Savills on what the future holds for Australia's office market

Australia’s main CBD markets have recorded a decline in office vacancy rates throughout the first half of 2018, with Sydney and Melbourne CBDs continuing to exhibit their strength as vacancy rates in both markets fell to their lowest levels in more than 10 years.

The findings come in the Property Council of Australia’s (PCA) release of its mid-2018 Office Market Report.

Here's Savills Australia's analysis starting with the national outlook, then state by state:

National overview

Savills Australia’s Associate Director for Capital Strategy and Research, Shrabastee Mallik, said there had been a clear difference in performance between the Sydney and Melbourne CBDs and the other main CBD markets, with the resource-reliant Perth and Brisbane office markets feeling the effects of the mining downturn until about six months ago.

“A renewal in economic growth globally in 2017 saw a renewal in demand for Australian resources and subsequent rises in commodity prices, leading to significant growth in corporate profits, particularly in the mining sector,” Ms Mallik said.

“We are now seeing this having a positive effect on the previously struggling Perth and Brisbane office markets, with subsequent falls in vacancy rates in these markets.”

Ms Mallik went on to say that a turnaround in these markets was already evident, with further improvements in 2018 likely when activity on the ground and various forward-looking economic indicators were considered.

“Low rents and high incentives in Perth and Brisbane are providing the impetus for businesses to acquire space in the CBDs, with recentralisation likely to be a key theme in the short to medium term,” she said.

“While there is concern that the Sydney and Melbourne CBD office markets appear to have peaked in terms of performance, when we consider forward-looking economic indicators, such as economic growth forecasts – particularly in the services and education sectors, which are key market-drivers for these markets – these fears would appear to be largely unfounded."

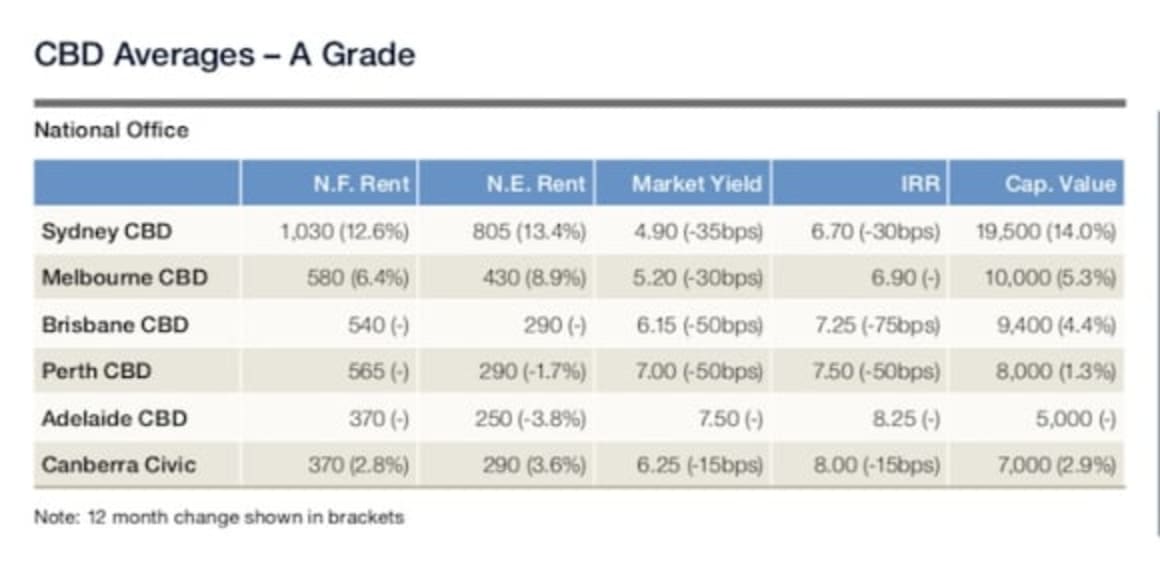

Source: Savills

New South Wales

In the first half of 2018, the Sydney CBD office vacancy rate fell to its lowest level since the Global Financial Crisis in 2008, after a steady decline for the past eight quarters.

The strength of the market has been further highlighted by face rents rising to record high levels across all grades.

“We have seen a large number of tech and IT firms centralising and organically growing in the CBD after decentralisations due to cost pressures during the 2008 to 2010 period,” Savills NSW State Director for Office Leasing in Sydney, Rob Dickins, said.

“These firms are now profitable and chasing and trying to retain talent in a very competitive industry sector."

“We have obviously also seen the emergence of co-working groups such as WeWork, Regus and Spaces, among others, which are now significant occupiers of space in the CBD.”

Mr Dickins said demand from smaller occupiers was still evident, with a spike in leasing activity in the sub-1,000sq m category, driven largely by the opportunity and capital cost savings in speculatively fitted tenancies.

“While net absorption has been low, this is largely as a result of reduced available space in this category, due to the absorption associated with government projects, and the redevelopment and change-of-use projects currently underway,” he said.

Victoria

The Melbourne CBD experienced a reduction in vacancy rate as a result of tenant migration to higher-quality office space, predominantly A Grade space, as well as some tenants taking on expansion space.

Savills Australia’s State Director for Office Leasing in Melbourne, Mark Rasmussen, said that the Melbourne CBD office market continued to maintain strong growth across all office building grades and all sectors.

“Continuing falling vacancy due to lack of supply and steady demand has resulted in maintaining the trend of increasing rentals and lower lease incentives,” he said.

