Has the interest-only cliff almost been negotiated? Pete Wargent

Pete WargentDecember 17, 2020

EXPERT OBSERVER

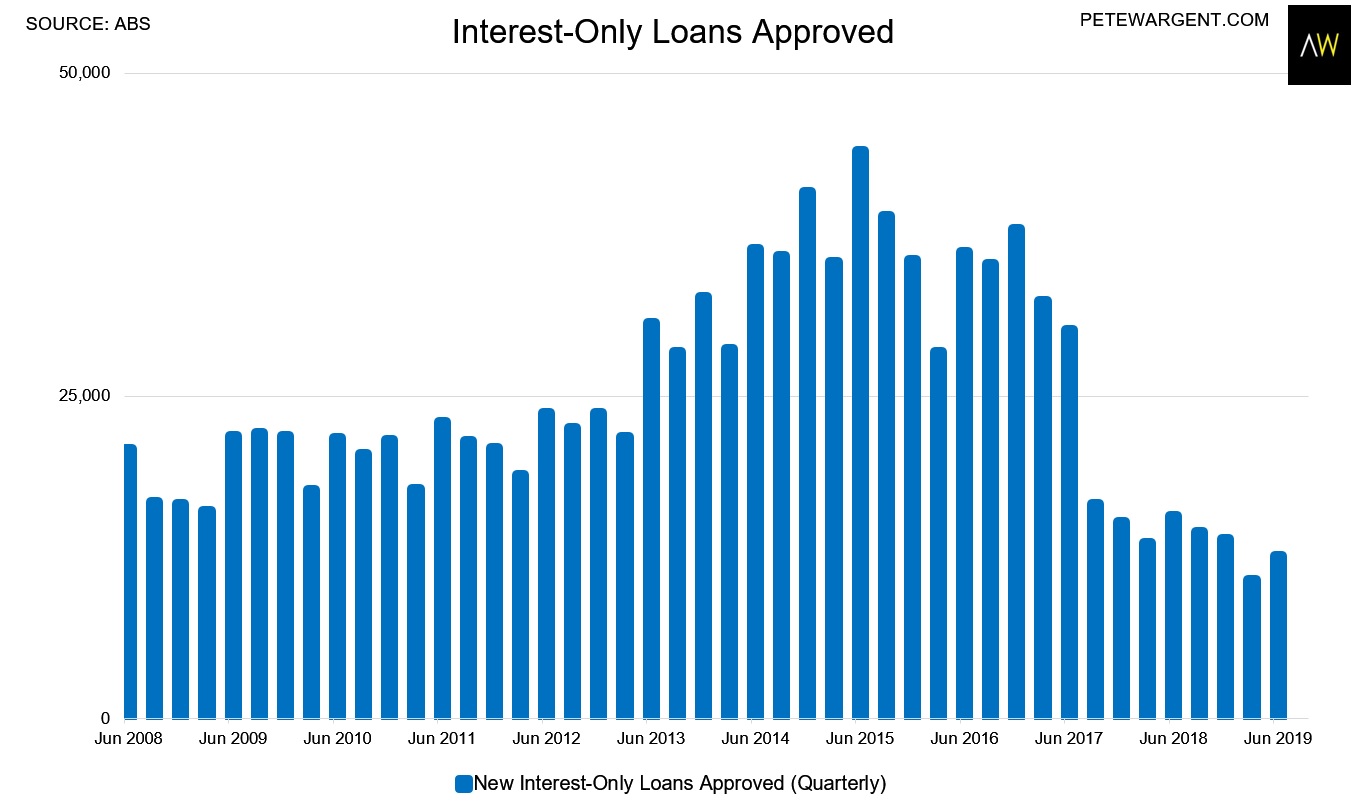

Some blessed relief for housing investors as the number of interest-only loans was finally off the lows in the June 2019 quarter.

Following changes to serviceability rules further increases should hopefully be observed in the second half of 2019.

