East Coast industrial vacancies rise for the first time in a year: Knight Frank

East Coast industrial vacancies have risen for the first time in a year, driven by a 6.2 percent increase in Melbourne, although Sydney and Brisbane recorded small declines over the quarter, according to the latest Industrial Vacancy Analysis research report by Knight Frank.

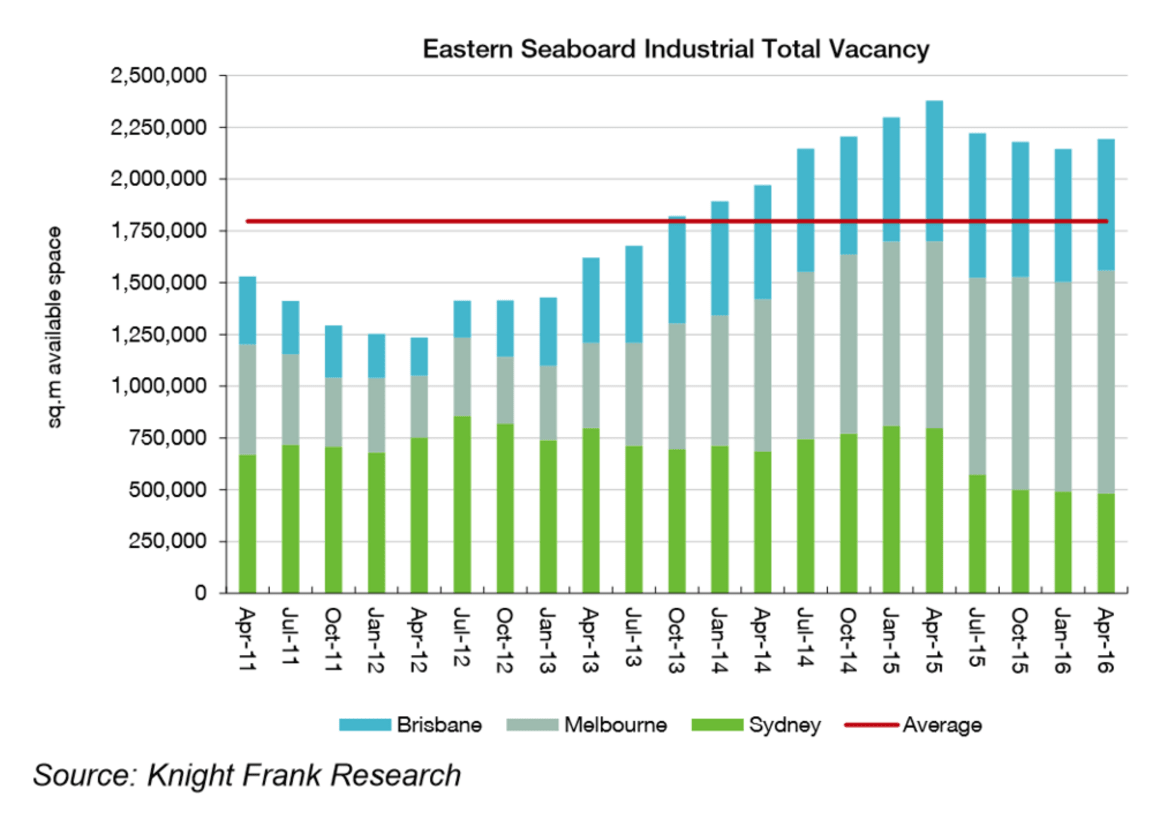

The total industrial vacancy on the East Coast currently sits at 2.19 million square metres, with a 2.3 per cent increase recorded over the past quarter. However, total vacancy fell by 8.3 percent over the past year, with Sydney driving this result, down a staggering 39 per cent over the year to April 2016.

Sydney was the standout market over the past year, recording a two per cent fall in vacancy over the past quarter to 482,820 square metres, said Knight Frank’s Group director of Research & Consulting, Matt Whitby.

Over the past year, however, vacancies have fallen from a peak of 807,485 square metres in January 2015.

