Mortgage demand shrinks in January, will it continue throughout 2016? Cameron Kusher

Housing finance data for January 2016 shows that the value of housing finance commitments was recorded at $31.9 billion over the month.

Based on this figure, mortgage lending fell by -3.4 percent over the month. Even though the data is seasonally adjusted, we often see falls in mortgage lending over January so perhaps we need not read too much into the fall, however, this is the largest January fall in lending since 2011.

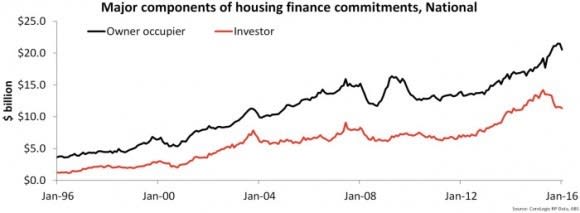

Looking at the two major components of mortgage lending: owner occupier and investors both have recorded a fall over the month. In January there was $20.5 billion worth of finance commitments to owner occupiers and $11.4 billion in commitments to investors. The value of owner occupier commitments fell by -4.3 percent over the month but was 15.9 percent higher year-on-year.

Investor commitments fell by -1.6 percent in January and were -14.8 percent lower year-on-year. With investor demand having slowed over recent months, they now account for 35.6 percent of all mortgage commitments which is virtually right on its decade average after peaking at 43.3 percent of all housing finance commitments in May of last year.

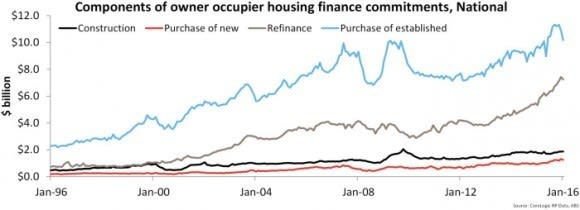

Of the $20.5 billion in commitments to owner occupiers in January, $1.9 billion was for construction of dwellings, $1.2 billion was for purchase of new dwellings, $7.2 billion was for refinancing of established dwellings and $10.2 billion was for the purchase of other established dwellings. Construction of dwellings was the only segment of lending to rise over the month (+0.7 percent) with falls in value of lending for purchase of new dwellings (-5.2 percent), refinancing established dwellings (-2.3 percent) and purchase of other established dwellings (-6.4 percent).

Despite monthly falls, year-on-year all segments have seen an increase in lending with construction of new dwellings rising 6.1 percent, purchase of new dwellings up 35.6 percent, refinances up 36.0 percent and purchase of other established dwellings having increased by 4.8 percent. Although lending is up over the past year, there is a clear downwards trend in owner occupier lending, particularly for established dwellings, over recent months. It will important to monitor whether this trend persists in coming months as it could point to slowing value growth.

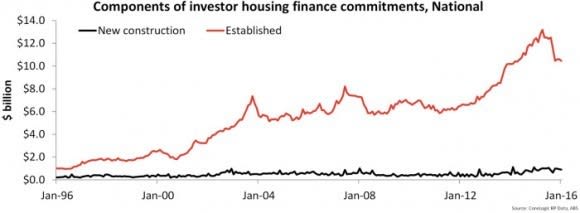

Following intervention in the market by the regulator, we have seen a sharp slowdown in lending to the investment segment over the past 8 months. As earlier mentioned, investors accounted for 43.3% of all housing finance commitments in May of last year with their proportion falling to 35.6% in January 2016. Looking at the two components, in January 2016 there were $899 million worth of commitments for new construction and $10.5 billion worth of commitments for established housing stock.

Over the month, the value of commitments fell by -4.2% for new construction and by -1.4% for established housing stock. Year-on-year the value of lending is 3.2% higher for new construction but -16.0% lower for established stock. Much like the owner occupier chart, it shows that demand for established stock has eased and is trending lower, albeit at a slower pace. In fact, the value of commitments for established investment stock is at its lowest level since April 2014.

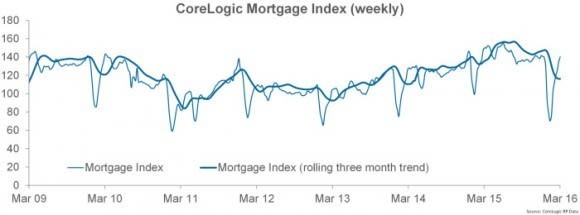

The CoreLogic Mortgage Index which is published weekly and tracks mortgage activity across our proprietary platforms indicates that January was a weak month for housing finance commitments. We would expect that housing finance commitments will rise in February and so far March also points to increasing demand. However, mortgage demand remains lower than it was at the end of last year and lower than it was a year ago. While housing finance commitments should increase from their January levels it is unlikely that demand will start to grow as strongly as it was in the early part of last year or late in 2015.

The constraints on investment lending have been extremely effective and have resulted in a swift and significant pull-back in demand, in fact the value of investment housing finance commitments in January was -20.0% lower than its April 2015 peak. Although the CoreLogic Mortgage Index points to a rebound in demand over the coming months, we expect that growth in housing finance commitments will remain more subdued than what we saw over recent years.

Of course, the direction of housing finance will ultimately be determined by housing demand. After demand weakened over the second half of 2015 we have seen stronger demand early in 2016 with much stronger auction clearance rates falling property listings in a number of cities and a rise in property transactions.

Cameron Kusher is research analyst for CoreLogic RP Data. You can contact him here.