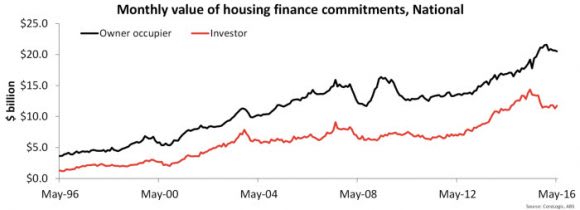

In May 2016 there were $20.5 billion worth of owner occupier housing finance commitments and $11.7 billion worth of investment commitments. Owner occupier commitments fell by -0.6 percent over the month but were 15.4 percent higher year-on-year. Conversely, investor housing finance commitments increased by 3.9 percent over the month and are -13.3 percent lower year-on-year.

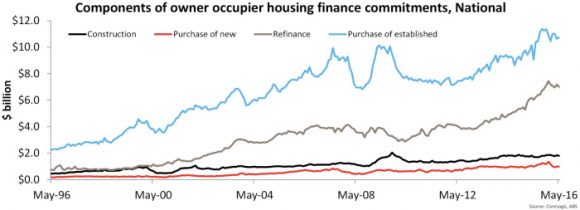

The $20.5 billion in housing finance commitments by owner occupiers was both lower over the month and -4.9 percent lower than the December 2016 peak of $21.6 billion worth of commitments. Across the components of owner occupier housing finance commitments there was $1.8 billion in commitments for construction of dwellings, $1.0 billion for purchase of new dwellings, $7.0 billion for refinances of established dwellings and $10.7 billion for purchase of established dwellings.

Each segment of owner occupier mortgage lending except for purchase of established dwellings fell over the month with each segment now also lower than the recent peak. The respective declines are recorded at -3.8 percent for construction of dwellings, -27.0 percent for purchase of new dwellings, -5.9 percent for refinancing of established dwellings and -5.6 percent for purchase of established dwellings.

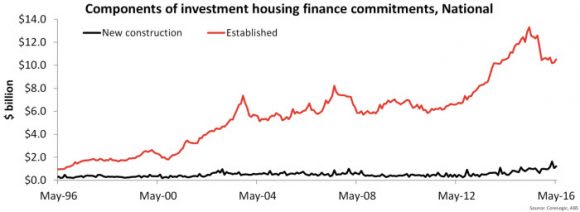

There was $11.7 billion worth of investment housing finance commitments in May 2016 which is -18.2 percent lower than its $14.4 million peak in April 2015. Looking at the components, there was $1.2 billion worth of commitments for construction of dwellings and $10.5 billion in commitments for established housing. The value of commitments for construction of dwellings was 15.5 percent higher over the month and 22.4 percent higher year-on-year. Meanwhile, the value of commitments for established housing was 2.7 percent higher over the month and -16.1 percent lower year-on-year.

Since mortgage lenders began to implement investment lending changes to slow annual investment credit growth below 10% there has been a significant slowing in lending to this segment.

The May 2016 housing credit data from the Reserve Bank (RBA) shows that investment credit has advanced 6.0% which is its slowest annual increase since July 2013 and well below 10% annually. Perhaps this is why investor lending picked up in May with mortgage lenders now having more scope to lend to investors.

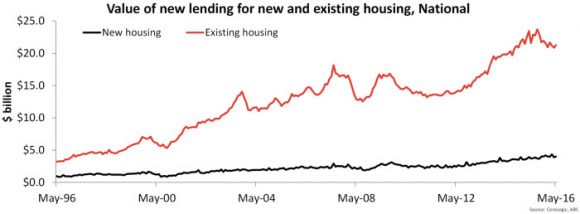

Looking at the value of new lending (excluding refinances) for new housing and established housing shows that in May 2016, $4.0 billion was for new housing and $21.3 billion was for existing housing. Based on this data, 15.9 percent of total lending over the month was for new housing with the remaining 84.1 percent for established housing.

Of this $4.0 billion in lending for new housing, $1.2 billion or 30.6 percent was lending for investment purposes with the remaining $2.8 billion or 69.4% of lending for owner occupation purposes. Of the 84.1 percent of new lending for established housing, $10.7 billion or 50.5 percent was borrowing by owner occupiers with the remaining $10.5 billion or 49.5% borrowed for investment purposes.

The data shows that much more lending is for established housing which makes sense when you consider the flow of new housing, despite being at record highs, is only a fraction of the total housing stock.

Despite low interest rates that are anticipated to go lower over the coming months it is difficult to imagine how growth in housing finance commitments will experience a significant uplift. Investor demand may pick up a little but historically weak rental growth and record low rental yields along with a surge in new investment housing stock should limit any uplift.

This should also contribute to a slowing in value growth in Sydney and Melbourne and although other areas may see a pick-up in mortgage demand, much lower home values in those regions will likely limit any significant pick-up in housing finance commitments.