The property suburb winners and losers of 2012: Cameron Kusher

It has been another comparatively weak year for the residential housing market, with data to November indicating that capital city home values have fallen by 0.1% over the year.

What to expect in 2013

As we enter 2013, Australia’s housing markets are likely to remain relatively flat. However, in some sectors we may see capital gain increases over the coming year.

As per the current status quo, there is likely to be a continued variance in performances from city-to- city and region-to-region. Property markets in Sydney, Brisbane, Perth and Darwin, where home values have corrected more than the other capital cities, may be the markets to watch for improving conditions.

We are already seeing signs of a recovery in these markets, particularly in Perth and Darwin. On the other hand, markets such as in Melbourne, where capital gains have had a strong run, are more likely to see weaker conditions.

The number of properties being advertised for sale across Melbourne has ramped up very quickly; new listings have remained fairly constant. However, the total number of homes available for sale simply hasn’t been absorbed due to a slowing rate of sale.

Due to the high capital gains and a comparatively weak rental market, Melbourne rental yields are also comparatively low. There seems to be a likelihood of further interest rate cuts in the near future by the RBA, especially in light of the revelations of a slowing Chinese economy and a substantial decline in commodity prices and the likelihood of much slower economic growth over the third quarter of 2012.

The rising rental costs and lower interest rates may, in certain areas, result in some renters now looking to enter into home ownership. On the other hand, consumer caution persists and consumers broadly continue to prefer paying down debt and shun new debt, which is likely to restrict any significant improvement borne through lower interest rates.

The big wild card remains the global economy. The likelihood of further economic uncertainty is high, which will continue to dampen consumer confidence and the willingness to spend on high commitment decisions like purchasing a property.

As a result, any significant growth in values across the national housing market would appear to be some way off. The recent improvement in sales transactions will be vital to a sustainable return to value growth across the country. However, it will need to be maintained for a number of months before there is evidence to proclaim a recovery.

Click to enlarge

Source: RP Data

The state of play in 2012

This year delivered weaker market conditions for the residential housing market, with data to November indicating that capital city home values fell by -0.1% over the year.

- House values fell by -0.4%

- Unit values increased by 1.6%

- Over the first 11 months of 2011 capital city home values fell by -3.8%

- House values were down -4.0%

- Unit values declined by -2.6%

How did 2011 compare with 2012?

There are a number of reasons for the property market’s lacklustre performance in 2012. These include: growth in housing credit has been extremely limited; low levels of consumer confidence; affordability barriers due to a higher mortgage rate environment.

Although research confirmed that the property market was weak over the past 12 months, there are select areas around the country that have well and truly outperformed others.

The following lists the top performing suburbs around Australia over the 12 months to September 2011. Specifically, the analysis will look at:

- Highest median sale prices

- Most affordable median sale prices

- Most affordable median sale prices within 10km of the capital city

- Highest indicative gross rental yields

- Highest indicative gross rental yields within 10km of the capital city

- Greatest increase in median selling price over the past 12 months

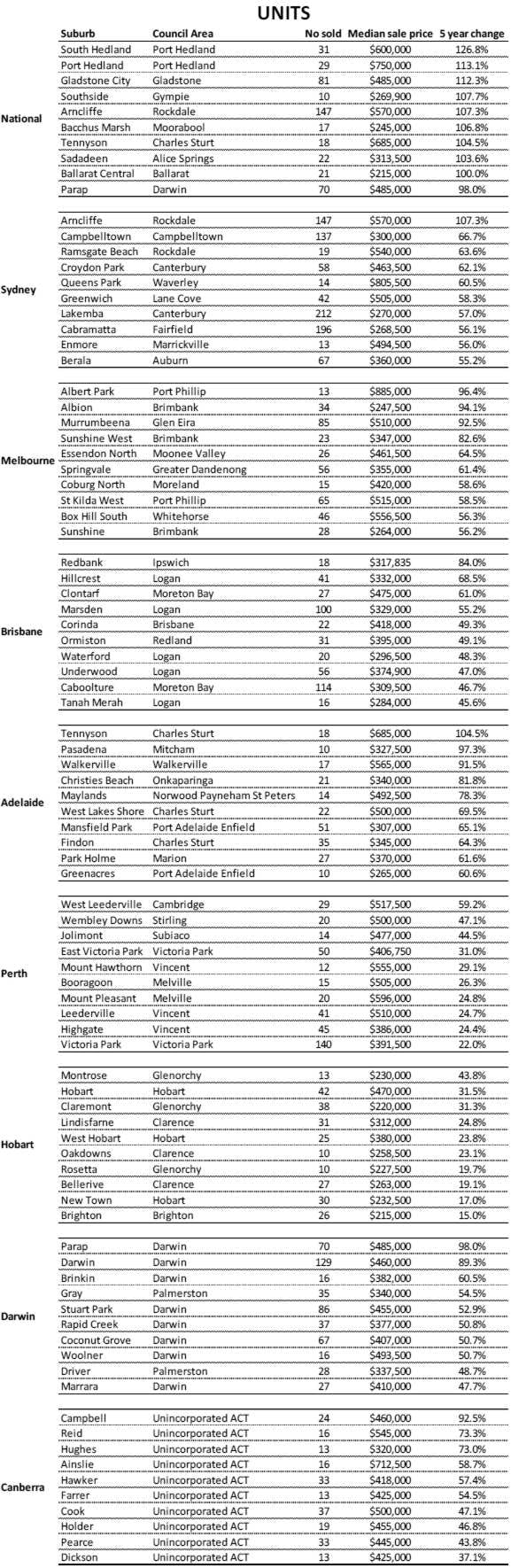

- Greatest increase in median selling price over the past five years

- Highest median weekly advertised rental rates

- Most affordable median weekly advertised rental rate

