From strength to resilience: APRA chairman Wayne Byres

- it is strong – participants in the banking sector, and particularly the larger players, should have the capacity to endure plausibly foreseeable stress while continuing to meet the reasonable needs of the Australian community; and

- it is resilient - there are mechanisms in place, in the event one or more institutions are no longer viable, to facilitate their orderly resolution and ensure that continued access to critical functions, such as credit provision, is not materially impaired at a time when it is most needed.

Moving from strength to resilience

Achieving this objective will involve work in four broad areas, and take the next several years to fully implement:

- reinforcing capital strength;

- improving the stability of liquidity and funding profiles;

- enhancing both the public and private sectors’ readiness for adversity; and

- strengthening the risk culture within the financial system.

I’d like to briefly step through each of these issues in turn.

- Capital strength

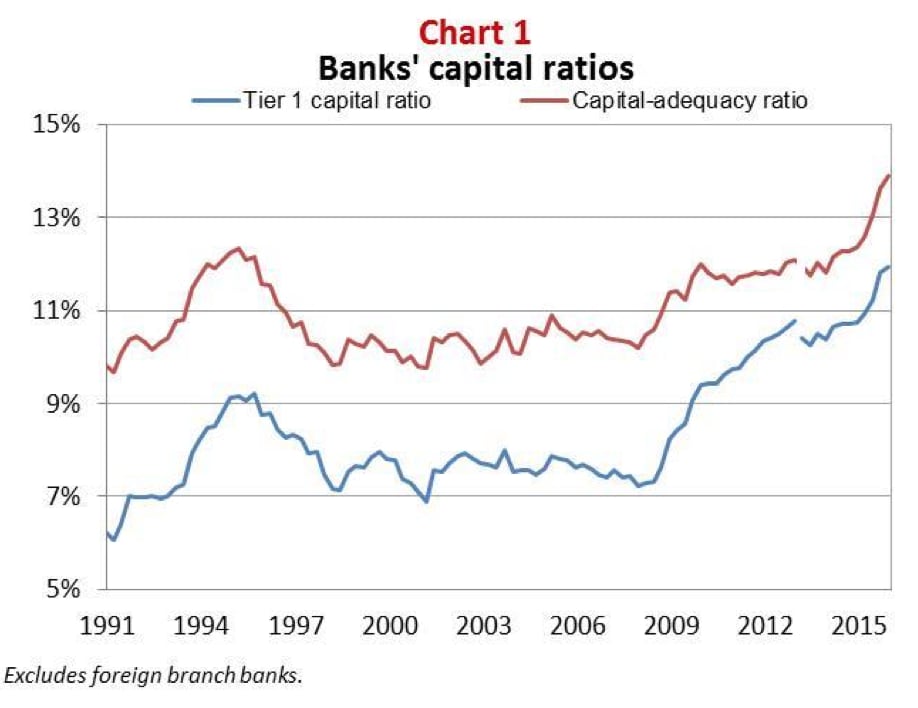

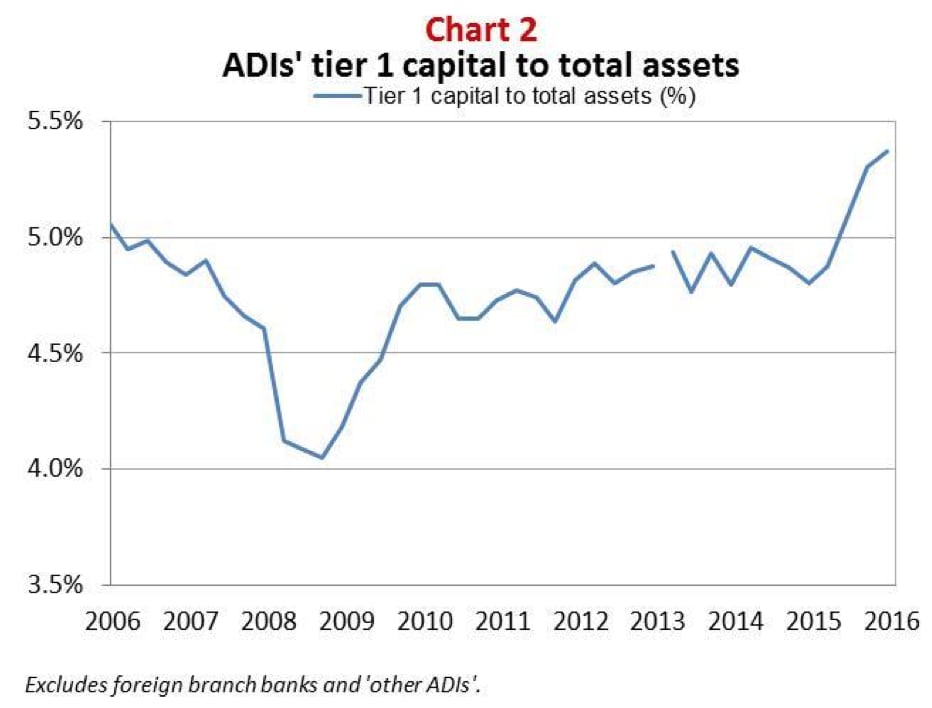

The capital strength of the banking system has attracted much attention during and since the FSI. I’m sure it was not accidental that the first recommendation of the Inquiry’s Final Report concerned the need for Australian ADIs’ capital ratios to be seen as ‘unquestionably strong’: given our bank-dominated financial system, the soundness of the banking sector is critical to ongoing economic prosperity.

However, as Bill Coen’s remarks on the Basel Committee’s work programme have made clear, there are a large number of important components of the bank capital regime that are still being debated in international fora. As a result, our consideration of what constitutes ‘unquestionably strong’ in an Australian context will need to wait until around the end of the year.

