The record year for house lending: Pete Wargent

Pete WargentDecember 17, 2020

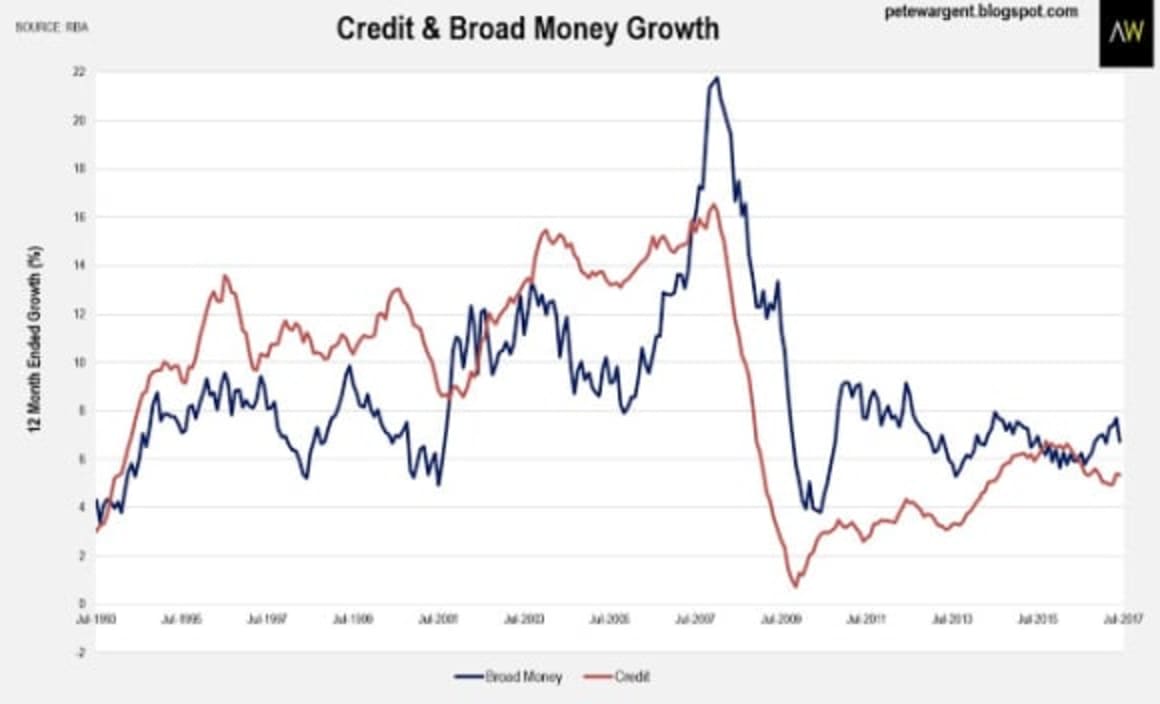

The Reserve Bank of Australia (RBA) reported credit growth of +5.3 per cent over the year to July 2017, a fair bit slower than the +6.6 per cent seen a year earlier.

The slowdown has partly been a reflection of business credit growth ambling along at an annual rate of +4.2 per cent, although surveys suggest that business investment is set to gather a bit of momentum.

Growth in credit relating to housing market investors has slowed a touch to +7.4 per cent, now well under the 10 per cent cap, with more slowing to come based on recent monthly figures.

Owner-occupier credit growth is still powering along, though, and total housing credit growth is still a sprightly +6.6 per cent, unchanged from a year earlier.

Personal credit growth remains negative, as consumers tend towards mortgage buffers and offset accounts instead of of credit cards and personal loans.

Shifts at the margin

There's no doubt that it's become more difficult at the margin to gain access to housing credit, particularly for investor loans, and most especially for interest-only mortgages.

The growth in investor loans is now well below the regulatory 10 per cent cap for each of the major banks, which between them account for most of the mortgage market.

A couple of minnow lenders have been pinged with a speeding ticket, including the tiny Heritage Bank, so they'll be putting investor loans in the sin bin, perhaps for a month or two.

A couple of minnow lenders have been pinged with a speeding ticket, including the tiny Heritage Bank, so they'll be putting investor loans in the sin bin, perhaps for a month or two.

But on the flip side, there's plenty of potential for most of the main lenders to loosen standards again for investment loans as we head into spring and beyond.

Moreover, while APRA's latest ADI monthly statistics hinted at a marginal slowdown, the reality is that non-standard loans have to some extent been picked up by alternative lenders such as Pepper and their ilk.

