retailers irrespective of whether they are occupiers or not.

Retailer ownership has increased by 28% since early 2013, but, only half of these retailer owned units are owner-occupied.

Purchaser motivations seem to be in part competitive and in part a way to future proof themselves against further rental growth following the strong rental uplift seen over the last three years (prime Zone A rents on New Bond Street have increased by an average of 20.8% per annum). This trend appears relatively unique to London and is facilitated by the city’s transparent and open real estate market.

On the flip side, this investment appetite from brands has also contributed heavily to competitive tension in yields and retailers becoming landlords to their competitors. In the case of Oxford Street, where the need for protectionism is less acute, overseas retailer ownership is lower, accounting for 10.0% of all units on the street.

Meanwhile, investment activity by other international investors has picked up significantly. With availability on Bond Street some overseas investors have looked to other retails streets to satisfy demand. For example, overseas ownership on Oxford Street has increased by 24.4% since early 2013.

Going forward, activity from overseas investors is expected to continue but is likely to focus on those key retail destinations where current ownership profile offers opportunity.

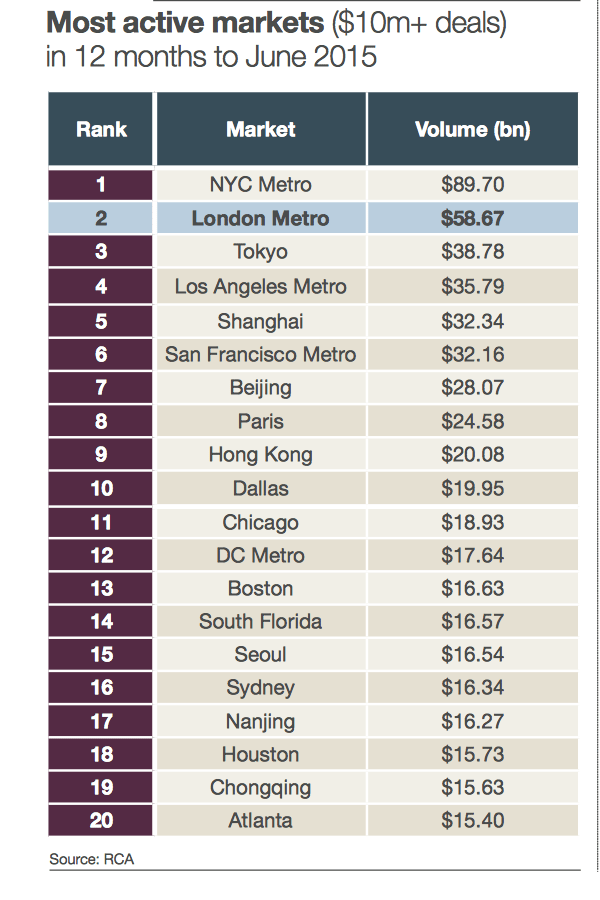

The weight of money pressing on real estate in world cities is a widely reported phenomenon. London was the second most invested world city after New York by large-scale investors in the year to june 2015 according to Real Capital analytics.

But it is not just institutions and corporations who are focused on real estate as an investment class. The type and range of players in the market has increased substantially since 2008 with Sovereign Wealth and private individuals entering the fray to a much greater extent.

A recent survey of global wealth advisers by Savills/Wealth Briefing showed that private wealth is very active in real estate with 45% investing more than a fifth of wealth in direct property holdings and 37% investing an additional sum amounting to more than 10% of their wealth in indirect property holdings (property companies and REITs for example). Only 9% of these survey respondents said their clients were planning to decrease their exposure to direct property and 13% to decrease their indirect holdings.

Much of the recent buying activity in real estate has been directed at prime property in world cities, and buying behaviour has been focused on London and top US cities. Our survey of private wealth property holdings in 2014 shows few signs

of activity abating. According to the Savills/Wealth Briefing survey, 67% of high net worth private clients want to buy more real estate in North America and 63% in the United Kingdom. This compares with only 37% who are looking to buy in China and Hong Kong, for example.

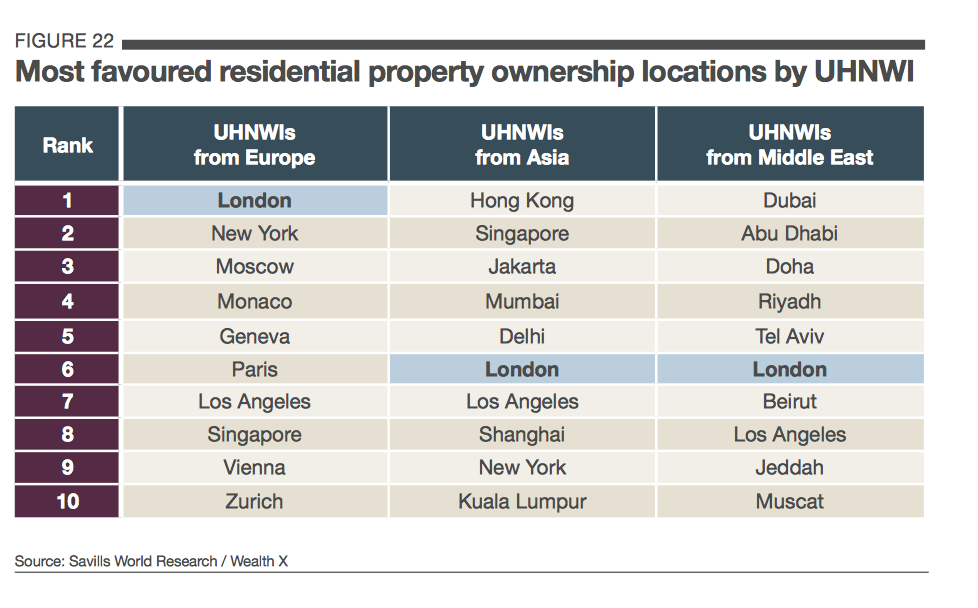

One characteristic of private wealth is that it is focused on different sectors of property to institutional money. Residential property, development land and agricultural land are the three top buys on private clients’ shopping lists (72% of all respondents say their clients are looking at this sector). But offices also feature prominently, with 50% looking to buy in this sector.

The implications of this for London are that money will likely continue to press on the city’s real estate markets. For those seeking the best income returns from day one, the extent to which this weight of money suppresses yields and increases prices means for them, too much money is pointing at the city.

Consequently, we anticipate that the smart, income-seeking money will increasingly move away from the prime centre to the higher-yielding periphery and even outside of London. Some of it already is, with high-quality city markets like Oxford, Cambridge and Edinburgh already seeing significant investment activity.

Those seeking capital growth will do well to look at the underlying fundamentals of rental growth and the prospects of its continuance, as there is very little scope for further investment yield reductions to boost prices.

Meanwhile, trophy properties, such as mansions, farms and sporting estates, are also beginning to see increased activity and we expect this to grow. Access to London, even from these more far flung retreats, will still be important, so the western corridor with access to Heathrow and the world beyond will likely continue to be a favoured location.

Yolande Barnes is director, world research with Savills. You can follow Yolande on Twitter here.