Investor lending gathers pace as dwelling values surge higher: Cameron Kusher

GUEST OBSERVER

Interest rate cuts and the return of lending to investors over the past year have seen a re-emergence of investors as a dominant force in the national housing market.

At the end of last week the Australian Bureau of Statistics (ABS) published housing finance data for January 2017 and it showed that at that time, demand from the investment segment of the market was continuing to surge. Pairing the housing finance data with the Reserve Bank’s (RBA) lending aggregate data provides deeper insight into housing investor behaviour.

The January 2017 housing finance data showed that over the month, investors committed to a total of $13.8 billion in finance for investment properties. The figure represented a 4.2 percent rise over the month and a 27.5 percent increase year-on-year (the largest annual increase since August 2014).

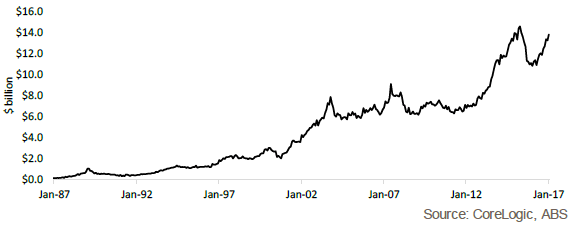

The first chart shows that the value of investor housing finance commitments remains below its previous peak but has ramped-up significantly over the past 12 months. In fact, the value of investor housing finance commitments in January 2017 was just -5.3 percent lower than its historic peak in April 2015.

Monthly value of investor housing finance commitments

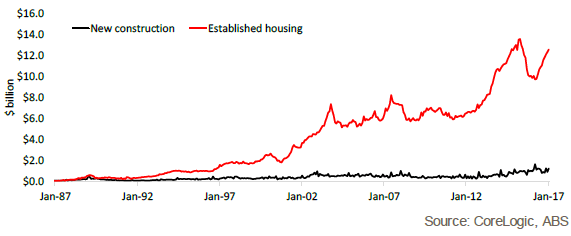

The second chart highlights how most of the investor housing finance commitments are flowing to established homes rather than new homes. This isn’t really a surprise when you consider that the amount of established housing stock is substantially greater than new stock and new housing typically has a price premium over existing stock. Over the month, $1.2 billion in commitments were for new construction compared to $12.6 billion for established housing stock.

Monthly value of investor housing finance commitments by property type

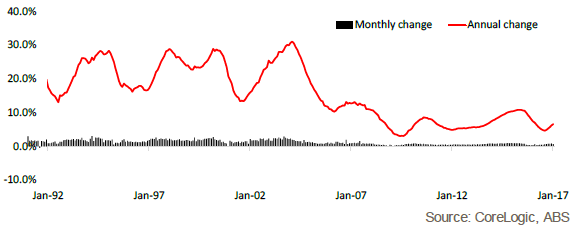

The third chart comes from data published by the RBA on investor housing credit which represents the total amount outstanding to mortgage lenders for the purposes of investor housing. In January 2017, investor credit expanded by 0.6 percent to be 6.6 percent higher over the year. The monthly change was actually the lowest it has been in four months while the annual change was the highest it has been in 10 months.

Much like the housing finance data, the credit data shows the impact of APRAs recent curbs to investor credit growth which have slowed growth however, more recently credit has once again started to expand.

Monthly and annual change in investor housing credit to Australian lenders

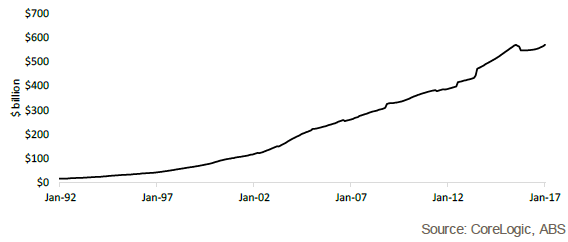

The final chart shows the monthly value of investor credit outstanding to Australian lenders. At the end of January 2017, the RBA reports that there was $572.2 billion in investor credit outstanding to Australian lenders. This figure accounted for 34.9% of all housing credit outstanding ($1.637 trillion) and 21.5 percent of total outstanding credit. The chart shows a significant rise in investor housing credit, in fact, two decades ago investor credit represented 21.8% of total housing credit and 8.7 percent of all credit.

Monthly value of investor housing credit to Australian lenders

All of the data presented highlights that the latest data we have shows demand from the investor segment in the housing market continues to surge. With the substantial increase in dwelling values in Sydney and Melbourne over recent years, home owners are able to utilise the equity in their principal place of residence to purchase investment properties. It is clear from the data that many are doing so.

While investor activity is rampant, the proportion of total housing finance commitments to owner occupier first home buyers is at an historic low. On one hand it is positive that home owners are investing on the other hand they can continue to outbid those people that don’t already own homes further locking many potential buyers out of the housing market.

It is anticipated that over the coming months we will see further tightening of lending policies to investors with some lenders approaching APRAs 10 percnet speed limit. Should this occur it is likely to result in a moderate slowing of demand from the investment segment, at least temporarily like we saw in mid-2015 and early 2016.

Cameron Kusher is research analyst for CoreLogic. You can contact him here.