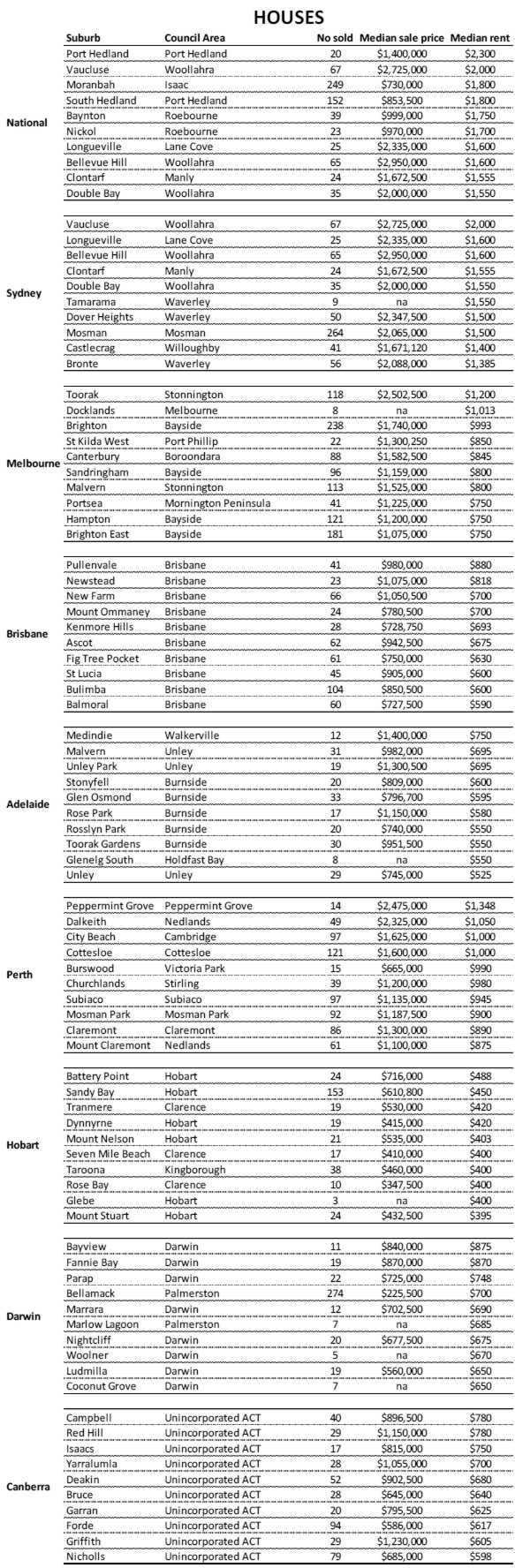

- Highest gross value of sales

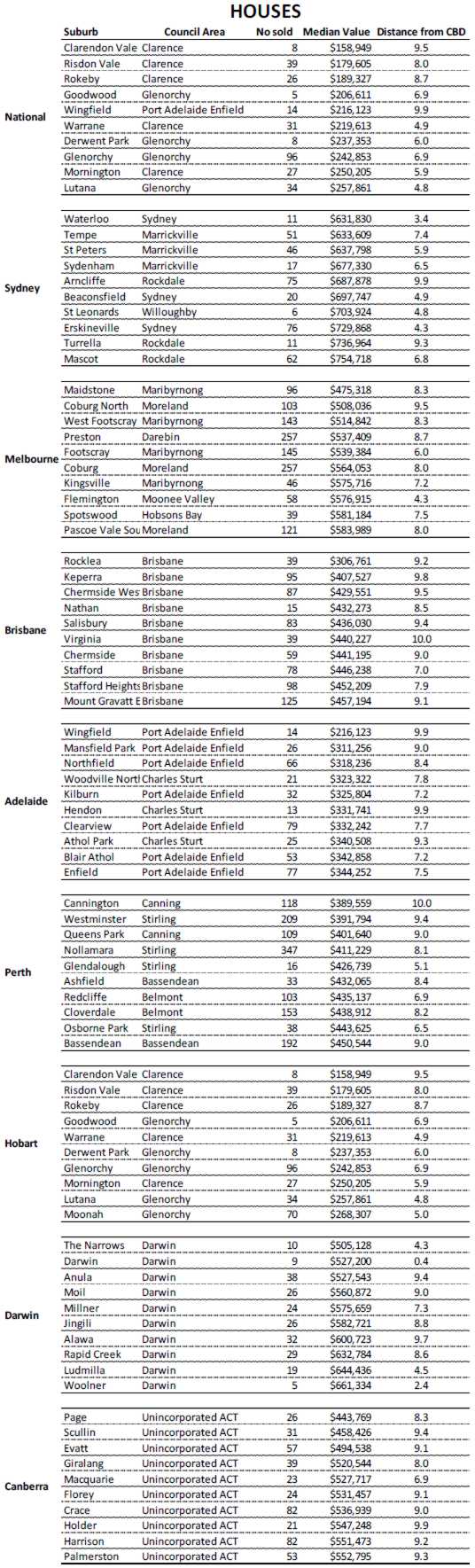

Highest median value

Source: RP Data

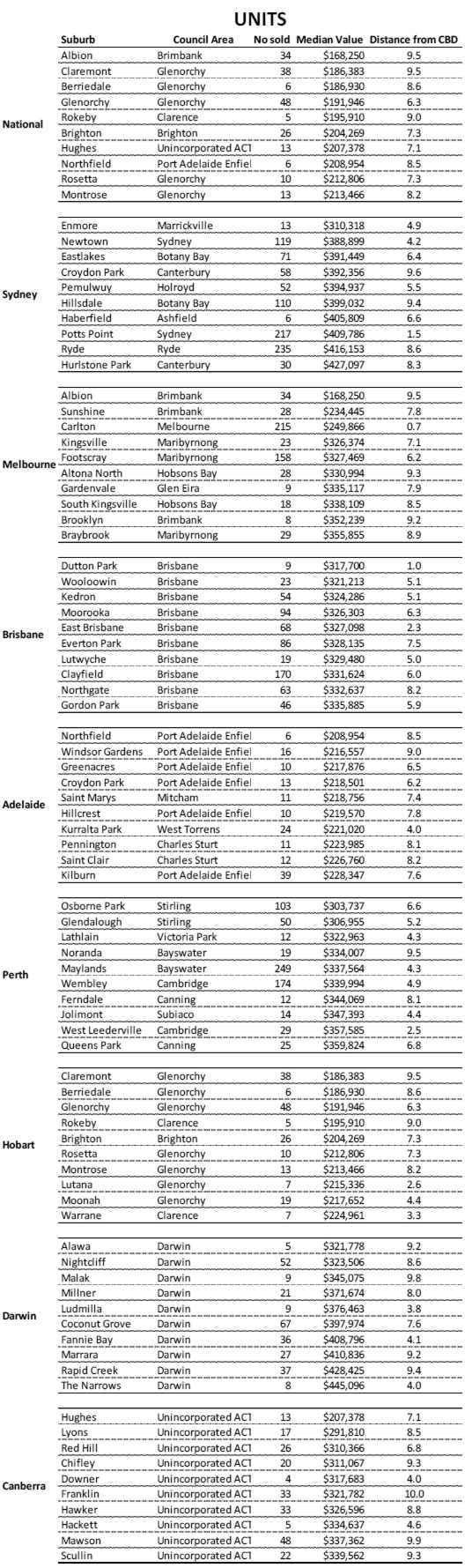

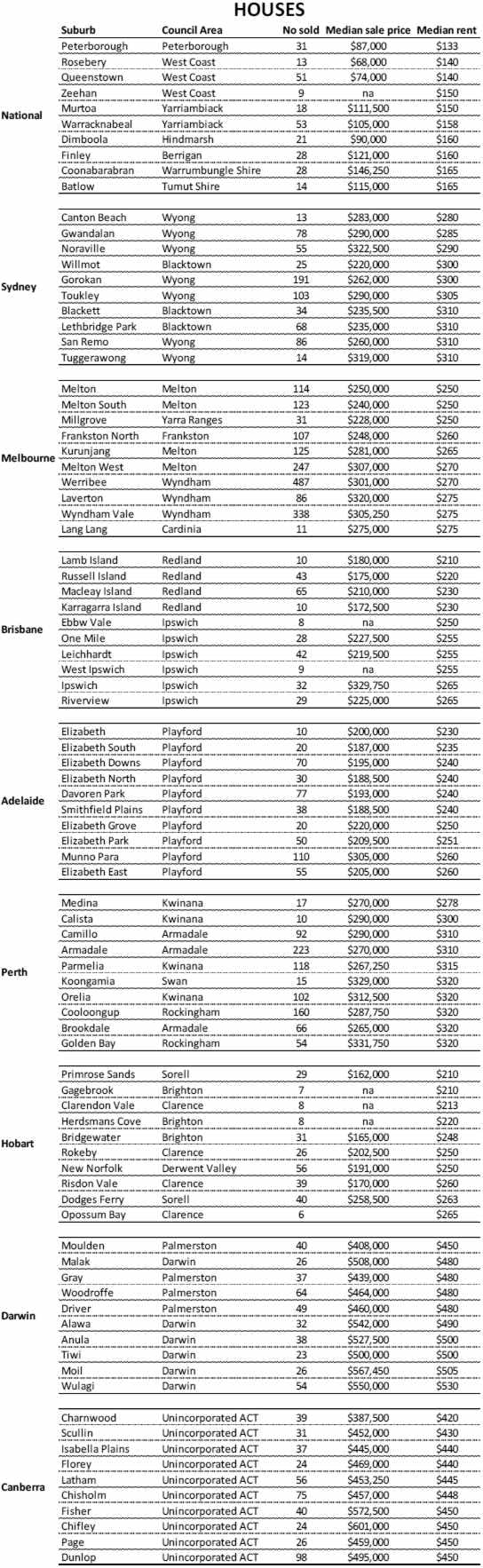

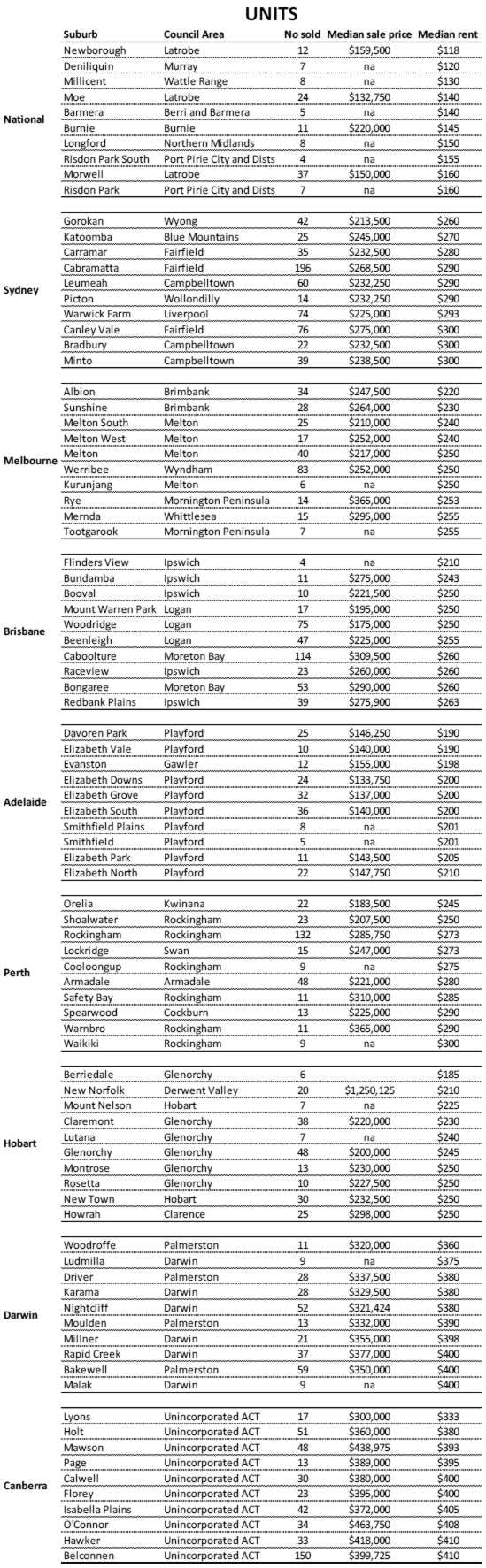