“The strong economy, positive market sentiment and continued migration – of tenants to the CBD and the increasing population – is underpinning demand."

“The co-working sector, education market and growth across Melbourne’s increasingly diversified market is adding further upward pressure to rents.”

Mr Rasmussen said the fourth quarter of 2019 would see the market peak, with record low vacancy rates and rental rates continuing to climb after decades of remaining “stubbornly low”, when compared to most other Australian marketplaces.

“While the 2020 and 2021 new supply numbers are locked in and significant, the pent-up demand will see the new higher rent levels being maintained, with increases in incentives back to 2016 and 2017 levels likely,” he said.

Queensland

Following a slight spike in the total office vacancy rate in Brisbane’s CBD in December 2017, vacancy rates dropped after strong leasing activity in the first six months of 2018.

“With rents and incentives in the Brisbane CBD now very similar to the surrounding fringe office market, we have seen a number of recentralisations from large firms in the finance and insurance sectors consolidating space in the CBD, as they take advantage of large floor plates in refurbished prime grade buildings,” Savills Australia’s State Director for Office Leasing in Brisbane, John McDonald said.

South Australia

Adelaide’s CBD office vacancy rate appears to be in a holding pattern, as the “flight to quality” trend continues to partially offset the migration from potentially non-competitive space, to prime-grade space concentrated within specific buildings.

Increasing competition on the supply side for prime-grade stock had previously led to a rise in backfill vacancy within secondary space as these tenants relocated but this trend seems to be subsiding, as the gap between prime and secondary vacancy rates begins to shrink.

This observation comes on the back of owners looking to reposition buildings on a floor-by-floor basis to retain existing tenants.

Savills Australia’s Director for Office Leasing in Adelaide, Adam Hartley, said the majority of demand for office space in Adelaide was for prime-grade space, although the market was seeing lower levels of take-up.

“We are starting to see signs that incentives are tapering off, particularly for prime or refurbished space,” he said.

“We have seen examples of tenants securing a net incentive of around 35 percent – this time last year, that figure would have been around 40 percent.”

Mr Hartley said he was expecting to start seeing a shift in the technical vacancy rate in the second half of the year.

“There have been a number of economic metrics that have constrained tenant decision-making throughout the past nine months, including the state election and the last stage of abolishing stamp duty cuts for non-residential property transfers being finalised,” he said.

“On that note, there are several green shoots emerging, which will begin to benefit office take-up in the CBD – defense announcements being key, as well as general public infrastructure investment that is underway."

“These industries bode well for take-up of engineering or project space in the short-term,” he concluded

Western Australia

Perth’s office leasing market is unlikely to see any further increases in the technical vacancy rate in the medium term, as the market is no longer facing the high volume of incoming new supply that it was through 2015 and 2016.

While the period of tenants rationalising space is over, the “flight to quality” trend remains a key driver in the market, as does recentralisation back to the CBD.

Savills Australia’s Director for Office Leasing in Perth, Shelley Ritter, said demand for prime-grade space was continuing to drive a reduction in the overall vacancy rate, and it was becoming “increasingly challenging for larger tenants to secure contiguous floor options, especially in premium-grade space”.

“The differential between prime and secondary space that began to emerge mid-2015 has never been this wide, a trend which is beginning to drive down incentives, particularly in premium and A Grade space,” she said.

Ms Ritter said there had been some “marked improvements” in the state’s economy, with long-term outlooks suggesting a return to a more sustainable investment level in regards to the mining and resource sector.

“Some of the state’s biggest and best-known mining producers have announced commitments to new projects, and investment in emerging sectors such as lithium is rising,” she said.

“We know that there is circa 70,000sq m in active leasing requirements currently in the market for new or expansion space from some of these large occupiers.

“These companies will play a significant role in office take-up for the next three to five years, with indirect organic demand expected to be created on the back of this from other industries, such as finance, legal, property and business services.”

Ms Ritter said a conservative outlook would suggest that the weight of this demand, together with a “somewhat cautious” development pipeline, will contribute to a decline in vacancy rate.

“Our view, however, is that this will potentially occur much faster than the market anticipates,” she said.

Australian Capital Territory

Canberra’s office market offers stable rental growth unlike any other office market in Australia, due to the strong government sector presence, according to Pip Doogan, Savills Australia’s Director of Office Leasing in Canberra.

“While other markets are often subject to economic cycles, the nature of the government tenants in Canberra means that lessors are protected against significant rises and falls in rents,” she said.

Savills Australia data shows that on average, net face rents for Canberra’s A Ggrade assets grew 2.8 percent throughout the 12 months to June 2018, largely in line with the 10-year Compound Annual Growth Rate (CAGR) of 1.95 percent per annum.

“Interestingly, rental growth across B Grade assets was more pronounced, with net face rents growing 8.5 percent throughout the past financial year, far exceeding the 10-year CAGR of 0.7 percent per annum,” Ms Doogan said.

Ms Doogan noted that a slight increase in incentives across secondary-grade assets has meant that growth on an effective basis has been flat.

“Based on leasing deals we are currently looking at and witnessing, there appears to be a divergence in rental growth in prime and secondary grade buildings,” she said.

“Given the wide range of buildings available in Canberra (based on quality), lessees are able to negotiate more favorable terms on secondary-grade space, while the pendulum remains firmly in the landlord’s favour, particularly in those sub-precincts with record low vacancy rates.”

Source: Savills