Investors and owner occupiers keeping first home buyers out of market: CoreLogic RP Data's Cameron Kusher

Entering the property market is a tough gig for first home buyers, especially when faced with competition from buyers who hold larger buying budgets, some of which has been accrued from property equity earned as a result of recent strong capital gains.

While home value rises have been moderate over recent years outside of Sydney and Melbourne, it provides little comfort for first home buyers in the two largest cities who struggle to compete with those that already own homes.

In 2008, combined capital city home values fell by -6.1 percent in the space of 9 months. By the end of the year, home values had reached and began to climb further thereafter.

The growth drivers largely came from two forms of stimulus: aggressive interest rate cuts and a boost to the First Home Owners Grant (FHOG). Since the removal of the FHOG boost and scaling back and complete removal of others, first home buyers have continued to languish at near record-low levels.

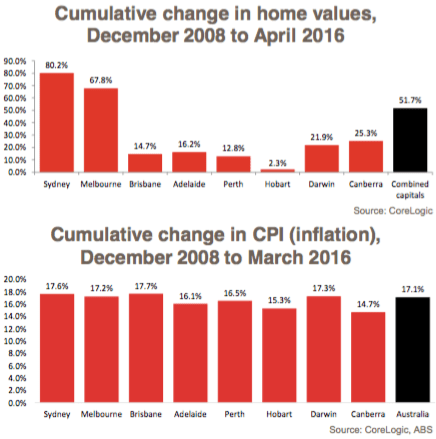

The increase in home values across each capital city from December 2008 to April 2016 can be seen in the first of the adjacent charts. Another way to think about this is that if in December 2008 you owned a home worth $500,000 it is now worth $758,418 which is $258,418 more than in December 2008. Looking at this same calculation across each capital city, the increases in value over that time based on a $500,000 home owned in December 2008 are: Sydney ($400,825), Melbourne ($338,866), Brisbane ($73,417), Adelaide ($81,029), Perth ($64,096), Hobart ($11,263), Darwin ($109,293) and Canberra ($126,262).

The data clearly shows that the value property for home owners has undergone some massive rises, the increase in inflation and wages has been comparatively more sedate.

Although combined capital city home values have increased by 51.7 percent between December 2008 and April 2016, inflation has increased by a significantly lower 17.1 percent over the period. CPI has increased by a greater amount than values in Brisbane, Adelaide, Perth and Hobart indicating ‘real’ home values have fallen. Meanwhile in Sydney, Melbourne, Darwin and Canberra CPI growth has lagged that of home value growth.

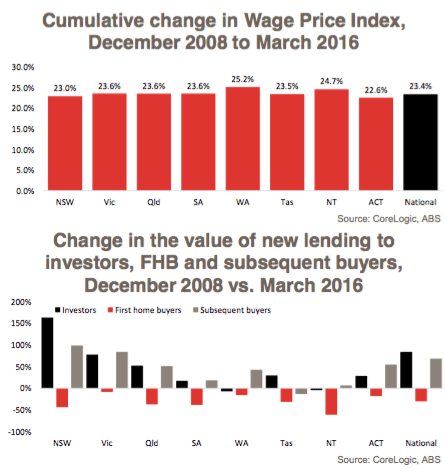

Looking at wages growth between December 2008 and March 2016, the data shows that nationally, and in New South Wales, Victoria and the ACT, it has lagged value growth across the capital cities; wages are now growing at their slowest pace in at least 18 years.

While the increases highlighted include strong wage increases in the latter part of the mining boom, nonetheless, it shows that in NSW and Vic wages are increasing at a much slower pace than home values in Sydney and Melbourne are.

The last chart shows the change in the value of new lending (excluding refinances) to investors, owner occupier first home buyers and subsequent buyers between December 2008 and March 2016, and highlights how the value of lending to owner occupier first home buyers is now lower than it was in December 2008 across each state and territory.

This has occurred despite the increase in home values over the timeframe.

While lending to owner occupier first home buyers has fallen, lending to investors and subsequent buyers has increased in most states and territories with substantial rises in NSW and Vic.

Outside of Sydney and Melbourne home values have increased below or at a similar pace to inflation and wages, however, it is a very different story in the two largest capital cities where existing Sydney and Melbourne home owners have seen significant increases in the ‘real’ value of their home.

Those that do not yet own a property will struggle to compete with investors and upgraders who have been active in the market and where significant equity has been acquired.

The simple answer for first home buyers, particularly in Sydney and Melbourne, is to look to buy properties outside of these cities however, that may seem a little simplistic given jobs creation has not been as strong outside of Sydney and Melbourne and for many moving interstate, employment opportunities are generally a big decision.

Even buying outside of Sydney in nearby regional cities may not be attractive because transport infrastructure does not provide quick and efficient access to Sydney and Melbourne from nearby regional cities.

Whatever the outcome, we certainly don’t advocate for the return of grants for first home buyers as they have tended to just push up the cost of housing.

Cameron Kusher is research analyst for CoreLogic RP Data. You can contact him here.