Most affordable median value

Source: RP Data

Most affordable median sale prices within 10km of the capital city

Source: RP Data

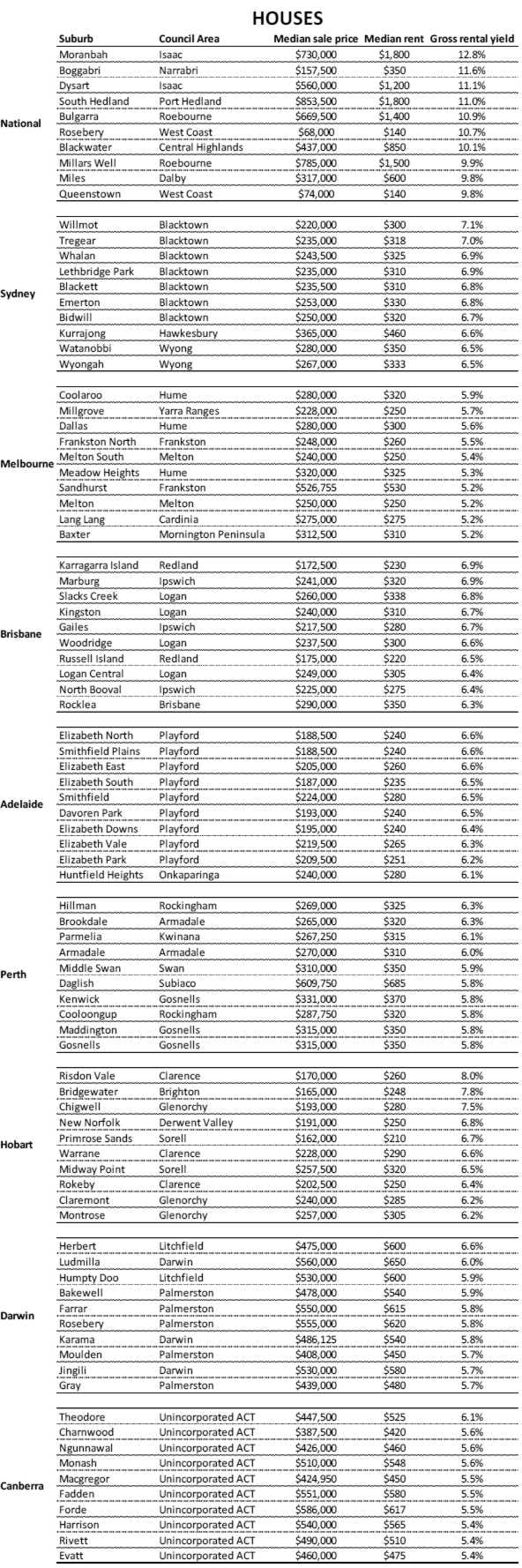

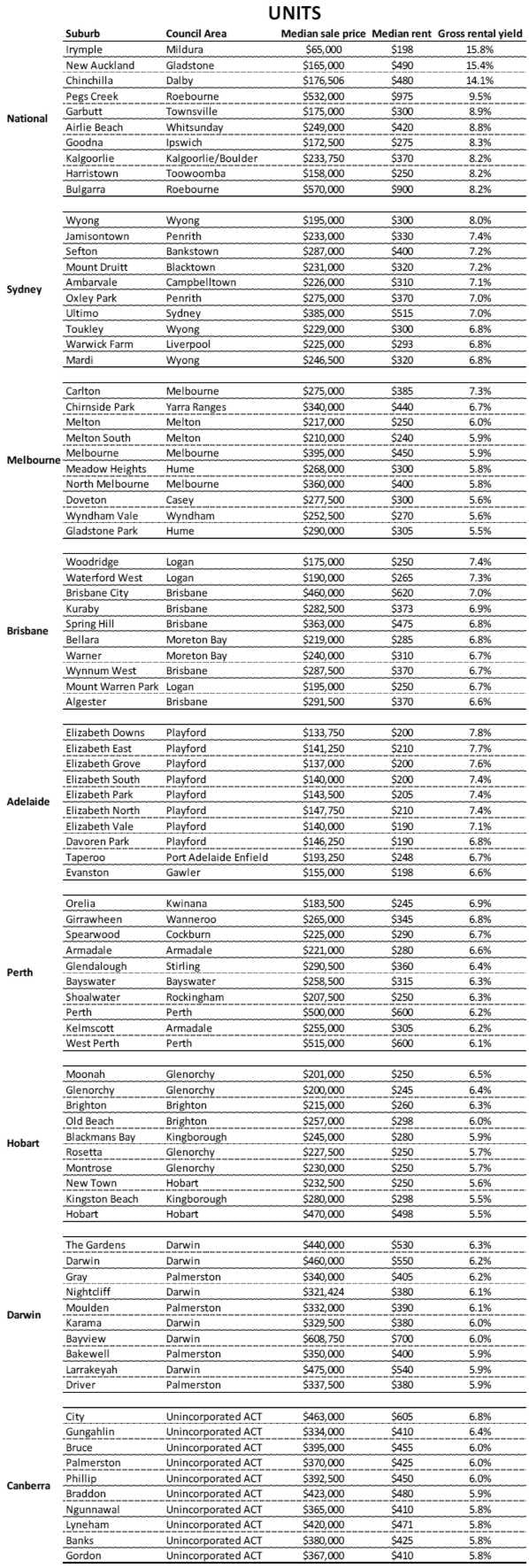

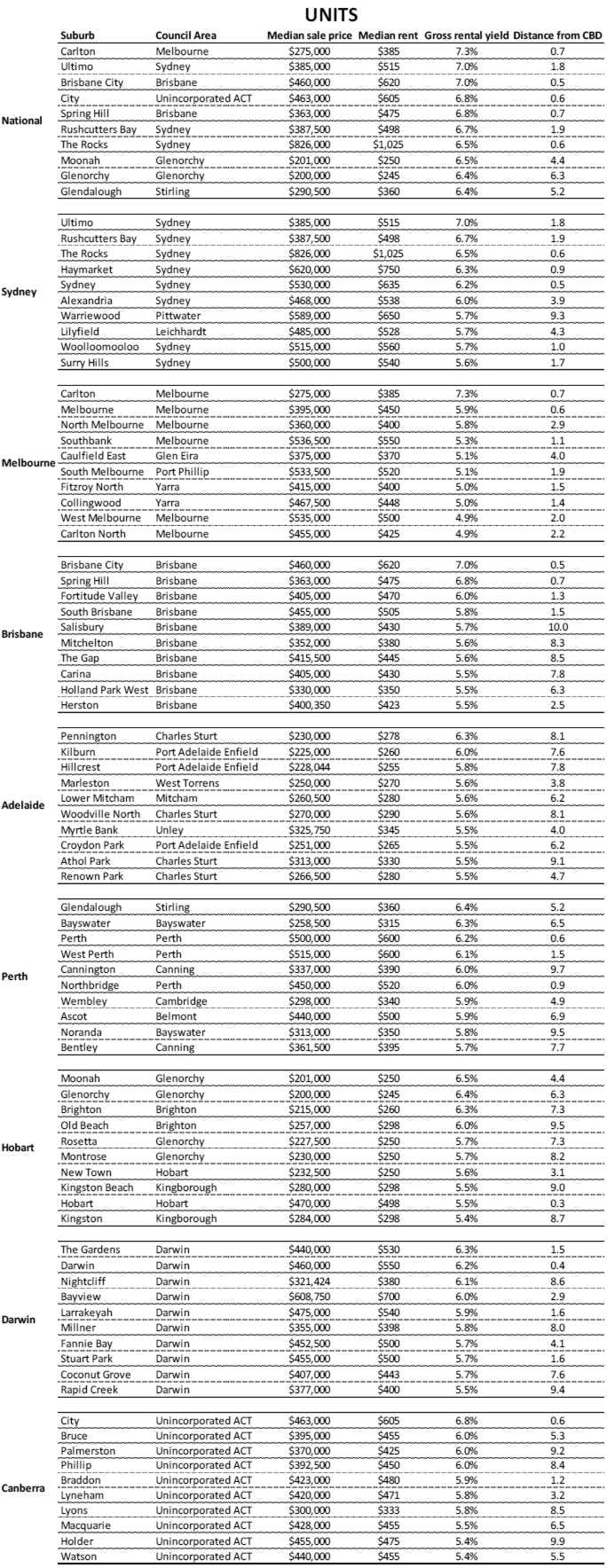

