New South Wales and Victoria economic growth leads to increased office demand: CBRE

The office market in 2016 witnessed more divergence between the southeast markets and the resource-based states with the trend likely to continue in 2017, according to commercial real estate firm CBRE’s latest report.

Strong economic growth in New South Wales and Victoria led to increased demand in the office sector.

Queensland and Western Australia continued to lag, although Brisbane has stabilised and will be on the road to gradual recovery in 2017, while Perth is expected to bottom.

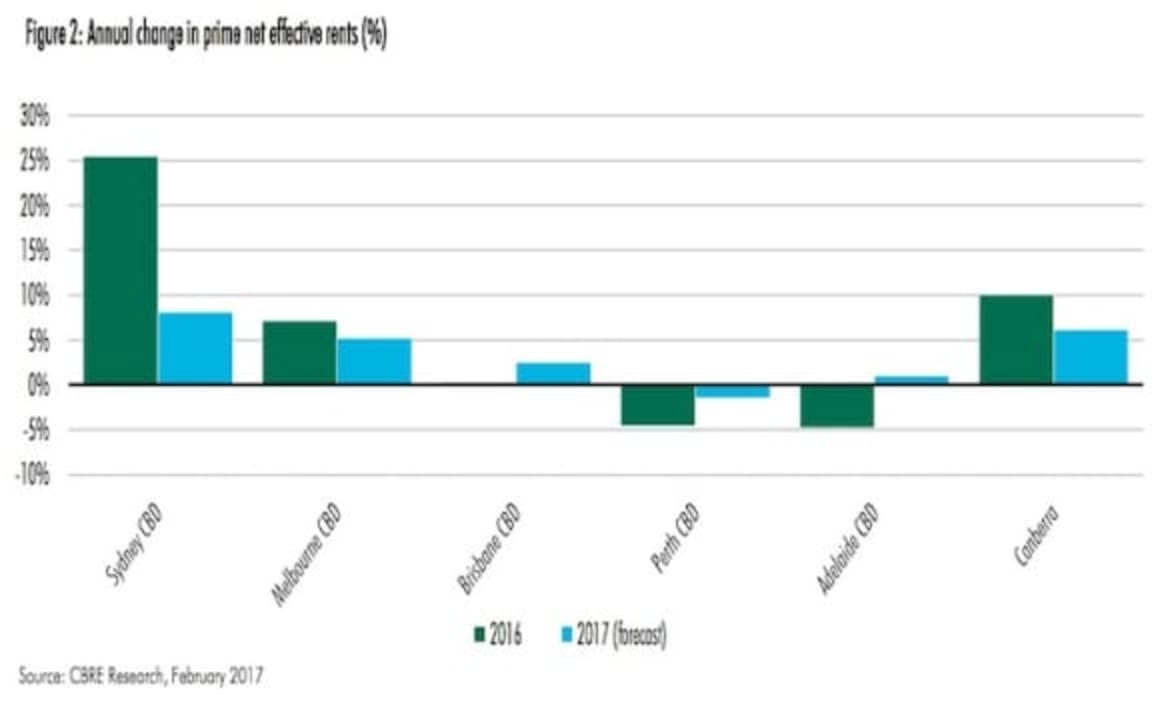

Office markets in Sydney and Melbourne performed well in 2016. Sydney CBD, in particular, outperformed with its strongest level of net effective rental growth in over 20 years.

Net effective rents (NER) grew 25 percent in the prime grade sector.

The Sydney CBD secondary grade office market set new records in 2016: vacancy fell to record lows, NERs grew 32 percent and indicative secondary rents topped $600/sqm for the first time ever.

Stock withdrawals affected the secondary market more significantly, helping deliver these results.

The prospect of limited supply over the next three years, strengthened by high withdrawal activity, in conjunction with steady growth in the services sector will continue to keep vacancy constrained.

The Melbourne CBD office market set new records in 2016 in terms of investment metrics.

Prime and secondary yields reached new lows at 5.5 percent and 6.2 percent respectively, and the spread between the two grades narrowed to a record level.

Further, albeit minor, compression is expected in H117 before yields bottom.

VIC’s strong economic growth drove white collar employment (WCE) and thus demand for office space.

Melbourne CBD achieved the highest level of positive net absorption of all states over 2016 with 117,253 sqm.

Most of this strength was captured in the last half of 2016 and resulted in vacancy declining to 6.4 percent at year end.

This helped the Melbourne CBD market achieve NER growth after four years of declines due to rising incentives.

A combination of above-average face rental growth and slight easing of incentives saw prime and secondary NERs grow 7.2 percent and 6.3 percent respectively in 2016.

"With limited supply in 2017 and demand expected to remain healthy, we forecast further NER growth in 2017 (Figure 2),” the report said.

The QLD economy has overcome the drag of the LNG CAPEX unwind and returned to growth in 2016.

“We expect further gradual improvements in 2017,” the report stated.

The advancement towards a possible 2017 construction start for the $21.7 billion Carmichael mine project by Adani has provided some confidence to the medium-term outlook, although the project represents only a fraction of activity sparked by the three recent LNG projects.

Brisbane CBD vacancy peaked in 2016 but then tightened to 15.3 percent by year-end due to its strongest annual absorption ever recorded (94,601sqm).

The latest supply cycle has completed and 2017-18 is expected to see low levels of supply in the CBD and Near City markets.

“We forecast a gradual fall in vacancy despite the strong absorption outcome in 2016, partly due to at least two further major tenant relocations to the Near City market,” the report said.

The Perth CBD office market appears to be approaching the bottom of the cycle: vacancy has probably peaked at 22.5 percent, leasing activity has picked up, and the rate of rental decline slowed substantially over 2016, with Q416 net face and effective rents remaining static.

The market is starting to benefit from tenant migration from fringe and suburban locations as businesses take advantage of lower rents and higher incentives by upgrading accommodation in a flight-to-quality.

This has led to an increase in the number of CBD leasing transactions.

The SA economy in 2016 was bolstered by public investment and also surprising growth in private consumption and retail trade.

These impacts will pass in 2017 and economic growth will moderate. The Adelaide office market remains steady with vacancy hovering at around 16%.

“Net absorption was weak in 2016 and we don’t expect much improvement in 2017,” concluded the report.

Limited supply (in the form of refurbishments) will help the vacancy rate tick slightly lower.

The ACT recorded the highest growth in State Final Demand of all the state and territories in the year to Q316, which supported Canberra CBD white collar employment growth of 3.4 percent over the same period, more than any other CBD market in Australia.

Limited new supply has resulted in vacancy trending downward since 2015 – a trend expected to continue over the medium term, posing a favourable outlook for the Canberra market.

Although softer tenant demand is expected in major office markets in 2017, the outlook for Australia’s office sector is favourably impacted by the lowest level of net supply additions in 20 years.

National CBD vacancy will begin to trend down and we forecast it to reach 9.8 percent by year-end 2017.

CBRE Research’s near-term view of office market return expectations (annualised 3-year NER growth plus yield as at December 2016) for each market is illustrated in Figure 3.

“This return calculation assumes static yields so paints a clear picture of our NER growth expectations. "We forecast that the best performing markets in Australia will be: Melbourne CBD, Macquarie Park, Parramatta, Canberra CBD and Sydney CBD,” the report concluded.