The direction is pretty clear – no one should be planning for capital requirements to decline – but as Australian ADIs start with a relatively strong capital position, the actual implementation of any changes should be able to be managed in an orderly fashion. Broadly speaking, 2016 is the year for finalising the international framework, 2017 will be the year for consultation on its domestic application having regard to the FSI, and 2018 will be the year for implementation.

- Liquidity and funding profiles

A key rationale for the FSI’s ‘unquestionably strong’ recommendation was the banking system’s critical role intermediating between foreign lenders and domestic borrowers. As the financial crisis showed, the smooth functioning of the Australian financial system can be jeopardised when access to foreign funding is disrupted.

The FSI recognised that Australia, as a capital importing country, is unlikely to reduce its reliance on foreign funding any time soon, if ever. As a result, making sure international investors maintained their faith and confidence in the health of Australian banks – via ‘unquestionably strong’ capital ratios - was seen as critical to reducing the risk that access to foreign funding might become restricted.

But capital is not the only means by which this risk can be mitigated. Improving the stability of bank funding profiles also helps. As I noted a little earlier, the Net Stable Funding Ratio - which is designed to promote more stable sources of funding and discourage excessive reliance on short-term borrowing - will also help reduce the risks in the event of an abrupt constriction in access to international markets.

To be clear, the NSFR doesn’t completely remove the risk, but to the extent we can do more to reduce our exposure to sources of funding that can evaporate at the first sign of trouble, the banking system will have more time in which to respond and adjust.

