Lenders continue to reduce the risks in their mortgage books

EXPERT OBSERVER

The latest data from the Australian Prudential Regulation Authority (APRA) on property exposures data from authorised deposit-taking institutions (ADIs) shows that the tougher lending policies of recent years continue to reduce mortgage risks.

Over the March 2019 quarter, APRA reports that there was $72.395 billion in residential mortgages to households, which was -17.9% lower than the previous quarter and down -16.5% on the March 2018 quarter.

As the chart shows the value of lending to investors and owner-occupiers is falling.

Over the quarter the value of lending to owner-occupiers was -17.6% lower and it was down -15.2% year-on-year. Lending to investors was -18.7% lower over the quarter and -19.6% lower year-on-year.

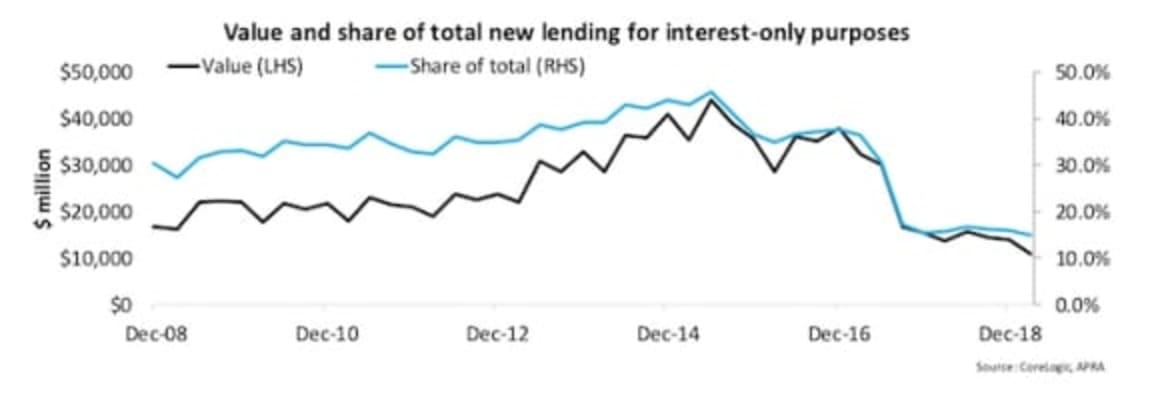

The heightened level of interest-only lending has been seen as a key risk in the market and new interest- only lending has fallen over the quarter both on a value and share of total basis.

Over the quarter there was $10.785 billion in interest-only lending which was the lowest on record.

As a share of total lending, interest-only was also at a record low of 14.9% which is a far cry from its peak at 45.6% in June 2015.

As a proportion of the total portfolio of outstanding loans, interest-only now accounts for a record low 23.3% which is down from a peak of 39.5% in June and September 2015.

Interest-only lending isn’t the only area in which there has been a reduction riskier lending. The value of low documentation loans, other non-standard loans and loans approved outside of serviceability all fell over the quarter in terms of both value and their share of total lending.

In fact at 0.1% of total lending over the quarter, both other non-standard loans and low documentation loans were at an historic low share of mortgages while the 4.3% of loans that were approved outside of serviceability was the lowest share since December 2017.

While most areas of riskier lending recorded a reduction over the quarter, there was a slight increase in the share of new mortgages written with a loan to value ratio (LVR) of more than 80%. Over the quarter there was $15.772 billion worth of new mortgages with an LVR of more than 80%.

Although that was the lowest value on record, that is more a function of reduced overall demand for mortgages. The share of mortgages with an LVR in excess of 80% was recorded at 21.8% over the quarter which was its highest share since March 2017. The share of higher LVR loans is still well below its peak of 37.6% in March 2009 and most new borrowers have more than 20% equity in the property they are purchasing.

Nevertheless, it is a little surprising that given the current tight credit conditions and falling dwelling values that there is an increased willingness to lend to borrowers with less than a 20% deposit.

Overall, the data reflects the ongoing improvements in mortgage quality and the shift towards reducing the build-up of risk in the mortgage market. We would expect the current conditions to continue over the next quarter. Thereafter it will be interesting to see what happens given that there has been an interest rate cut and it looks as if APRA will be relaxing some of the serviceability limits in place on mortgages.

On the other side of things, comprehensive credit reporting is being implemented which is likely to mean even more scrutiny on borrowers debts and subsequently increased pressure on lenders to write high quality mortgages.

CAMERON KUSHER is the head of research for the Australian branch of CoreLogic

Kusher regularly posts on the CoreLogic website.