Coronavirus to slow Australian GDP significantly: NAB's Alan Oster

EXPERT OBSERVATION

Headline GDP rose by 0.5 per cent in Q4 to be 2.2 per cent higher over the year, a moderate result ahead of an expected virus-driven fall in output in Q1.

Notwithstanding a significant contribution from the recovery in housing turnover and small improvement in consumer spending, private domestic demand remains weak with falling residential construction and business investment subtracting 0.3ppt from growth. Net exports and stocks helped offset this weakness.

While the focus of policy-makers has turned to the impact of the coronavirus on both the global and domestic economies, today’s outcome confirms a below trend pace of growth as a starting point even with the strong recovery in housing turnover, with a turnaround unlikely for some time given residential investment has yet to trough, consumer spending is constrained by weak wage growth and businesses outside of mining remain reluctant to invest.

Factoring in an initial hit from the virus outbreak, this leads us to forecast growth to remain below trend over the next year or so, before seeing a small improvement. There is significant uncertainty about the extent and duration of the shock from the outbreak, but this outlook points to rising unemployment over 2020 and likely further action from the RBA beyond our expected rate cut in April.

We will update our forecasts for growth, the labour market and the policy outlook next week.

In Q4, weak private demand growth was driven by a fall in dwelling investment which is now down 9.7 per cent over the year, and a decline business investment. While consumption growth improved, it also continues to track well below its long- run average, reinforcing our long-held view that tax rebates have failed to provide a significant boost to household spending.

Indeed, part of the increase in consumption reflects extreme price discounting. Public-sector spending made no contribution following the solid outcome in Q3. Offsetting some of this weakness was a 0.1 contribution from exports - though this is a little weaker than recent quarters. A significant (though likely) temporary boost to the expenditure side came from the recovery in housing turnover which saw a boost to real estate margins.

Both the production and income measures of GDP were slightly stronger than the expenditure measure in the quarter.

Looking forward, the magnitude of the bushfires and especially the coronavirus impact on the March quarter will be a focus, as will the ongoing impacts of the latter in subsequent quarters. For now, we have factored in a decline in March quarter GDP, but for a small recovery in quarterly growth thereafter on the assumption that the virus is quickly contained.

As a result, we see year-average growth of 1.2 per cent in 2020 before an improvement in 2021 to around 2.7 per cent. Should the impact of the virus become more protracted this will necessarily see a down grade to our forecasts for growth.

Notwithstanding the impact of the virus, our read is that the sluggish pace of underlying growth already warrants further policy action, with below-trend growth over the next 18 months likely to see a deterioration in the labour market with further downside risk as a result of ongoing impacts from the coronavirus.

Indeed, we see the RBA cutting rates for a second time in 2020 at the April meeting and a significant risk of unconventional policy going forward depending on the severity of the uptick in the unemployment rate as well as the magnitude and impact of any response from fiscal policy.

Household consumption growth improved slightly in Q4, rising 0.4 per cent q/q but remains weak at 1.2 per cent y/y – the weakest pace since the GFC. The drivers of consumption growth in the quarter were increases in discretionary categories including clothing & footwear, household goods and recreation and culture – possibly reflecting some impact from the earlier tax cuts.

Nonetheless, spending on discretionary items has remained weak over the year, with spending on essentials having driven the bulk of consumption growth.

Underlying business investment declined by -0.8 per cent q/q, similar to Q3 (-1.1 per cent q/q). Unlike Q3, however, weakness in business investment was driven by non-mining investment which fell 3.6 per cent, while mining investment increased by 5.0 per cent q/q.

Mining investment in Q4 was 3.2 per cent higher than the same time a year ago – the first time annual growth has been positive since 2013 other than one-off gain posted in Q3 2017. The turnaround in mining was not unexpected, but the decline in commodity prices that started towards the end of last year, now reinforced by the coronavirus shock to the world economy, casts doubt on whether this will be sustained. At the same time, weak business conditions remain a headwind for non-mining sector investment.

Dwelling investment fell 3.4 per cent in the quarter driven by a fall in investment in construction (-4.1 per cent) and a fall in alterations & additions (-2.2 per cent). Over the year dwelling investment has fallen 9.7 per cent. This result is unsurprising given the weakness in work done, and the ongoing weakness in dwelling approvals. These data also confirm the downturn in construction is not over. The decline was driven by a fall in NSW and QLD, though construction also declined in WA and Tas. Vic saw a small improvement in the quarter.

