International brands putting local retailers under the pump: CBRE

Australia’s retail sales performance was weaker in 2016, averaging 3.2% growth compared to 4.3% in 2015, according to CBRE’s latest report.

Most retail categories are underperforming their long-term averages.

A two-tier market is evident with international retailers expanding while some incumbent, domestic retailers are under pressure.

“Conditions in 2017 are expected to be slightly more challenging than in 2016; we expect only moderate rent growth of between 1%-2% across most retail property categories,” the report stated.

"Australian retailers have faced various challenges in the post-GFC period. First the GFC and then weak trading conditions from 2010 to 2013 caused many retailers to reduce operating costs and undertake consolidation.

"Then as these challenges were beginning to fade, the last three years saw new competition aggressively emerging from international brand entrants, who continue to gain market share, resulting in profit margin pressures for domestic retailers."

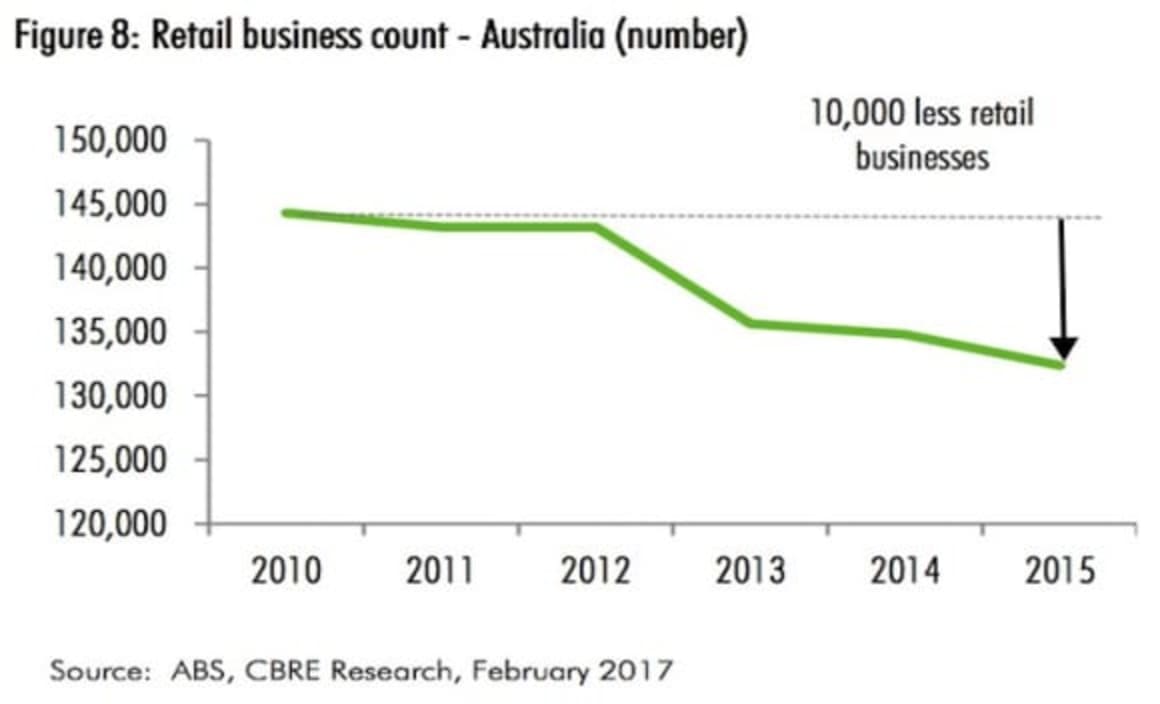

Competition has seen closure of over 10,000 retail businesses since 2010. The success of some international brands has been their ability to offer diversity of products at competitive pricing.

The entry of fast fashion international retailers has coincided with weaker sales performance of incumbent department stores and discount department stores over the past three years.

In the face of tougher conditions, some domestic retailers have responded by altering their offering to remain competitive.

For example, Myer and David Jones have closed underperforming stores and have adopted new store formats (downsized stores, fewer products and better quality) for existing and new stores.

Other retailers including some discount department stores have been slower to adapt and are reportedly facing less certain futures.

"A combination of factors are acting as headwinds for retail," the report says.

