Economic growth likely to remain below current RBA forecast: Bill Evans

EXPERT OBSERVATION

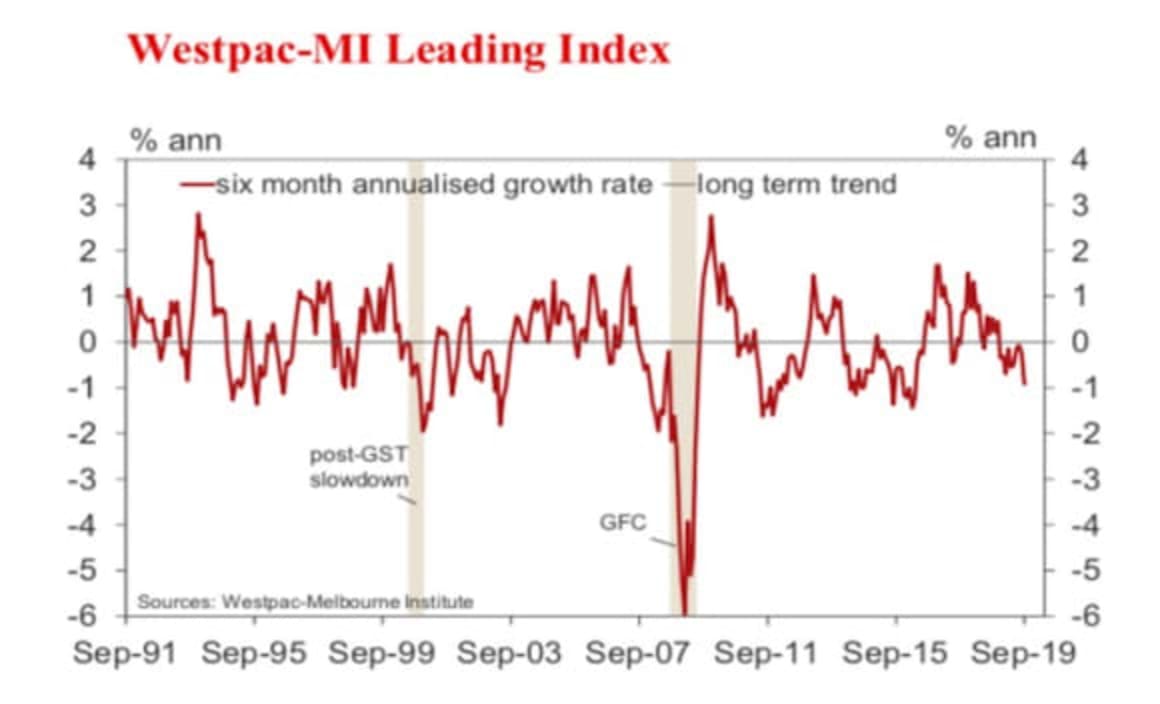

The growth rate is now materially below trend and is signalling that growth through the first half of 2020 is likely to remain below trend.

That profile is broadly consistent with Westpac’s forecasts which have growth in the first half of 2020 at an annualised pace of 2.4% consistent with the overall growth pace in 2020 of 2.4%.

This forecast contrasts with the Reserve Bank’s current forecast of 2.8% although that forecast may be revised when the Bank releases its new forecasts on November 8.

Click here to enlarge:

The Leading Index growth rate has deteriorated over the last six months from –0.56% in April to –0.92% in September.

The main components driving the 0.36ppt shift have been a further weakening in dwelling approvals (–0.25ppts); a deterioration in consumer sentiment (–0.21ppts); a sell-off in commodity prices (–0.20ppts); and slower growth in monthly hours worked (–0.11ppts).

These negatives have been partially offset by a reduced drag from the yield spread as the RBA’s rate cuts have lowered short term interest rates (+0.24ppts), and a slight improvement in US industrial production (+0.23ppts).

The Reserve Bank Board next meets on November 5. Westpac expects the Board to hold the cash rate steady at that meeting.

On October 15 the Bank released the minutes of the October Board meeting. The minutes contained a detailed justification for the decision to ease the cash rate from 1% to 0.75% at that meeting.

In particular it emphasised the benefits to the economy of a lower currency and improved cash flow for households, while recognising some potential negative impact on confidence of ultra-low rates.

That issue was subsequently highlighted by the 5.5% fall in the Westpac MI Consumer Sentiment Index in response to the October rate cut.

It seems clear that the Board expects to ease rates further although we believe the November meeting will be a little too soon. Westpac continues to expect that the next rate cut will come in February next year.

Read full report 'Westpac-MI Leading Index September' (PDF 116kb)

BILL EVANS is Chief Economist for Westpac