Prime v secondary office property: Which one is more likely to outperform?

A comparison of the performance of prime and secondary office property demonstrates that prime at 9.0% per annum has outperformed secondary office property at 8.6% per annum over the 28 years from 1985 to 2012 by 0.4% per annum. Through cyclical market fluctuations, performance outcomes vary. Secondary property returns are more volatile, however secondary office property can outperform prime property in the stable return periods and the subsequent initial upswing phase of market cycle.

Prime properties are located in major commercial centres with great public transport accessibility, built with quality design externally and internally, which are energy efficient, and have tenants which are financially strong. Absence of any of these criterion means that an asset will generally be rated as secondary property.

Total Return

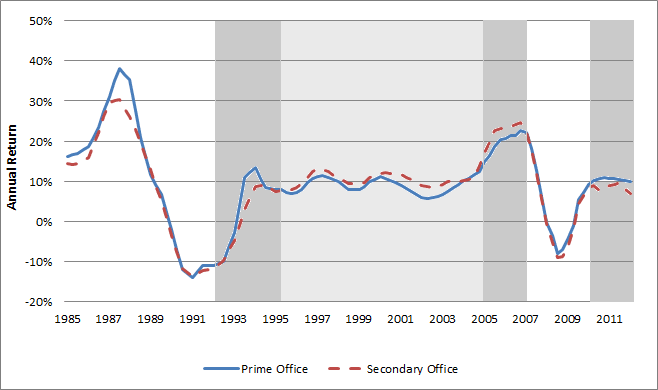

In broad terms, prime and secondary office returns have followed the same cycle over the past 28 years, indicating that that they are significantly influenced by the same fundamental demand and supply forces. Chart one compares annualised total returns for prime and secondary office property in Australia over the period from 1985 to 2012.

Chart one – Prime and secondary office property annual total return 1985 - 2012

Source: IPD

Table one compares the performance of prime and secondary property over different periods. Four periods have been selected which highlight the different market conditions.

Table one – Prime v secondary office property returns

Source: IPD

There are three key observations:

During the stable return period from mid 1990s to mid 2000s, secondary office properties outperformed. The higher risk of secondary office property through higher vacancy was rewarded through the higher returns achieved over the period reflecting the higher income yield of secondary office property.

Prime office properties have led the initial recovery in returns, however secondary offices gained more momentum in the later phases of upswings and surpassed prime property from 2005 to 2007. Investors sought higher returns and were willing to accept more risk in the positive market.

Returns for prime property have surpassed secondary property in the recovery stage from periods of weak return in the property market. Two examples are recoveries after the “recession we had to have” in early 1990s and global financial crisis (GFC) in 2008. Property market falls led investors to be more risk averse with a preference for prime properties with more secure rental income. As a result, prices of prime office property have recovered from weakness in advance of secondary office property.

Income return

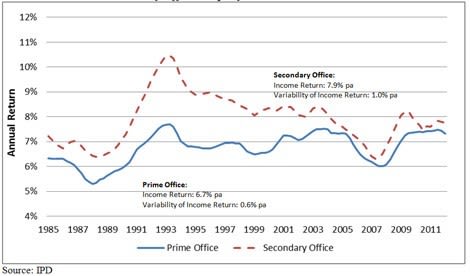

Income return provides a further performance measure that differentiates prime fraom secondary office property. Chart two tracks the changes in prime and secondary office rents from 1985 to 2012. Secondary office properties have generated a higher income return that is also more variable than prime office properties.

Chart two – Prime and secondary office property - income returns 1985 - 2012

Source: IPD

The difference in variability between prime and secondary income returns reflects the fact that prime offices fulfils the majority of market demand as an economy rebounds. However, in a sustained economic recovery, with limited availability of prime properties, tenants that could not secure or afford prime office space compromise by securing secondary property. That spill over of demand leads to improved rents in the secondary office property.

\Conversely, in an economic downturn when there is a lot of vacant space, tenants will secure prime office buildings and prime office rents will fall less than secondary rents. Secondary property will suffer more from increased vacancy. Secondary offices are generally let to less financially resilient tenants for relatively shorter terms, therefore downsizing and subsequent non-renewal of leases by tenants in a weak economy is more likely. Secondary property vacancy rates and therefore rental income are more variable.

Investment in commercial property can be implemented in a variety of ways. Prime office properties are larger in size and value and can be invested in through AREITs or wholesale unlisted property funds. Secondary properties can be invested in through retail unlisted property funds or through property syndicates.

Prime office has shown outperformance in the recent market as investors are still relatively risk averse after the GFC. Signs of recovery in corporate earnings in Australia indicate that the market is heading for a stable period. Secondary office properties will be rewarded by stable rental income at higher income yields so that higher total returns are expected in the immediate future.

Ming Niu is an analyst at Atchison Consultants.