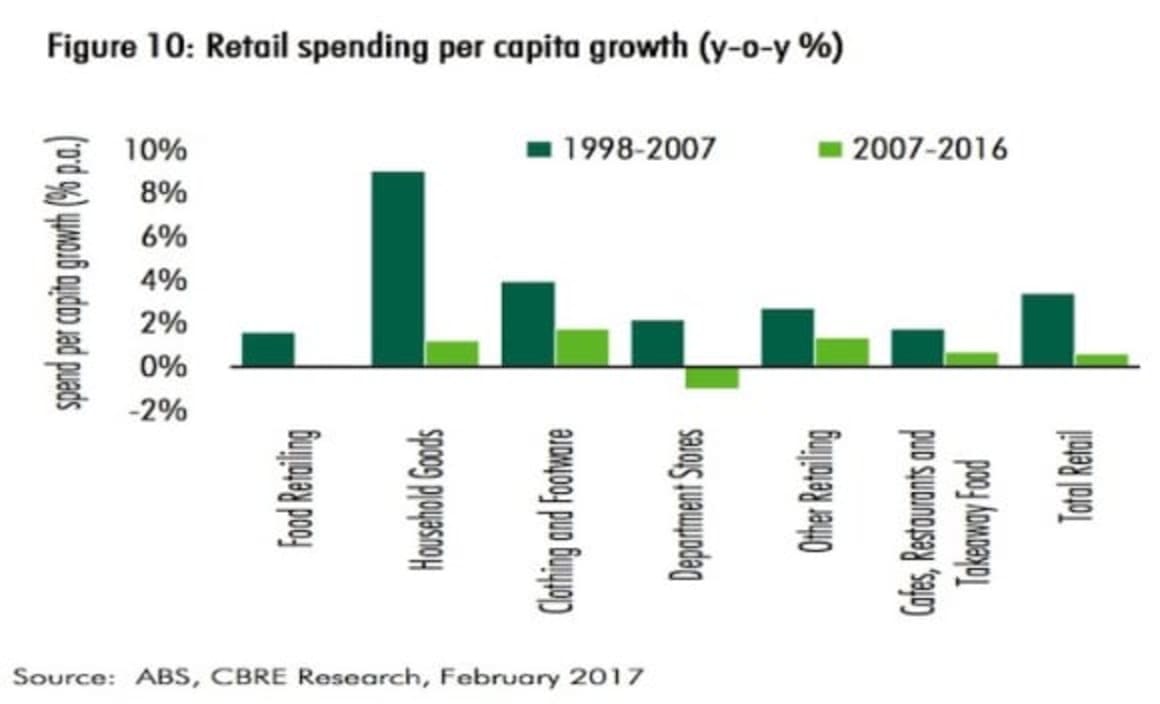

Over the past decade spending per capita grew a mere 0.6% per annum, and households aren’t funding consumption with debt to the extent they were prior to the GFC."

Population growth slowed to 1.4% annually over the last two years compared to 2% between 2004-2013.

"The combination of these factors will contribute to slower retail sales growth in 2017, and with an expected increase in international brands, domestic retailer profit margins are likely to incur further pressure,” the report stated.

"We have already seen profit margins fall for discount department stores (except for Kmart which has reset its strategy), apparel retailers and supermarkets during the past five years."

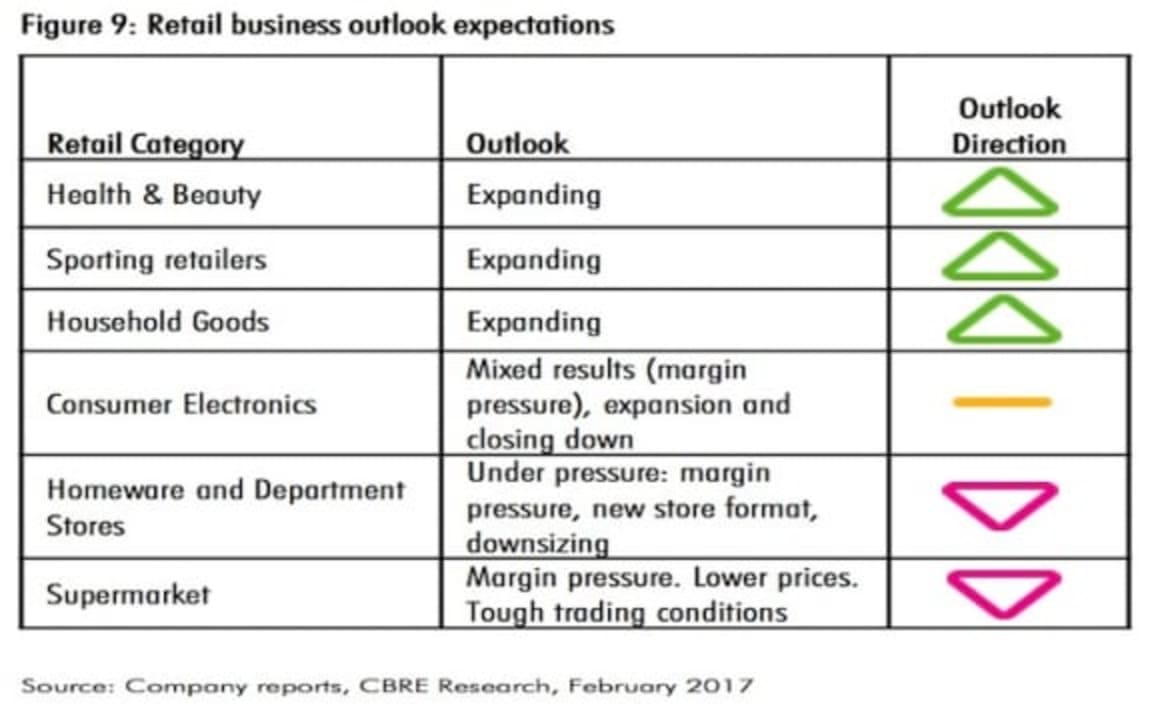

According to company reports of most listed retail companies, the sectors with the most negative outlooks are supermarkets and homewares and department stores.

Health and beauty and sporting retailers have a more positive outlook. Although retail trade growth was lower overall in 2016, there was positive news in the increase in spending in cafes, restaurants and takeaway food.

This suggests a preference shift to eating out, and this category has also benefitted from higher volumes of international tourists.

Lifestyle preferences such as convenience and shopping experience (especially amongst younger demographics) are driving upgrades in food courts and higher quality food offerings.

As a result, eating out is on average costing more but is being supported by consumer preference.