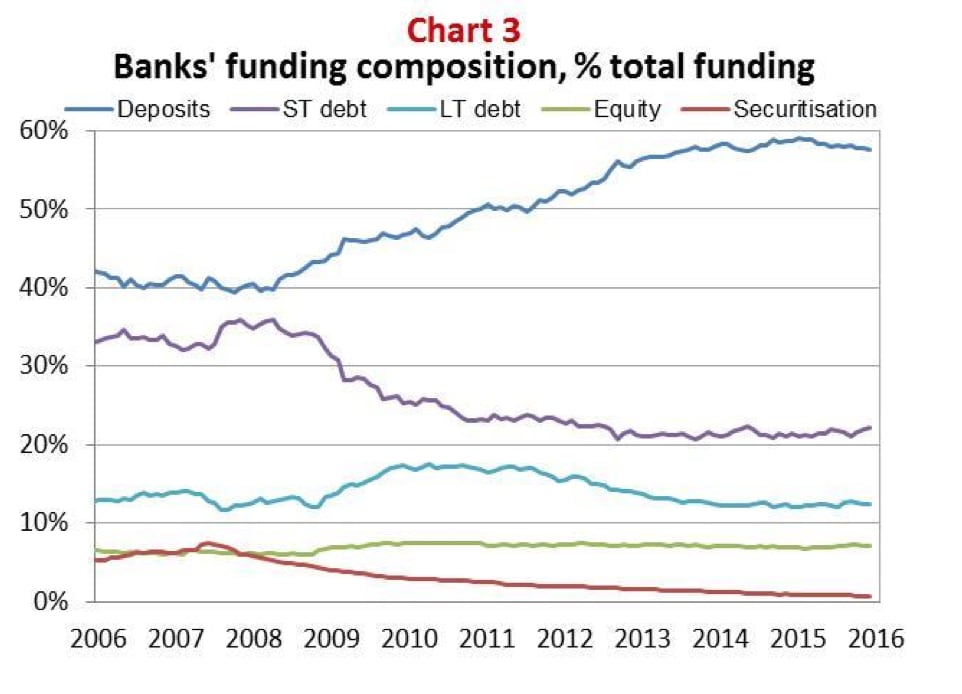

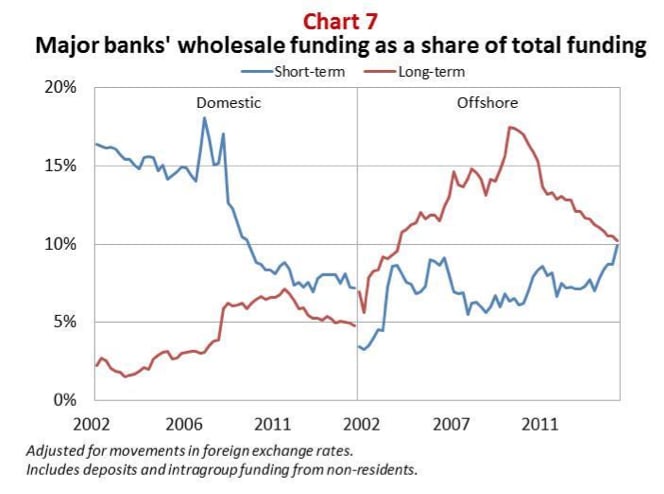

Notwithstanding my earlier comments regarding the positive changes in the post-crisis period, if you look a little deeper there is still room for improvement in funding profiles. While overall wholesale funding has declined as deposit funding has increased, term funding has contracted, and to the extent short-term wholesale funding has also reduced, it has been from domestic, rather than offshore, markets (Chart 7). Looking at whether we can do more to build domestic wholesale capacity, and generally lengthen tenors, will be an important area of attention over the next few years.

- Readiness for adversity

The strengthening I’ve talked about thus far will help reduce the probability that financial firms will reach the point of failure, but there can be no guarantees. Another integral part of improving resilience is to be better prepared for the next crisis, whenever it might arrive.

I’ll highlight three particular work streams here. The first two - enhancing APRA’s crisis management powers, and improving recovery and resolution planning – deliver important benefits with limited cost. The third work stream - developing a framework for loss absorbing and recapitalisation capacity - will need careful consideration to ensure it delivers the requisite benefits to system resilience at an appropriate cost and without unintended consequences.

APRA’s current crisis management powers are a vital, albeit often overlooked, component of the prudential framework. The Financial Stability Board’s (FSB’s) Key Attributes of Effective Resolution Regimes (Key Attributes) provide the relevant international standard in this area: as noted in the FSI’s Final Report and the FSB’s recent peer review, there are some gaps and deficiencies in the Australian resolution framework when compared with the Key Attributes. We were therefore pleased to see the Government, in its response to the FSI, endorse improvements to APRA’s crisis management powers as a matter of priority.

The Key Attributes also require jurisdictions to put in place recovery and resolution plans for relevant firms. On recovery planning, APRA is working with larger ADIs (and in due course other relevant firms) to ensure they have plans that are credible – that is, a realistic and continuously reviewed menu of actions that can be practically implemented in stressed operating conditions. On resolution planning, we are reviewing our own capabilities to ensure that we are able to use our (hopefully enhanced) resolution powers effectively when needed. Resolution plans are the responsibility of regulators, but require the input of the relevant institutions and, potentially, consideration of pre-positioning measures that could help to improve resolvability.

The third workstream in this area is the FSI’s recommendation that Australia ‘implement a framework for minimum loss absorbing and recapitalisation capacity in line with emerging international practice, sufficient to facilitate the orderly resolution of Australian authorised deposit-taking institutions and minimise taxpayer support.’1 The Government’s response to the FSI report endorsed APRA to implement this recommendation, but wisely didn’t impose a firm deadline, simply noting that it would be work that extended beyond 2016.

