Household debt growing slower than asset wealth as both hit record highs

Household finance data released by the Reserve Bank (RBA) each quarter looks at the ratios of household debts and assets to disposable income. The latest RBA update shows that while households debt is growing, asset wealth is simultaneously increasing.

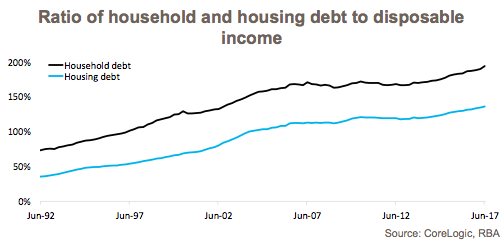

According to the RBA, the ratio of household debt to disposable income was recorded at 193.7% at the end of June 2017 and now sits at a record-high having increased by 2.0% over the quarter and by 3.9% over the year.

According to CoreLogic research analyst Cameron Kusher it was not surprising to see that most of this debt is housing related; the ratio of housing debt to disposable income is recorded at 136.4% having increased by 1.4% over the quarter and 3.9% over the year.

Kusher said, “Clearly, household and housing debt has increased over time relative to disposable incomes. Of note is that since the financial crisis, the rate of escalation has slowed.”

Further data from the RBA reveals that of the 136.4% ratio of housing debt to disposable income, 103.2% is held by owner occupiers with the remaining 33.2% held by investors.

At the end of June 2017 the ratio of household assets to disposable income was recorded at 935.6% and the ratio of housing assets to disposable income was 516.5%, both of which were record highs. Over the past year household assets and housing assets have increased by 6.6% and 7.8% respectively, well in excess of the increase in household and housing debt.

By comparing the ratios of assets and debt the RBA also produces ratios of household and housing debt to assets. Mr Kusher said, “The data reiterates that although debt levels are high, at this stage debt is well supported by assets which are valued substantially higher.”

Over recent years the ratios of household and housing debt to assets has actually been falling. In June 2017, the ratio of household debt to assets was recorded at 20.7% and the ratio of housing debt to assets sat at 26.4%.

According to Kusher, a big contributor to the declining ratio of debt to assets over recent years has been the ongoing fall in interest rates to their current lows. At the end of June 2017 the ratio of household interest repayments to disposable income was 8.7% and for housing it was 7.1%. Lower interest rates also mean that where there is a debt, debtors have the ability (if they choose) to maintain previous repayments which in turn means additional debt is repaid as interest rates fall.

He said, “The latest household finance data from the RBA highlights that Australian households are heavily indebted, largely due to housing. While debt levels are high, the value of household and housing assets are, at this stage, considerably greater than the level of debt.”

“Of course, if household and housing asset values begin to fall in the future, the accompanying debt may not fall at the same rate and that remains the main concern with the ongoing increase in household and housing debt.

“Although Australia survived the financial crisis with much less damage than many other countries, of note was the fairly sharp rise in the ratio of household and housing debts to assets over that period. A more sustained downturn could potentially see a much greater increase in these ratios as asset values fall but the debt against these assets remain,” Mr Kusher said.