40 percent of loan applications are being turned down as credit squeeze hits would be-borrowers

Digital Finance Analysts' Martin North has noted credit is harder to get.

The surveys conduction by DFA show that up to 40 percent of applications for mortgages are now being turned down, compared with just five percent a year ago, as lenders apply more forensic analysis of applications received.

This was triggering weaker conditions in Sydney and Melbourne.

He noted CBA is now looking at applications with a loan to income of 4.5 times and above.

"I am getting more reports of households who are finding their available borrowing power is as much as 35 percent down on a year ago."

So North suggests unlike the small correction which occurred to the CoreLogic Index in 2015, as credit was harder to get briefly, and which reverted a few months later, it would be "different this time."

He referred to the enhanced focus on mortgage lending serviceability means that a consideration of the loan to income ratio or LTI is ever more important.

In the UK, where LTI calculations are the norm, the Bank of England first introduced limits on high LTI mortgages in 2014.

These measures meant that no more than 15 per cent of mortgages issued should exceed a loan-to-income ratio of 4.5.

The UK’s 4.5 LTI cap on 85 per cent of new lending is still in place. In June last year, Bank of England governor Mark Carney announced that the 4.5 ratio “insurance measures” will become “structural features of the UK housing market.

"It should be of no surprise to note that the Commonwealth Bank of Australia has announced that it has brought in its new debt-to-income measurement for borrowers," North blogged.

CBA, who is the largest owner occupied mortgage lender in Australia has disclosed that it will now “monitor” loan applications with a debt-to-income ratio higher than 4.5 and will also bring in a new e-learning requirement for brokers that have not settled a CBA loan for more than a year.

Applications with a DTI higher than 7 will be subject to a manual credit approval check.

North estimates across the country around 7.9% of all loans have a current loan to income ratio of 6 times or more.

"But the prize goes to New South Wales with a massive 15.8% of households currently holding loans with a loan to income ratio of 6 or more. This is of course explained by the high prices, big mortgages, and lose lending standards," he says.

It is 7.1% of households in Victoria holding a loan to income ratio of 6 times or higher.

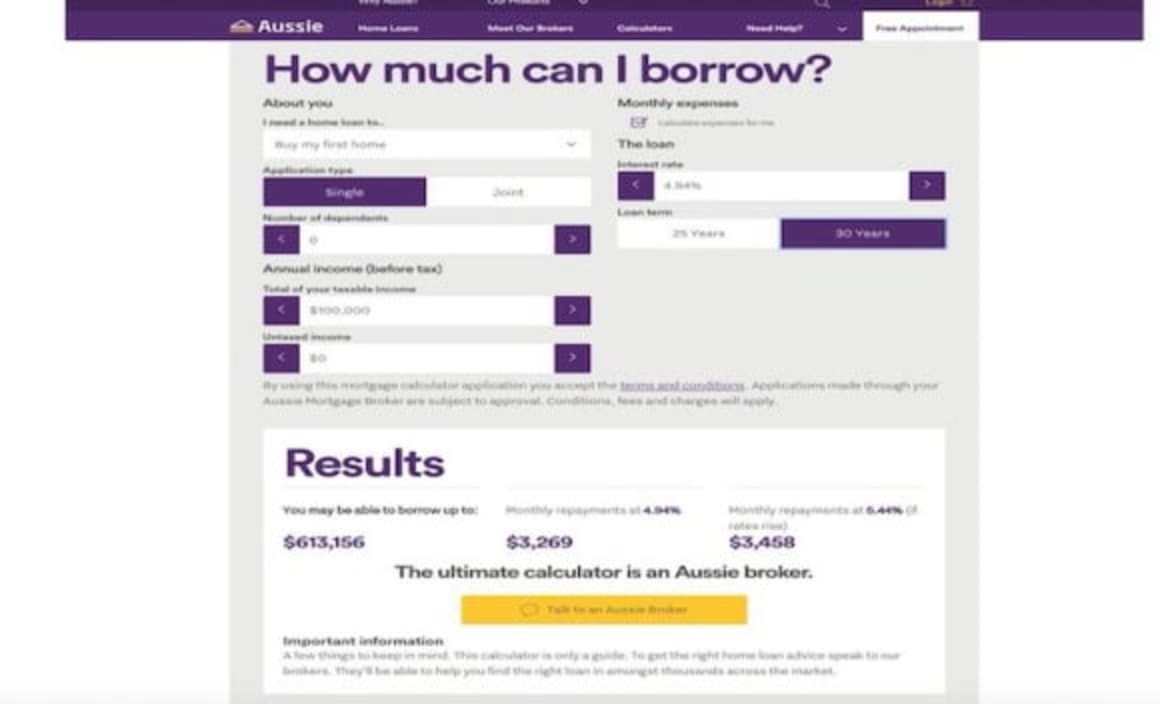

A recent borrowing sample was done by commentator Lindsay David at LF Economics on the Aussie Home Loan lending calculator site that showed how much the money on offer had dropped over recent years.

David's first image (below), is the figures of lending at an interest rate of 4.94 percent with a salary of $100,000 two years ago.

Aussie's online calculator advised it would be willing to lend up to nearly $825,000 two years ago.

Click here to enlarge.

Fast forward two years and the mortgage lending giant are willing to offer over $200,000 less to the same borrower type.

Click here to enlarge.

North looked at the RBA released their credit aggregates to April 2018.

He noted total mortgage lending rose $7.2 billion to $1.76 trillion, another record.

Within that, owner occupied loans rose $6.4 billion up 0.55%, and investment loans rose just 0.14% up $800 million.

Personal credit fell 0.3%, down $500 million and business lending rose $6.3 billion, up 0.69%.

The annualised stats show owner occupied lending is still running at 8%, while business lending is around 4% annualised, investment lending down to 2.3% and personal credit down 0.3%. On this basis, household debt is still rising.

But the Bank lending data from APRA showed that tighter lending standards are biting.

"In fact, Westpac apart, all the majors reduced their investor property lending in April," North noted.

Owner occupied loans grew by 0.29% or $3.1 billion to $1.07 trillion while investment loans fell slightly, down 0.01% or $42 million.

As a result, the relative share of investment loans fell to 34.14%.