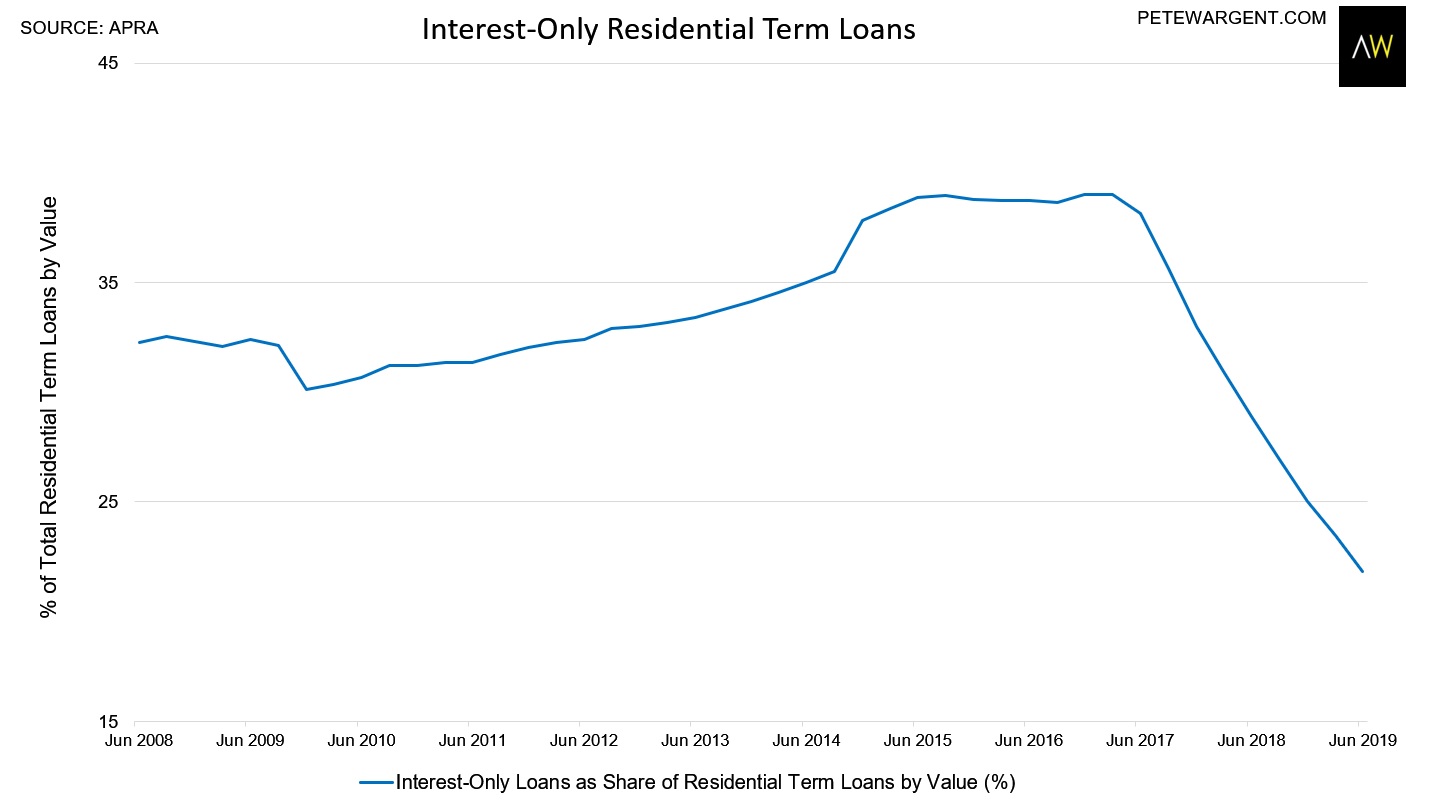

The stock of interest-only loans continued to decline sharply to 21.8 per cent of total mortgages, however - comfortably the lowest share on record - having been at 39 per cent of the stock of outstanding mortgages by value as recently as early 2017.

This shows how dramatically effective the interest rate differential was in lending and borrowing behaviours, alongside caps and certain other restrictions.

Despite all the hype, there have been comparatively few signs of forced selling to date, with most borrowers managing the transition comfortably.

In fact, new stock listings have remained exceptionally low.

There has been an impact on consumption, though, and NAB now forecasts three further interest rate cuts over the next nine months, as indeed does ANZ.

In fact, NAB also sees a chance of unconventional measures on top of these cuts.

In fact, NAB also sees a chance of unconventional measures on top of these cuts.

Of the remaining interest-only loans Westpac retains the largest stock.