Government demand growth slowed considerably from Q3. Underlying public demand grew by 0.1 per cent q/q, well down from 2.0 per cent in Q3. However, growth over the last year was a still solid 5.1 per cent y/y. Government consumption growth was 0.7 per cent q/q – the lowest growth since Q2 2018 due to a fall in defence spending (a volatile component) and another quarter of very modest state/local government consumption growth. In contrast, Federal non-defence spending grew by 2.4 per cent q/q (10 per cent y/y), likely reflecting disability and aged care spending.

Net exports made a 0.1ppts contribution to quarterly GDP growth even with export volumes basically unchanged in the quarter, as imports declined (-0.5 per cent q/q). Exports and imports of non-monetary gold declined substantially masking growth, overall, in other trade flows.

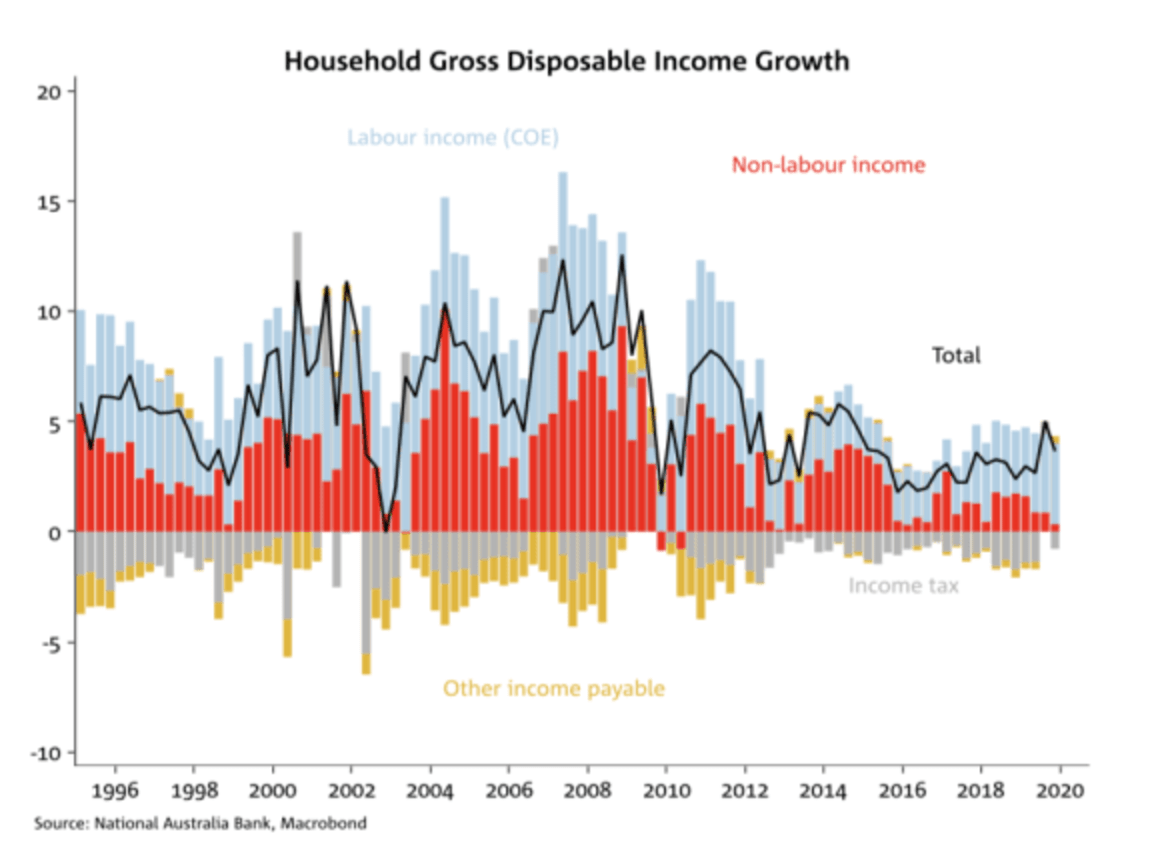

Compensation of employees rose by 1.0 per cent in the quarter (5.1 per cent y/y). While employment continued to rise, average COE per employee also increased by a moderate 0.5 per cent in the quarter. COE per hour continued to track above the WPI but saw a moderation in year-ended growth in the quarter. The boost to household income growth from tax cuts in Q3 faded in the quarter which also saw the household savings rate tick down.

