Housing finance commitments rise in July: Cameron Kusher

The Australian Bureau of Statistics (ABS) released housing finance data for July 2015 earlier this week.

Throughout July, there was $32.8 billion worth of housing finance commitments. This figure was comprised of $19.2 billion worth of commitments to owner occupiers and $13.6 billion in commitments to investors. Over the month, the total value of housing finance commitments increased by 1.5% to be 15.0% higher year-on-year.

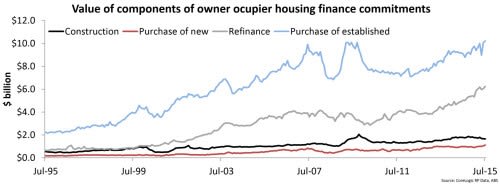

At $19.2 billion, owner occupier housing finance commitments increased by 2.2% over the month and were 13.9% higher year-on-year. Breaking the $19.2 billion into its components: $1.6 billion was for construction of dwellings, $1.1 billion was for the purchase of new dwellings, $6.2 billion was for refinances of established dwellings and $10.2 billion was for the purchase of established dwellings. Over the month, commitments for the construction of dwellings fell -1.5%, purchase of new dwellings rose 8.4%, refinances rose 3.3% and purchase of established dwellings rose 1.5%.

Over the past 12 months the refinance segment has been the key driver of growth in the owner occupier lending segment with commitments up 23.7%. In comparison, year-on-year changes have been recorded at -7.6% for construction of dwellings, 15.4% for purchase of new dwellings and 12.6% for purchase of established dwellings. Recently growth in the owner occupier lending segment has been lacklustre, driven largely by refinances however, the 13.9% year-on-year rise in owner occupier housing finance commitments excluding refinances is the largest rise since February 2014.

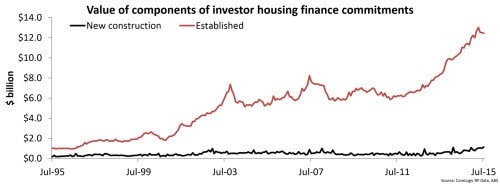

Turning to the investment segment of housing finance commitments, this has over recent years been a significant driver of new demand. In July 2015, investor housing finance commitments rose by 0.5% to be 16.5% higher year-on-year. If we look at the $13.6 billion in investment housing commitments across its components, $1.1 billion was for construction of new investment dwellings and $12.5 billion was for established homes.

Over the month, commitments for new construction rose 11.7% compared to a -0.4% fall in commitments for established homes. Year-on-year investor commitments for construction of new dwellings has increased by 81.5% compared to a 12.9% rise in the much larger segment for purchase of established investment homes. The chart above shows the recent weakness in commitments for established homes and the ongoing rise in commitments for new construction.

It seems that there is a growing appetite for investment in off-the plan investment properties while demand for established investment stock is waning a little. Despite the monthly rise in demand for investment lending, the rate of growth has started to ease as Australian authorised deposit-taking institutions (ADIs) tweak their lending policies in line with policy updates from APRA aimed at slowing growth in the pace of total investor housing credit.

Housing credit data for July 2015 showed that growth in owner occupier credit is ramping up while investor credit demand is potentially slowing. This release of housing finance data appears to support that notion. The ADIs will be hoping that they can entice additional activity from the owner occupier segment over the coming months as there is likely to be a slowdown in lending to the investment segment.

Housing finance data is continuing to rise however, it appears that growth is starting to tilt away from investors towards the owner occupier segment. Although regulators such as the Reserve Bank and APRA will be glad to see that exuberance from investment borrowers may be slowing, they will be very keen to monitor and ensure that any pick-up from owner occupier borrowers is not as a result of a relaxing of lending standards.

Both the housing credit and housing finance data will be closely monitored over the coming months in order to see if this transition continues. Specifically we will be watching whether housing credit can continue to increase its rate of growth and if new commitments continue to tilt away from investors towards owner occupiers and what impact that may have on housing finance demand.

Cameron Kusher is research analyst for CoreLogic RP Data. You can contact him here.