Fed eases again - but they are still just insurance cuts: Shane Oliver

EXPERT OBSERVER

As widely expected the Fed cut the Fed’s rate by another 0.25% taking it to a range of 1.75-2%, for the second cut this year.

While the Fed remains optimistic on the outlook for the US economy and made no significant changes to its economic forecasts, as with the July cut its basically taking out insurance given ongoing threats to the US outlook from the trade war and slower global growth at the same time that inflation is still running just below target.

The current easing cycle remains a bit like the Fed easings of 1987 after the share market crash and in 1998 after the LTCM hedge fund crisis – that saw the Fed cut despite solid growth in order take out insurance in case there was a negative flow on to the economy.

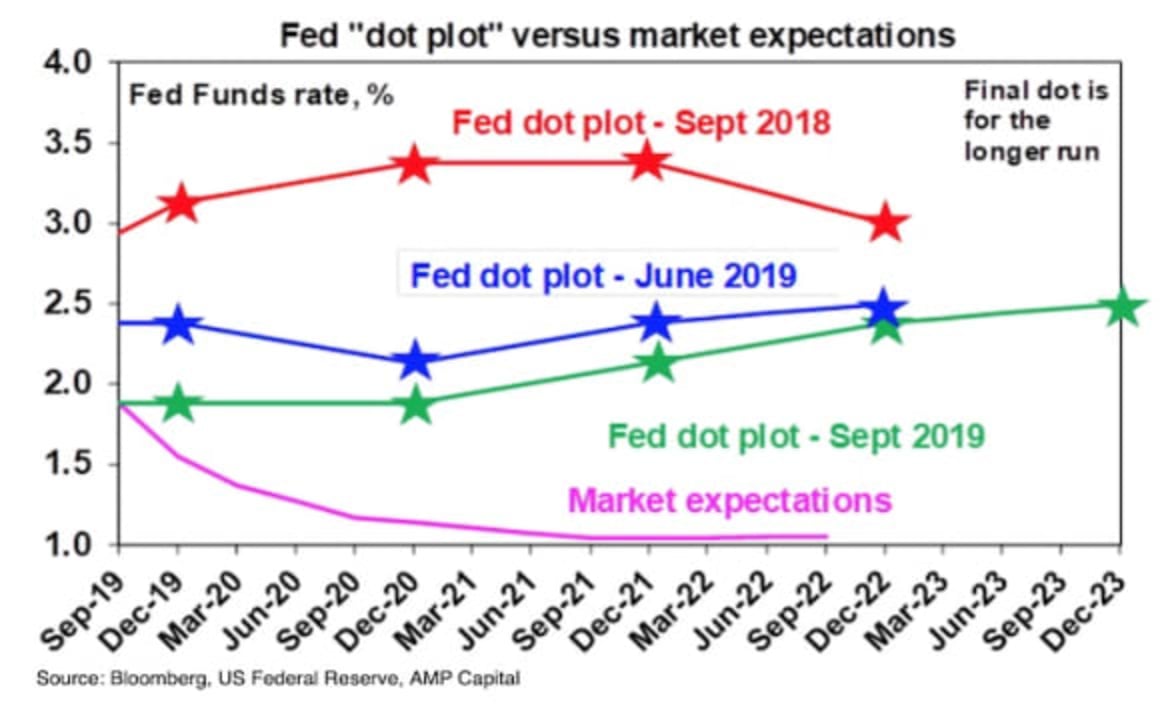

The Fed was a bit less dovish than expected and this was highlighted by the so-called “dot plot” of Fed officials interest rate expectations not falling as much as expected relative to the June “dot plot” and the median dot showing no more rate cuts. Specifically seven officials see another cut by December, five are on hold and five see a hike.

However, it’s likely that the seven who see a cut include the Fed leadership of Powell, Clarida and Williams and are mostly voting members whereas there is a likely a lot of non-voters in the five who see no change and the five who see a hike. So the dot plot is likely more dovish than it looks.

Our assessment remains that another 0.25% easing is likely, probably in October or if not then in December. The risks to the growth outlook – particularly on trade - won’t go away quickly and that the Fed appears to have taken the decision that it’s easier to control a rise in inflation than a further slide or deflation.