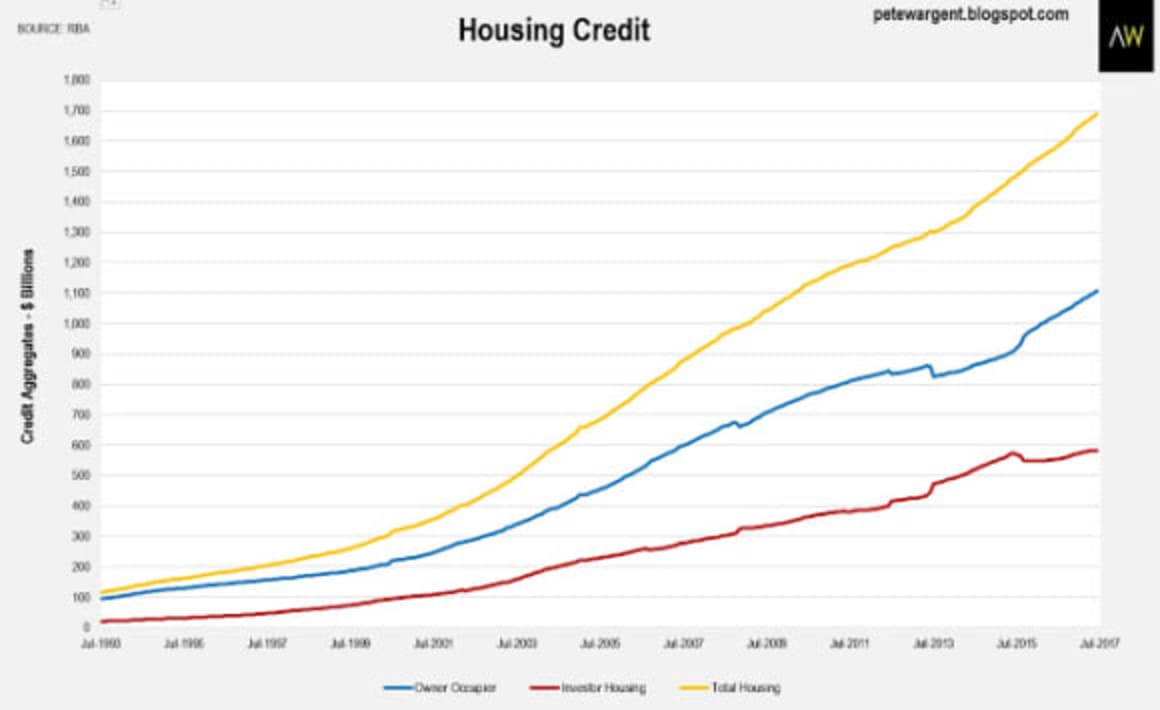

The RBA's figures show that over the year to July 2017 the total stock of outstanding housing credit increased by $113 billion to $1.69 trillion.

In dollar value terms, this is the biggest annual increase ever recorded.

In dollar value terms, this is the biggest annual increase ever recorded.

So, there may be a 'slowdown' of sorts underway, if you will, but as the above chart shows it looks like a shift in composition too.

Moreover, every single one of the main lenders continues to increase its stock of mortgages outstanding, even if there has been a move towards home loans and away from investor loans.

The wrap

Some one-track observers have noted that out of cycle rate hikes has crashed or destroyed demand for mortgage debt.

I'm not sure what data source they're using to draw that conclusion - none, most likely - but the official RBA figures shows a record annual increase in housing credit, with a slowing in investor credit just beginning to flow through to the annual data.

Experiences elsewhere in the world have shown that macroprudential measures tend to be effective for a while before borrowers and lenders find ways to get transactions happening again.

The reality is that, in aggregate, interest rate differentials have only slowed lending slightly at the margin to date, while simultaneously boosting the bottom line and equity of gleeful banks.

Out of cycle rate hikes were certainly never about funding costs, with the cost of wholesale debt barely having broken a decade-long downtrend.

Out of cycle rate hikes were certainly never about funding costs, with the cost of wholesale debt barely having broken a decade-long downtrend.

What would genuinely change the landscape would be a statement of intent from the RBA in the form of a hike in the cash rate, but in all likelihood that remains far away.

In the event a couple of dozen lenders have already cut their mortgage rates since the beginning of July, most notably Westpac, in anticipation of the spring selling season.

With the trend unemployment rate declining to its lowest level in more than four years and further improvements expected over the next few ahead by the RBA, it will be intriguing to see how claims of a 'perfect storm' and 'record mortgage stress' are reconciled with what's actually happening on the ground.

I say that because it looks suspiciously as though mortgage default rates are refusing to rise from benign levels outside Western Australia.

Naturally, household cash flows may appear weaker if accelerated mortgage repayments have become the norm.

But the statistics show that although wages growth has been weak, the unemployment rate has been falling, and underutilisation is declining in volume terms.

Genuinely, I'm intrigued to watch what the media will report having run so hard with the unprecedented mortgage stress meme.

Not everyone agrees with the improving economy thesis, mind.

Westpac sees the pullback of Chinese apartment investors leading to a sharp slowdown in residential construction and unemployment heading back towards 6 per cent next year.

Watch, this, space!!!

With the trend unemployment rate declining to its lowest level in more than four years and further improvements expected over the next few ahead by the RBA, it will be intriguing to see how claims of a 'perfect storm' and 'record mortgage stress' are reconciled with what's actually happening on the ground.

I say that because it looks suspiciously as though mortgage default rates are refusing to rise from benign levels outside Western Australia.

Naturally, household cash flows may appear weaker if accelerated mortgage repayments have become the norm.

But the statistics show that although wages growth has been weak, the unemployment rate has been falling, and underutilisation is declining in volume terms.

Genuinely, I'm intrigued to watch what the media will report having run so hard with the unprecedented mortgage stress meme.

Not everyone agrees with the improving economy thesis, mind.

Westpac sees the pullback of Chinese apartment investors leading to a sharp slowdown in residential construction and unemployment heading back towards 6 per cent next year.

Watch, this, space!!!

PETE WARGENT is the co-founder of AllenWargent property buyers (London, Sydney) and a best-selling author and blogger.

His latest book is Four Green Houses and a Red Hotel.

Pete Wargent

Pete Wargent is the co-founder of BuyersBuyers.com.au, offering affordable homebuying assistance to all Australians, and a best-selling author and blogger.

Tags:

Home Loans