International thinking in this area has been led by the FSB, which will require globally-systemically important banks (G-SIBs) to have a minimum amount of total loss absorbing capacity (TLAC) over and above their minimum capital requirements. Although Australian banks haven’t been designated as G-SIBs, the basic objective of facilitating orderly resolution and minimising the risk of taxpayer support is the same as that which led to the FSI’s recommendation.

The range of approaches emerging internationally to implement the TLAC standard, and the market’s perception of these different approaches, highlight how important it will be to consider the costs and benefits in an Australian context.

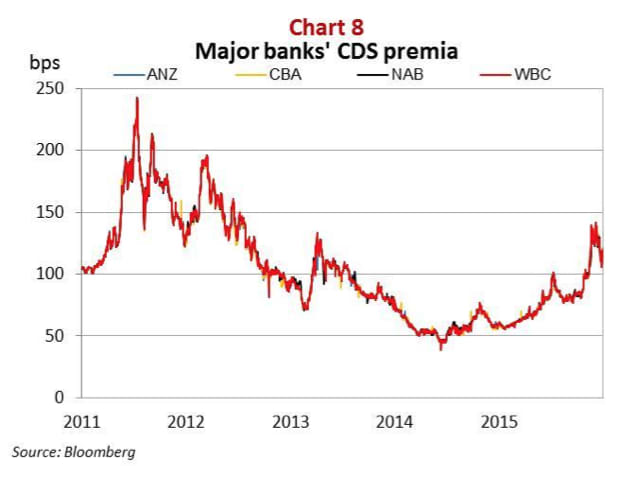

Given global developments, we will have the benefit of observing a variety of approaches as we progress our work. However, one issue we will need to bear in mind is that, when it comes to the provision of credit in Australia, the regulated sector dominates the unregulated sector. Within that, banks dominate the regulated sector. And the four major banks dominate the banking sector. They are also highly correlated.

For that reason, the rest of the world often sees Australian banks as peas in a pod: for example, you have to look very closely at this chart to notice there are four lines on it (Chart 8). So probably more so than in other jurisdictions, it will be necessary to design Australian arrangements with the idea of systemic, as much as idiosyncratic, problems in mind.

I’ve noted elsewhere that we will take advantage of our lack of fixed deadline and hasten slowly. I do want to stress that that is not to say we regard the issue is unimportant - quite the contrary. Moving forward on this issue will not only bolster the resilience of the system and minimise potential taxpayer support in times of stress, but help the competitive landscape by reducing the implicit subsidies that come from perceptions of ‘too big to fail’ and the associated reduction in market discipline.

- Risk Culture

Finally, it would seem no regulatory speech these days is complete without a few words on the issue of culture. Regulators have variously been accused of being on a culture crusade, and wanting to be the culture police. That’s not the case: indeed, regulators are really keen to see the industry lead the running on this issue. We need the financial sector to take up the challenge to put in place better incentives for prudent behaviour, so as to prevent problems emerging in the first place. That is likely to be far more productive than spending our time removing so-called ‘bad apples’ after the fact.

So while regulators have certainly put culture in the spotlight, it is the industry that needs to do something about it. There are good signs that is happening.

Our engagement with Boards has highlighted they are thinking about this issue more systematically, and I expect you’ll hear more about it later in today’s agenda.

And there are also industry-wide initiatives, like the Banking & Finance Oath and the associated Ethical Literacy Program, that complement the work in individual institutions. Balancing ethics, prudence, customer interests and shareholder needs in a commercial environment is a challenge that belongs to everyone in financial services. We’ve all got work to do to get the balance right, and the sins of the past continue to emerge, but at least the issue is starting to get the serious attention it deserves.

Concluding remarks

Australia has long benefited from a sound financial system, and the financial system has benefited from Australia’s long period of economic expansion. But we cannot be complacent about the risk of shocks to that prosperity. When those shocks arrive – as they inevitably will – we need to not only have a strong financial system, but one that is resilient in the face of adversity.

That requires not just sound governance and prudent balance sheet settings by financial institutions themselves, but also a regulatory architecture that allows for timely and effective intervention when needed. Achieving that will keep us all busy for a little while yet. But its better we invest in building resilience now, from a position of relative strength, than have to do so when circumstances are more difficult.

Wayne Byres is chairman, Australian Prudential Regulation Authority.