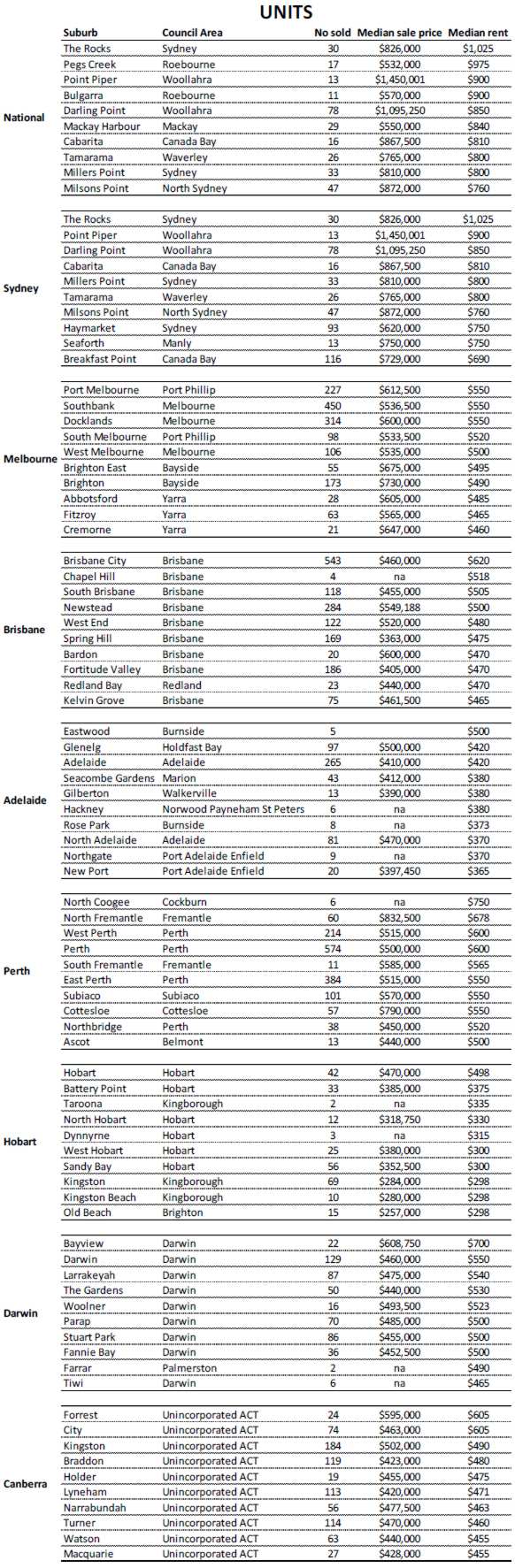

Highest indicative gross rental yields

Source: RP Data

Highest indicative gross rental yields within 10km of the capital city

Source: RP Data

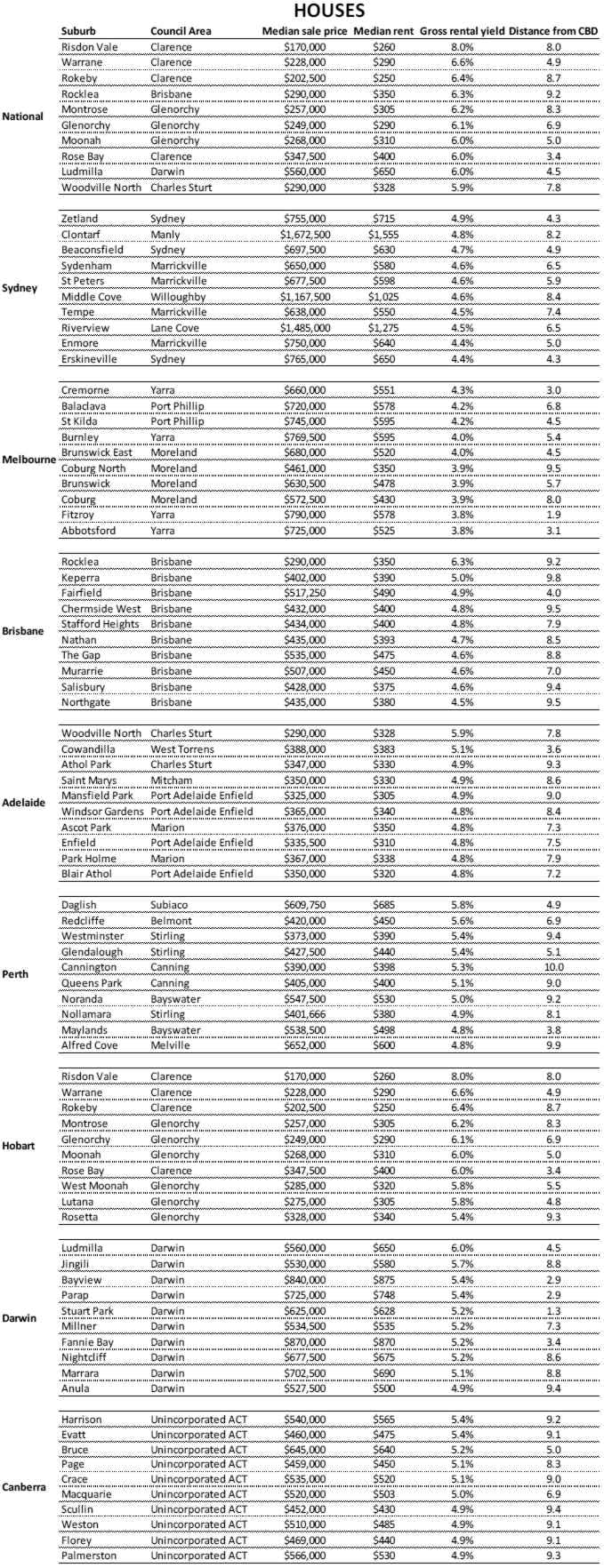

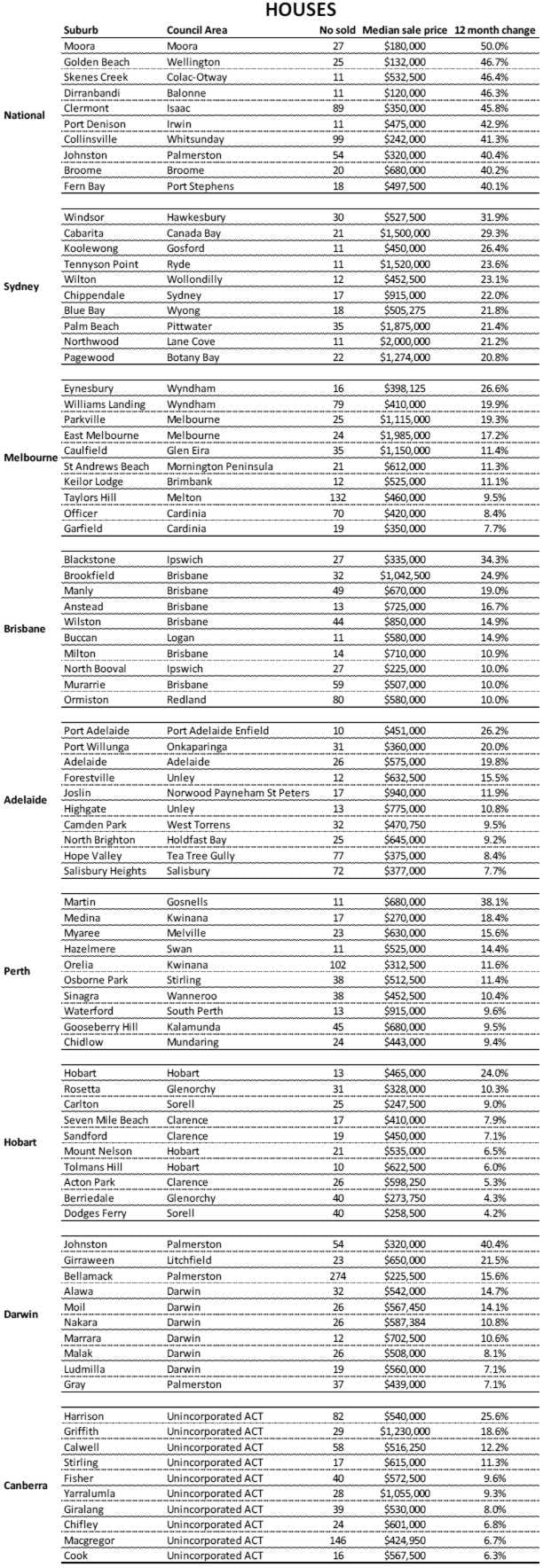