“Sydney has seen a steady upward trend in leasing deal volumes, resulting in above-average stock take up for the past nine consecutive quarters. This is a result of a number of factors, including increased economic activity, particularly in the household goods and construction sectors, and high demand in the Sydney area due to the development of key infrastructure projects. However it is also due to large institutional owners moving tenants among portfolio assets,” he said.

Brisbane recorded a fall in vacancy for the third consecutive quarter, down by nine per cent since the recent peak in mid-2015, taking the total to 636,288 square metres. “Despite the recent improvement, the vacancy remains 51 per cent above the long-term average and tenant demand is still patchy. However, the vacancy level within existing assets should continue to decrease with tenants having the opportunity to upgrade their accommodation at lease end on competitive terms.”

“The Melbourne market continued its recent steady growth in vacancies, with a 6.2 per cent increase recorded over the past quarter to over a million square metres now available (1,074,788 square metres). This increase was dominated by prime stock (up 16 per cent), as secondary vacancy actually fell by two per cent over the quarter,” Whitby said.

According to Whitby, although the level of vacant industrial space across the Australian East Coast market rose modestly over the past quarter, both prime and secondary vacancy fell over the past year, down by seven percent and nine percent respectively.

“Despite prime stock being highly in demand by industrial occupiers, given it is new and able to be tailored to individual businesses’ needs, the proportion of prime stock available now outweighs secondary stock across the East Coast.

“The key factors are due to current market conditions – cost-conscious occupiers are looking towards secondary stock. In addition, the emergence of new stock on the market has driven up availability.”

According to Whitby, “As at April 2016, the proportion of total vacancies made up of prime stock is now 53 per cent of East Coast industrial vacancies, up from 45 percent two years ago, and 37 percent three years ago.”

Whitby said that the preference in the market for prime space is clear to see, with 59 percent of take-up recorded being within prime accommodation over the 12 months to April 2016. The greatest bias to prime absorption was seen within the Sydney and Brisbane markets where 71 percent and 60 percent respectively of the annual take-up was prime space. In Melbourne, prime space accounted for only 48 per cent of take-up over the 12 months to April 2016.

Knight Frank’s head of Industrial, Greg Russell, said that following a softer pipeline of speculative stock over the past year, the April quarter saw the level of speculative stock available increase by 12 percent across the Australian East Coast market.

“The interesting statistic this quarter, is that the level of speculative stock under construction has jumped 17 percent over the past quarter and more than doubled over the past year, from 53,500 square metres to 108,000 square metres currently, however, the speculative space completed but remaining vacant fell 31 per cent over the past year to 113,719 square metres.”

“This has been predominantly driven by an increase in take-up for completed speculative product, coupled with new speculative commencements, as confidence returns in the markets, particularly in Sydney.

“The major institutional developers still have a healthy pipeline for further speculative development, and it will only take a few commitments to really see the speculative construction levels spike later this year and into 2017.”

Russell added that while the level of larger vacant options has been increasing in Melbourne, they have fallen in Sydney and Brisbane. The general trend towards upgrading accommodation by tenants means that prime, larger options will continue to attract solid demand and hence take-up. In Sydney, there are only eight prime opportunities above 10,000 square metres (down from 15 a year ago), while 23 over 10,000 square metres exist in Melbourne (up from 14 options a year ago), and there are 11 prime vacancies above 8,000 square metres in Brisbane (compared to 11 a year ago).

Brisbane

In Brisbane’s industrial sector (3,000 sqm+), total vacant space during the first quarter of 2016 fell by slightly to 636,288 square metres, but was down 6.4 per cent from a year ago (680,151 square metres).

Knight Frank’s joint head of Industrial Queensland, Mark Clifford and Chris Wright said, “The pre-lease market has been quite active and has contributed to the slow reduction in the vacancy levels. A flight to quality is evident and will continue whilst aggressive leasing deals are on offer.

“Pre-committed new construction is expected to provide further backfill vacant space over the course of 2016 with Beaumont Tiles, Couriers Please, Lindsay Bros Transport and OI all expected to make significant relocations during the year.

