Arrears pain is dull but mortgage regulation is excruciating: Pete Wargent

Pete WargentDecember 7, 2020

Let's take a considered look at S&P's mortgage arrears.

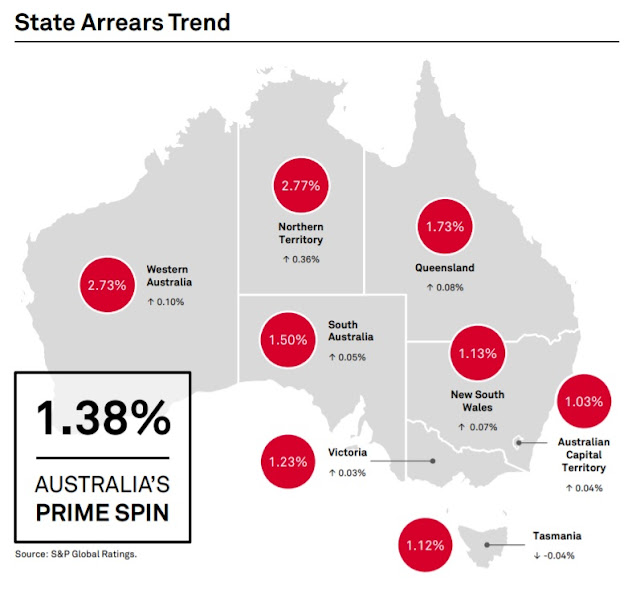

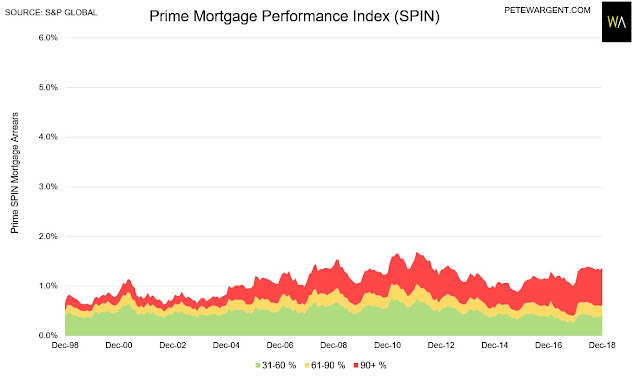

Basically unchanged throughout 2018 at 1.38% for 30+ day arrears.

90+ day arrears are now up a notch to 0.75%.

That's mainly related to major banks locking interest-only (IO) borrowers in as they roll over to P&I loans.

While this could be a drag on consumption most IO borrowers have buffers measured in years, and most didn't borrow anywhere near to their maximum capacity either.

I'd argue that most of the little mortgage stress that there is has been inflicted by excruciating mortgage regulation rather than rising unemployment, mortgage rates, or over-stretched borrowers.

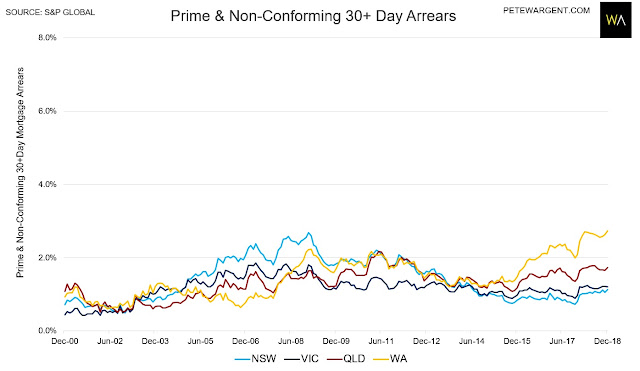

Weakness in Western Australia's economy is the other main contributory factor.

Weakness in Western Australia's economy is the other main contributory factor.

In fact, job vacancies are at record highs according to the ABS surveys, both in absolute terms and as a share of the labour force.

The unemployment rate is also at the lowest level in 6½ years at just 4.98%, while the respective unemployment rates in New South Wales and Victoria are actually the lowest on record.

The unemployment rate is also at the lowest level in 6½ years at just 4.98%, while the respective unemployment rates in New South Wales and Victoria are actually the lowest on record.

The main deterioration in arrears has clearly been in Western Australia, now at 2.73% for 30+ day arrears.

And non-confirming arrears remain close to their lowest ever level.

Unemployment is low, mortgage rates are low, and there are plenty of job openings.

Banks just need to lend on a more reasonable and timely basis.

Pete Wargent

Pete Wargent is the co-founder of BuyersBuyers.com.au, offering affordable homebuying assistance to all Australians, and a best-selling author and blogger.