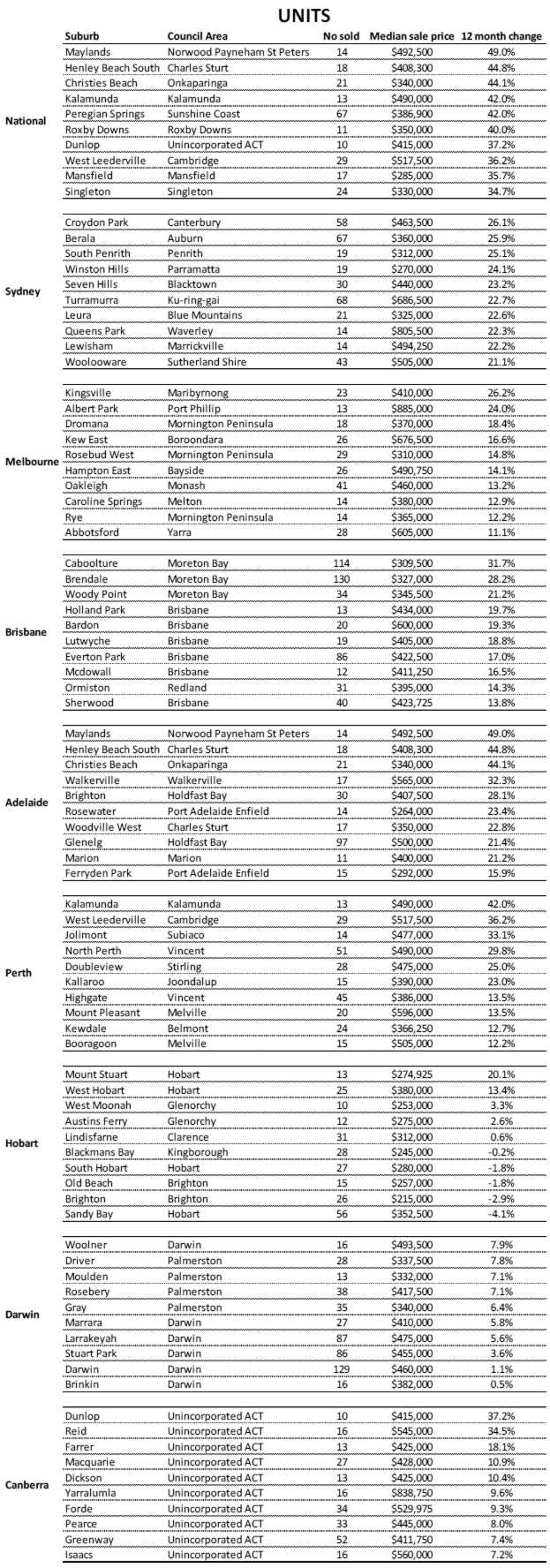

Greatest increase in median selling price over the past 12 months

Source: RP Data

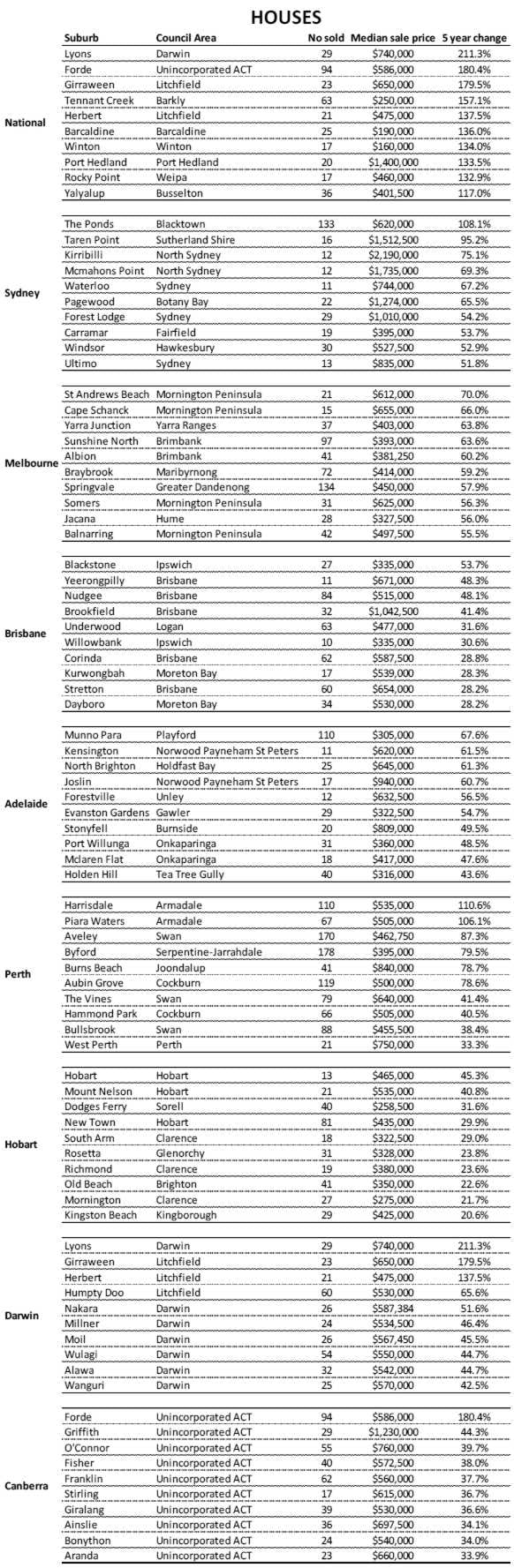

Greatest increase in median selling price over the past five years

Source: RP Data

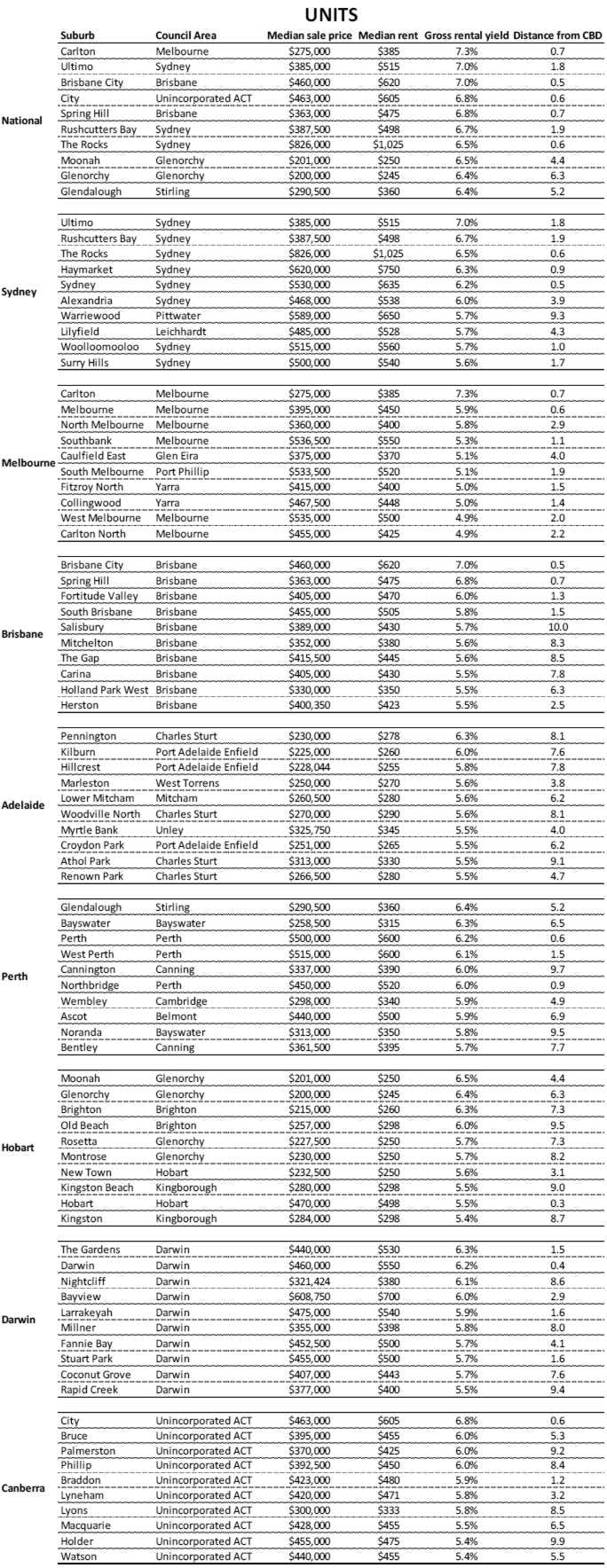