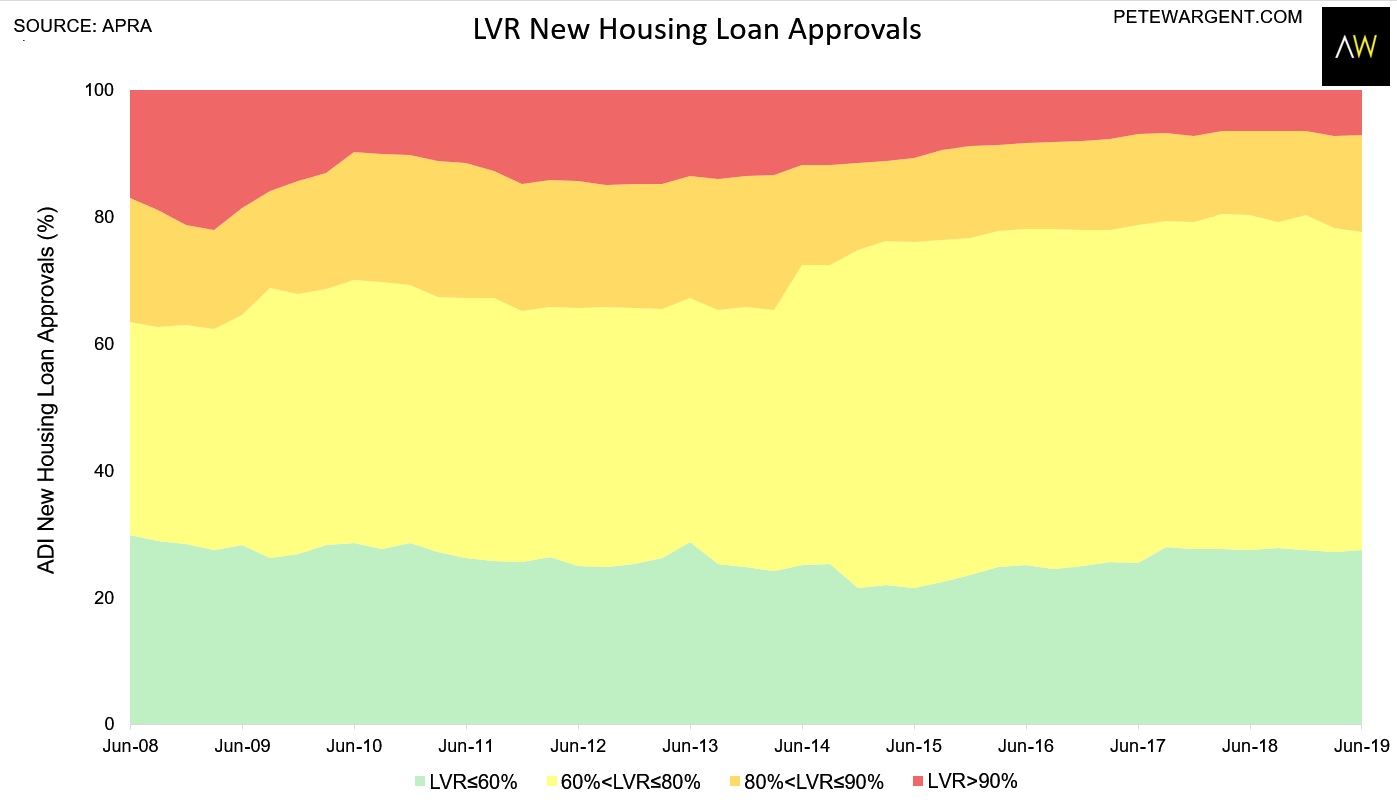

Finally, the 5-year squeeze on higher-LVR lending has finally eased a little, with the majors steadily writing more loans at 80-90 per cent LVRs, which is also a relief to see.

Non-banks wrote a fair chunk of the loans at above 90 per cent LVRs, but there have been fewer exceptions reported as a share of total lending.

Brink of crisis

Overall, there are some tentative signs that banks are somewhat more willing and able to write mortgages, half a decade after the prudential tightening began.

Investment lending is now only about half of what it was at the peak, and some loosening is welcomed to allow first homebuyers an opportunity to buy, with prices also lower over the past two years.

Moreover, the banking Royal Commission brought Australia to the brink of a recession and a related banking crisis.

At the last count monthly building approvals have crashed to 12,944 (with unit approvals down 44 per cent year-on-year), which is a diabolical leading indicator for activity in the economy, while credit growth is also dreadfully weak.

Despite these atrocious numbers, there's often a palpable complacency evident in the housing market commentary.

A banking crisis can still be averted, but only if banks can get some credit flowing again...and soon.

Investment lending is now only about half of what it was at the peak, and some loosening is welcomed to allow first homebuyers an opportunity to buy, with prices also lower over the past two years.

Moreover, the banking Royal Commission brought Australia to the brink of a recession and a related banking crisis.

At the last count monthly building approvals have crashed to 12,944 (with unit approvals down 44 per cent year-on-year), which is a diabolical leading indicator for activity in the economy, while credit growth is also dreadfully weak.

Despite these atrocious numbers, there's often a palpable complacency evident in the housing market commentary.

A banking crisis can still be averted, but only if banks can get some credit flowing again...and soon.

Pete Wargent

Pete Wargent is the co-founder of BuyersBuyers.com.au, offering affordable homebuying assistance to all Australians, and a best-selling author and blogger.