Owner occupier housing finance commitments take a step up: Cameron Kusher

The Australian Bureau of Statistics (ABS) released housing finance data for August 2015 earlier this week.

The data broadly showed a further pick-up in owner occupier lending and a slowing in investor lending. It is important to reconcile this against numerous reports that many mortgagees have been quick to advise their lenders that their properties which were formerly investment properties are now in fact owner occupied.

This is due to the fact that most lenders are now charging a premium for investment mortgages.

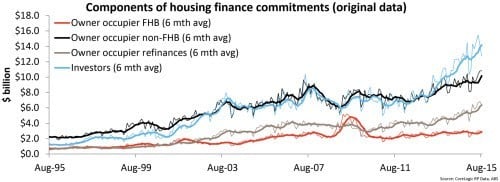

The above chart details the components of those borrowing over time. What’s immediately noticeable is that while there has been a recent surge in lending to investors, over recent months there has been a clear fall in lending to this cohort.

While investment lending is slowing, owner occupier lending is rising however, there has been very little bounce in lending to first home buyers. For the most part the rise in owner occupier lending is being fuelled by an escalation in both refinances and borrowing for new loans to non-first home buyers. Again, it is important to note some of these figure may be being affected by re-classifications of mortgages.

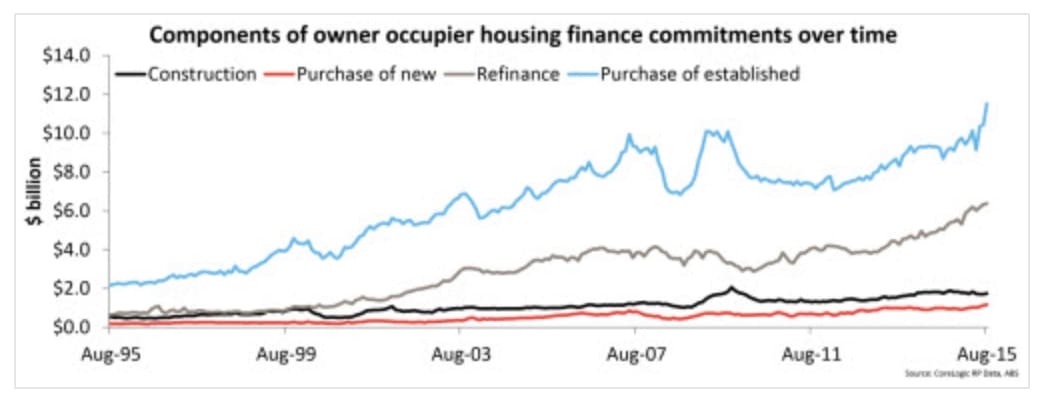

In August 2015, owner occupiers committed to $20.8 billion worth of housing finance, a 6.1% rise over the month and a 26.5% year-on-year rise. Looking at the components of owner occupier lending there was $1.7 billion in lending for construction of dwellings, $1.2 billion in lending for purchase of new dwellings, $6.4 billion in refinances of established dwellings and $11.5 billion for purchase of other established dwellings.

The 6.1% monthly rise in owner occupier lending was largely fuelled by a 10.4% rise in lending for purchase of established dwellings however, each component rose. Refinances have typically been the greatest source of growth in owner occupier lending however, they recorded the slowest growth of any segment over the month. Looking at year-on-year changes, lending for construction of dwellings rose 0.5%, lending for purchase of new dwellings rose 17.6%, refinances of established dwellings rose 26.7% and purchase of established dwellings increased by 32.6%.

Over the coming months we will be watching closely to see whether the growth in owner occupier lending can be maintained, particularly in the face of falling population growth and no real increase in activity from first home buyers.

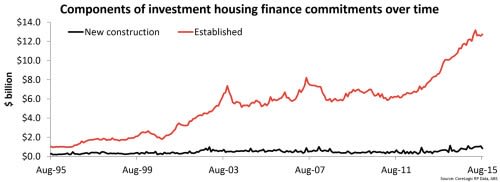

Switching the focus to the investor segment, there was $13.6 billion worth of commitments to investors in August 2015. The value of lending to investors was -0.4% lower over the month but 12.0% higher year-on-year. It was also the first time in 13 months that the value of new lending (excluding refinances) was greater to owner occupiers than it was to investors.

Over the month there was $0.8 billion in lending for construction of dwellings and $12.7 billion in lending for established housing. Over the month, lending for construction of dwellings fell -22.0% while commitments for established housing rose 1.4%. Year-on-year lending for construction of new homes is -2.5% lower and lending for established homes is 13.1% higher.

The data appears to indicate that there is a change occurring in the mortgage lending market. Whereas investors and owner occupier refinances have been the primary drivers of growth lately, it seems as if this is now tilting to owner occupier new loans starting to dominate. Given that investment mortgages generally now have a higher interest rate than owner occupier mortgages, it may be playing a role in the tilt towards owner occupier lending.

Furthermore, value growth has been strong for more than three years in Sydney and Melbourne and investors may be becoming concerned about the longevity of the boom while growth outside of these cities has been sedate.

Once you also consider a record high pipeline of residential construction accompanied by a record low rate of rental growth and historical low yields perhaps a growing number of investors are looking towards other forms of investment they perceive as less risky at this stage in cycle. It’s still early days for the slowdown in investment lending but we, along with the RBA and APRA, will be watching closely to see whether the slowing in investment lending and the rise in owner occupier lending persists over the coming months.

It is also going to be interesting to see what impact this has on overall demand for housing over the coming months in lights of evidence of a bit of a softening in the Sydney housing market.

Cameron Kusher is research analyst for CoreLogic RP Data. You can contact him here.