“We believe a series of imminent commitments will provide a solid boost to the leasing market. Tenants 6,000 square metres plus with a sufficient lead time will continue to be attracted to new construction as the low yield environment for long WALE assets supports construction at relatively lower rental levels."

Sydney

In Sydney’s industrial sector (5,000 sqm+), solid leasing activity has underpinned a decline in total vacant space, reducing 1.9 per cent during the first quarter of 2016 to 482,820 sqm.

Tim Armstrong, head of Industrial, NSW said, “Sydney’s industrial vacancies are now at a series low, which was the result of above average gross take up which measured 190,337m² over the past quarter, 35 per cent above the series average.

“Recent leasing demand has been primarily driven by 3PL groups as businesses continue to outsource logistic functions; however, there have been increased enquiry levels from pharmaceutical/medical operators in recent months.”

In terms of location, the Outer West continues to underpin leasing demand, accounting for 44 per cent of gross take-up over the first quarter of 2016 as four 10,000 sqm+ options were leased. However, a number of large backfill leasing options are starting to come back onto the market including the DHL backfill space at 227 Walters Road, Arndell Park which will partly offset above average leasing demand.

“While a number of speculative developments have been added to vacant stock levels over the past quarter, the reality is they aren’t remaining vacant for too long. In the first quarter of 2016, 25,442 sqm of under construction speculative stock was leased, highlighting the drive for operational efficiencies and demand for modern stock. Currently, unleased speculative stock measures 59,602 sqm, all of which is under construction with no vacant completed speculative stock available," said Armstrong.

“The generally positive outlook for the NSW economy is expected to see a continuation of solid leasing activity, particularly as there are a number of large briefs in the market which should crystallise into gross absorption throughout 2016,” said Armstrong.

Knight Frank’s senior director, head of Industrial Victoria, Gab Pascuzzi, said the impact of the upcoming closure of the automotive manufacturing and supply industry will start to come into fruition at the end of 2016. “To date this has had minimal impact on the industrial market, however we anticipate this will put increased pressure on vacancy rates across traditional industrial locations in 2017; predominantly across lower-grade secondary stock.

“Over the past 12 months, we have seen an increase in pre-commitment activity across Melbourne. Given the shortage of prime existing options in the market combined with increased tenant demand, we anticipate prime backfill space from the likes of Target and The Reject shop coming to the market later this year will be will be absorbed quickly.”

According to Pascuzzi, “The south-east region recorded the highest level of leasing activity since Q1 2010, totalling 70,995 square metres. However, we are seeing pressure in the market with a lack of large existing options notably in the West, with just two vacant stock options above 20,000 square metres.”

Perth

In Perth’s industrial sector (2,000sqm+), vacant industrial space in Perth increased by 16 per cent over the past quarter to 647,746 square metres, a series high.

Knight Frank’s senior director, head of Industrial WA, Jarrad Grierson, said Perth’s industrial market continued to be affected by the slowdown in the resources sector and relatively low market confidence with escalating levels of vacant space in the market.

“The Perth industrial market has a high correlation with the resources sector where companies are currently sitting idle or downsizing, triggering downward pressure on rental rates. Some businesses are taking advantage of the softer market conditions and looking to upgrade into better quality accommodation in a better location.

“Vacancy in secondary-grade buildings increased by 22 per cent over the past quarter and almost doubled over the past year and now accounts for 76 per cent of total stock. This is in stark contrast to the prime market, where vacancy was unchanged over the past quarter and actually fell by 24 per cent over the year.

“There continues to be a demand for sublease space in the market as these properties offer competitive rents and incentives in order to replace tenants. Activity in the market is also evident from pre-leasing activity that has occurred in the last 12-24 months.

“The market had 200,000 square metres of newly developed pre-lease space come on line, including a 42,000 square metres warehouse pre-leased to K-Mart in Jandakot in February. Moving forward this will continue to impact the level of backfill space once occupiers relocate into new industrial space,” concluded Grierson.