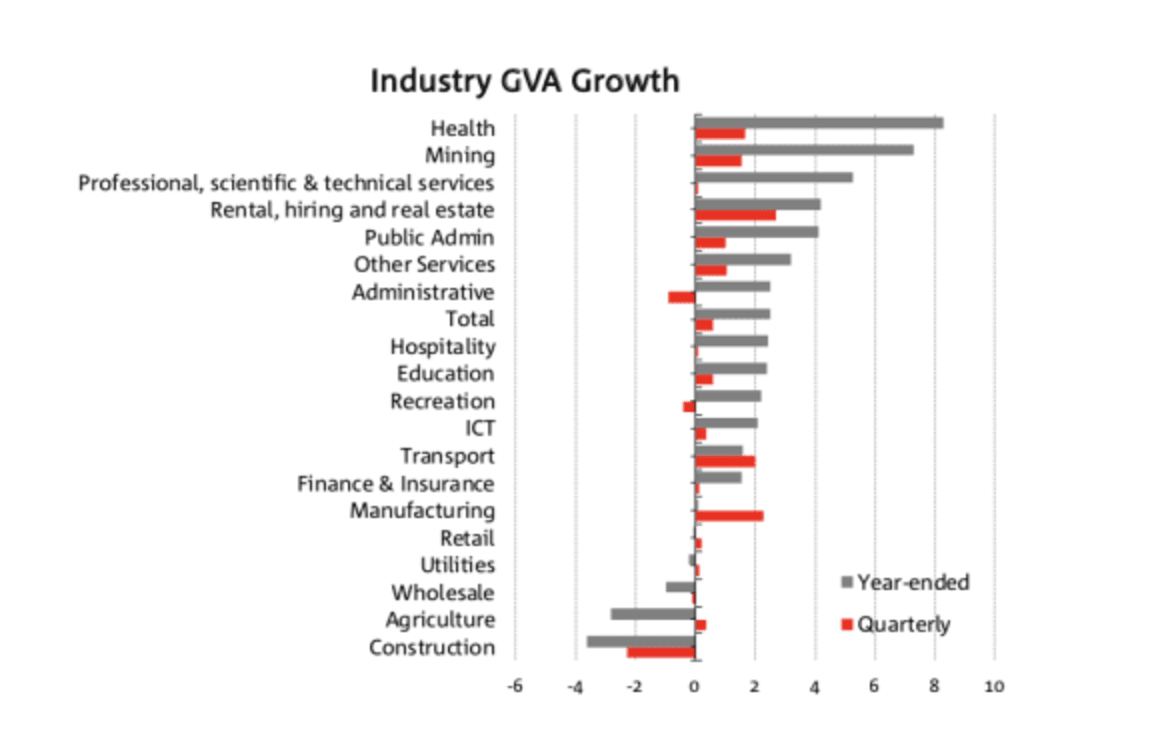

By industry, real estate services saw the strongest quarterly growth (up 2.7 per cent on a quarterly basis), likely reflecting the improvement in housing sales. Manufacturing (notably in food products), transport, healthcare and social assistance and mining also grew strongly, as did mining. Construction contracted 2.3 per cent on a quarterly basis, with building construction, engineering and construction services all hit down. Mining, manufacturing, transport, real estate services, public administration and health care each contributed 0.1 per cent to GDP growth in the December quarter, while construction detracted 0.2 per cent from growth.

By state, the ACT experienced the fastest growth in state final demand (+0.8 per cent q/q), followed by NSW (+0.5 per cent), with the latter result largely reflecting growth in public consumption and investment spending. NT SFD rose by 0.3 per cent, its first increase since Q3 2017, reflecting a big boost in public investment and to a lesser extent petroleum exploration (perhaps driven by the end of the NT’s fracking ban). Queensland recorded growth of 0.2 per cent q/q, while Victoria saw a fall of 0.1 per cent, largely reflecting a slowdown in major road construction. SA and WA both contracted 0.2 per cent, driven by falls in private and public investment. Tasmania fell 1.0 per cent on lower public and private investment; non-dwelling construction fell 18.6 per cent on reduced energy and accommodation project spending.

The slide in farm GDP was arrested in Q4 on a quarterly basis, up 0.4 per cent, although it remains lower on an annual basis (down 3.0 per cent). While the drought continued to wreak havoc in New South and Queensland in Q4, this led to higher cattle and sheep slaughter and therefore higher meat production. 2020 has brought a deluge to many Australian agricultural regions, which is very welcome relief indeed. However, this may be slow to show up in 2020 GDP as graziers rebuild herds and flocks – reducing meat production. It remains too early to say how the 2020-21 winter cropping season will perform.

Alan Oster is the Chief Economist at NAB Group