Highest median weekly advertised rental rates

Source: RP Data

Most affordable median weekly advertised rental rate

Source: RP Data

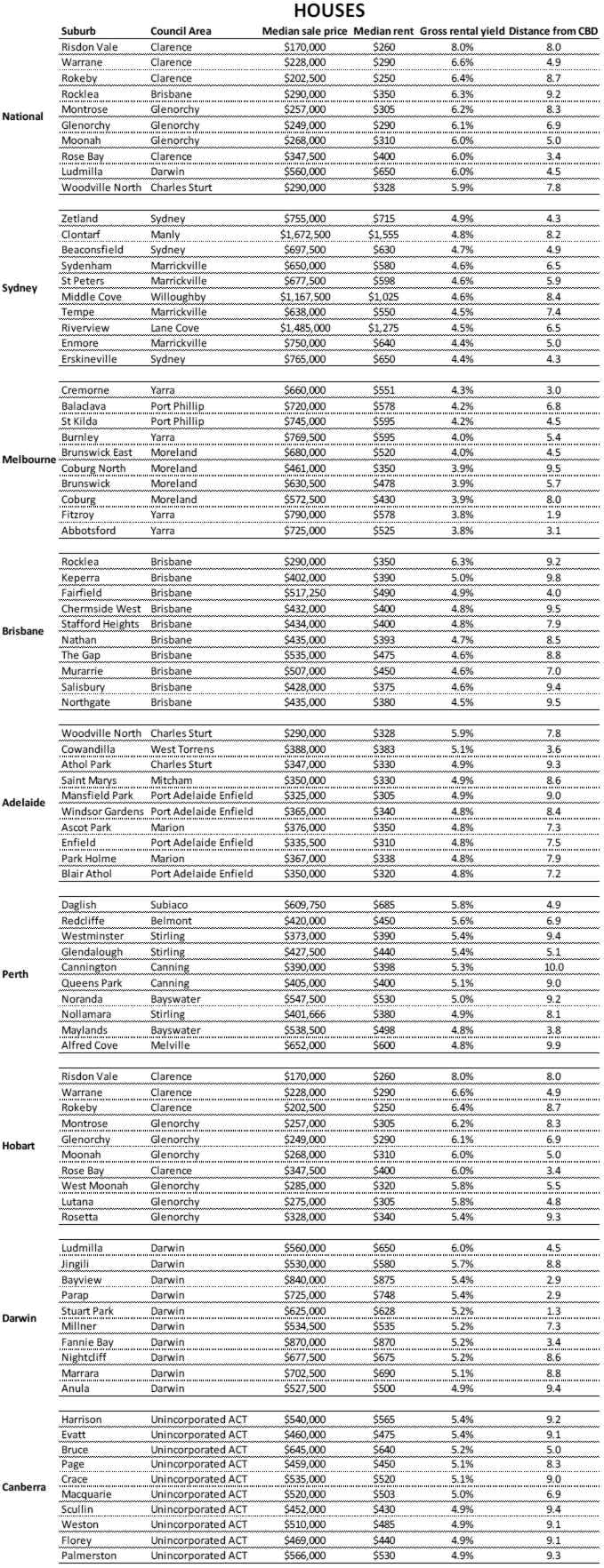

Highest gross value of sales

Source: RP Data

This article originally appeared on SmartCompany.