Large Melbourne supply hits post COVID-19

JLL's recent ‘Will Melbourne’s city Fringe keep kicking goals’ report explores vacancy and rental scenarios for the market, post pandemic.

In recent years, Melbourne’s Fringe office market has recorded strong rental growth in prime and secondary assets, in some cases outperforming CBD markets nationally.

In 2020 the new supply to the Fringe markets is expected to be more than 9 times the 20-year-average. By the end of 2024, Melbourne’s Fringe office market is forecast to have a net increase in stock of close to 305,300sqm, taking the total market to 1.87million sqm, JLL research forecasts.

While 1Q20 represents the peak of the net face rental growth cycle in the Fringe, the impact the health and economic crisis could have on the Fringe vacancy is still to be determined, particularly due to the variable and flexible component of the Fringe office supply pipeline. However, as vacancy increases with the onset of new supply and downward pressure on demand, JLL predicts we will see effective rents in older and secondary stock recording more pronounced corrections.

JLL Research is tracking 55 projects >1,000sqm that could deliver an additional 272,700 sqm of office space to the market by 2024.However many of these are unlikely to proceed without pre-commit and therefore may be deferred or put on hold.

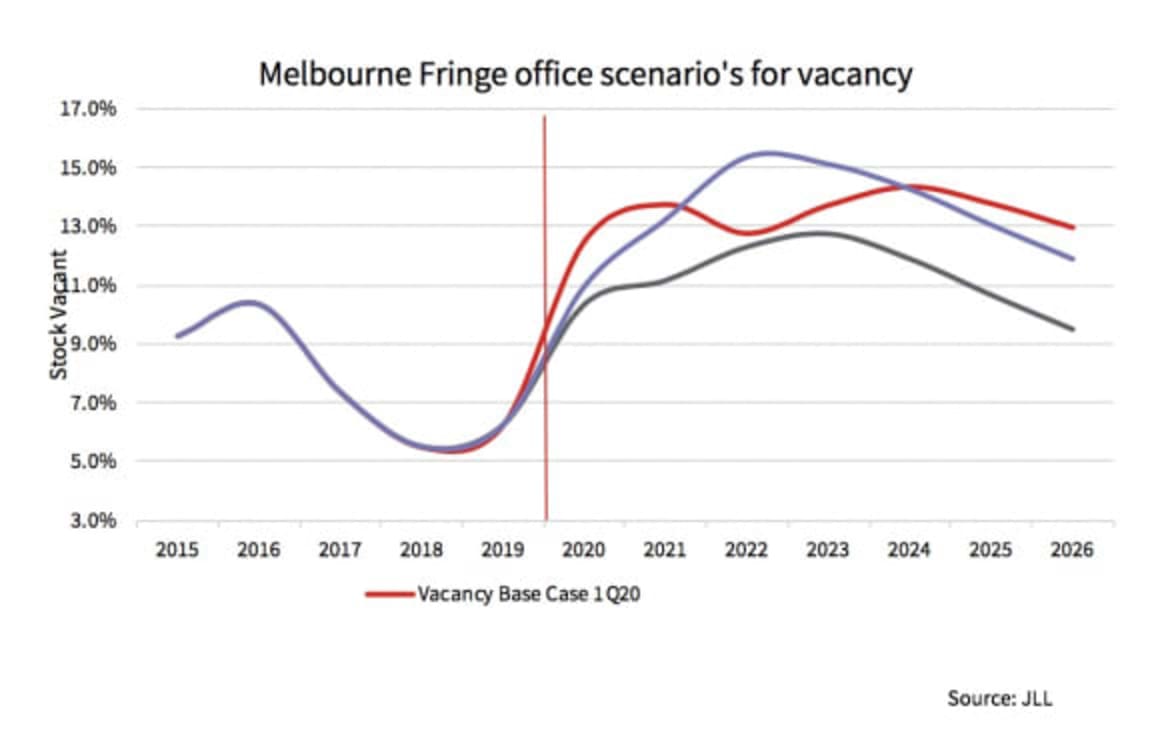

The projected supply, withdrawals and likely demand will all impact the Fringe office vacancy which is predicted to rise to 13.7 per cent by the end of 2021 and reach a second peak in 2024 at 14.3 per cent.

Several factors will impact the variance in predicted vacancy scenarios;

- Revised Scenario V shaped recovery assumes the supply pipeline is more substantially reduced or delayed and demand bounces back strongly in 2022. Vacancy peaks in 2023 are in the region of 12.8 per cent .

- Revised Scenario longer term impact assumes a reduced or delayed supply pipeline but also continuing inactivity for the next four years, minimal withdrawal of assets for any type of development and weaker demand. Vacancy peaks in 2022 are at approximately 15.4 per cent.

JLL’s senior research director, Victoria, Annabel McFarlane, said: “COVID-19 is expected to have a short to medium term impact on the Melbourne Fringe markets. After five years of very strong rental growth with prime net effective rents increasing by 9.2 per cent on average annually, we are projecting that net effective rents will contract by 9.1% from the peak in 1Q20 to trough in 4Q21.

“As demand softens, developers may postpone or place projects without any level of pre-commitment on hold as softening rents and yields impact the long-term viability of these projects. Shorter build periods and smaller project sizes gives the Fringe market a degree nimbleness as potential speculative supply is postponed in response to reduced demand.

“However, it is not all negative and we predict some sectors to expand post pandemic, which will particularly affect the Fringe market given the occupier range. The fringe market will have an important role to play in the post COVID environment as some businesses look to split workforces and increase flexibility for staff.”

JLL’s head of metro office leasing, Victoria, Josh Tebb added, “Sectors including Technology, Health Care and the Public Services sector which are predicted to expand already have strong footholds within the Fringe markets, and these precincts are well placed to absorb these rapidly growing sectors in the recovery.

“We are only beginning to witness the impact of COVID-19 on the Victorian office market but in these early stages, we believe the cost savings and controlled building environments of smaller buildings in the immediate fringe may appeal to some CBD tenants seeking to separate departments and project teams for the short to medium term.”

Ms McFarlane concluded, “Longer term, Melbourne is well positioned from a macroeconomic stance, with liveability, relative affordability, historic population and jobs growth and a strong education sector to support the recovery from this health and economic crisis. Office markets will need to become more metropolitan to accommodate the changing and growing workforce.”