The merits of a value-add property strategy

GUEST OBSERVATION

Value-add property includes a range of investment strategies, including buying assets at a discount to replacement costs; undertaking a releasing strategy; renovation and refurbishment of assets; redevelopment; strata subdivision of a property; land subdivision and rezoning of an industrial site.

Returns are delivered through the capture of market valuation enhancement as a consequence of insightful property management and capital expenditure, by improving property utilisation and improving occupancy. Upon completion the upgraded property asset may generate a higher and more reliable income.

Return and Factor Characteristics

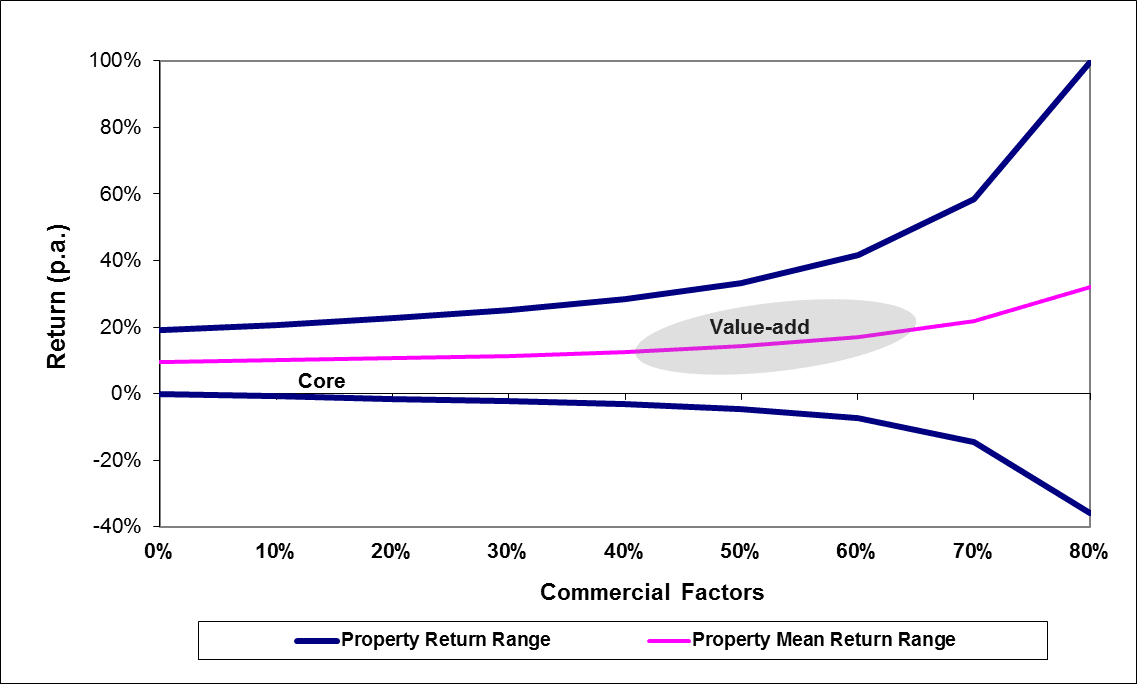

Commercial factors associated with value-add property imply a periodic absence of income reflecting the time engaged in negotiating and concluding leasing or sale outcomes or implementing other value add strategies. The prospective return characteristics of value-add property and core property across the property spectrum are shown in Figure 1.

Figure 1: Effect of Increasing Commercial Factors

Source: Atchison Consultants

Investment strategies illustrated in Figure 1, being core and value-add, exhibit different property factors and reflect increasing risk for which investors seek a higher return. Value-add property investment sits at the higher end of the spectrum, indicating an expected internal rate of return range of 12-20% per annum. Figure 1 also illustrates that as commercial risks are increased, the downside potential also increases.

Current Environment

Core property has the least risk for property investment. Given the prevailing prudent investing sentiment after the global financial crisis, these assets appealed to risk-averse investors. Investment opportunities providing enhanced returns above core property returns, may be generated by value-add property assets.

Investment in value-add property can be implemented through value-add property funds, or single asset syndicates. Participation tends to be limited to wholesale or sophisticated investors.

The conversion of secondary quality office space into residential apartments is a continuing trend. Lack of sites for residential use across capital city CBD markets, combined with softer investor demand for older office stock, has led to innovative managers offering funds which will participate in such projects.

A recent example of a value-add syndicate involved commercial office property in Sydney CBD which was 80% leased to two international corporate tenants. The building was purchased well below replacement cost reflecting a relatively poor lease structure. Value enhancement of the property is planned through upgrading the ground floor lobby entrance and external presentation of the building. This will result in the renewal of the lease with an existing tenant. In addition, the manager has identified a prospective tenant which will take the occupancy rate from 80% to 89%.

Ming Niu is an analyst at Atchison Consultants.