Fed Chair Powell did not seem too concerned about liquidity stresses in the US money market (which look related to corporate tax payments, higher budget deficits and the impact of quantitative tightening) but he did indicated that the Fed may need to resume allowing its balance sheet to grow with the economy. This is not quite QE and its much smaller but it would ease liquidity stresses. In the meantime the New York Fed is continuing to address the issue by injecting funds into the money market (via repurchase operations).

Interestingly Fed Chair Powell said that if the Fed Funds rate does have to go back to zero, that would be the lower bound. In other words the Fed would not take rates negative.

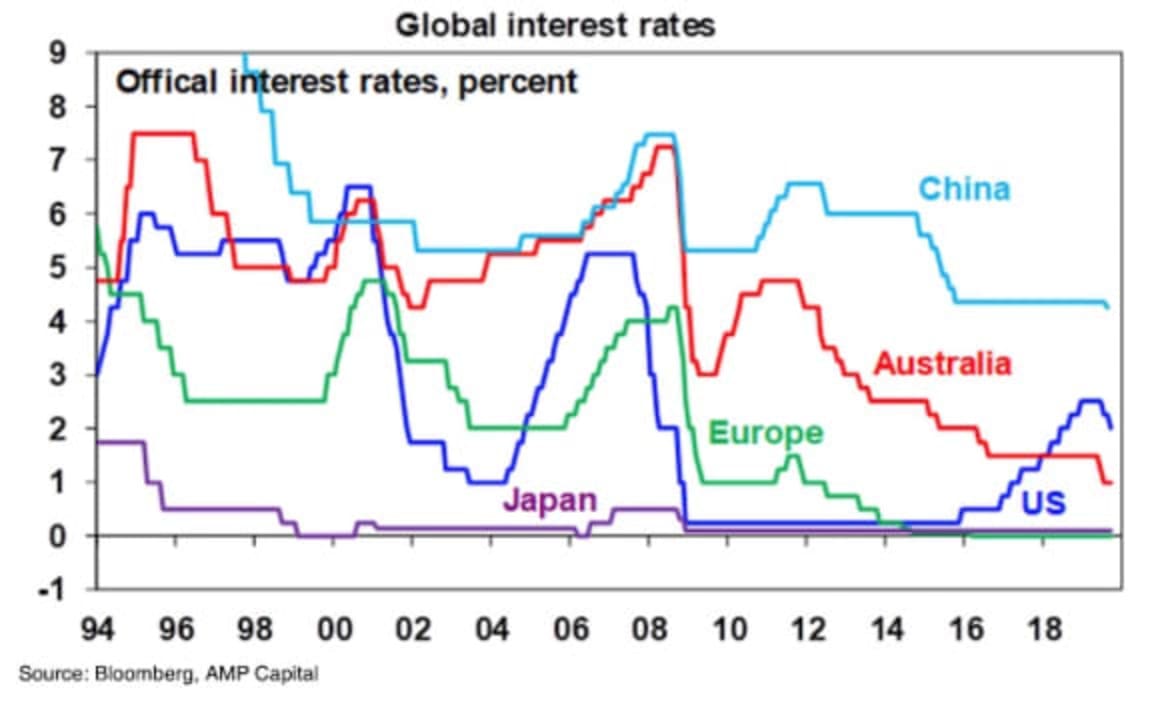

The directional relationship between US and Australian interest rates weakened long ago. The RBA started raising rates in 2009 when the Fed held at zero, it was easing in 2016 when the Fed was hiking and this year it started cutting ahead of the Fed. See the next chart.

So just because the Fed moves doesn’t mean the RBA will too. On the one hand the Fed’s easing along with stimulus elsewhere globally should help support global growth which is good for Australia. But it’s probably not enough to change the outlook for the RBA and its perception that global risks have increased. . Our view remains that it’s on track to cut the cash rate to 0.5% in the months ahead in two 0.25% moves and to some degree the Fed cutting and the ECB easing last week reinforces that to the extent that the RBA would like to keep the Australian dollar down.

Falling interest rates are generally positive for shares, unless there is a global recession. While the risk of recession has gone up thanks to the trade war and conflict in the Middle East we remain of the view that it will be avoided.

DR SHANE OLIVER is Head of Investment Strategy and Chief Economist AMP Capital.