NAB push back RBA cash rate hike forecast to mid 2019

The change reflects the fact there is no sign yet of stronger wages growth and unemployment has been stuck around 5.5% for the best part of a year.

We still expect the economy to strengthen, leading to a declining unemployment rate. This should eventually translate into stronger wages growth and give the RBA confidence that inflation will track back to its 2.5% target. However, we acknowledge there is considerable uncertainty around the timing at which wages growth will strengthen, and the time of the RBA’s next move will remain highly data dependent.

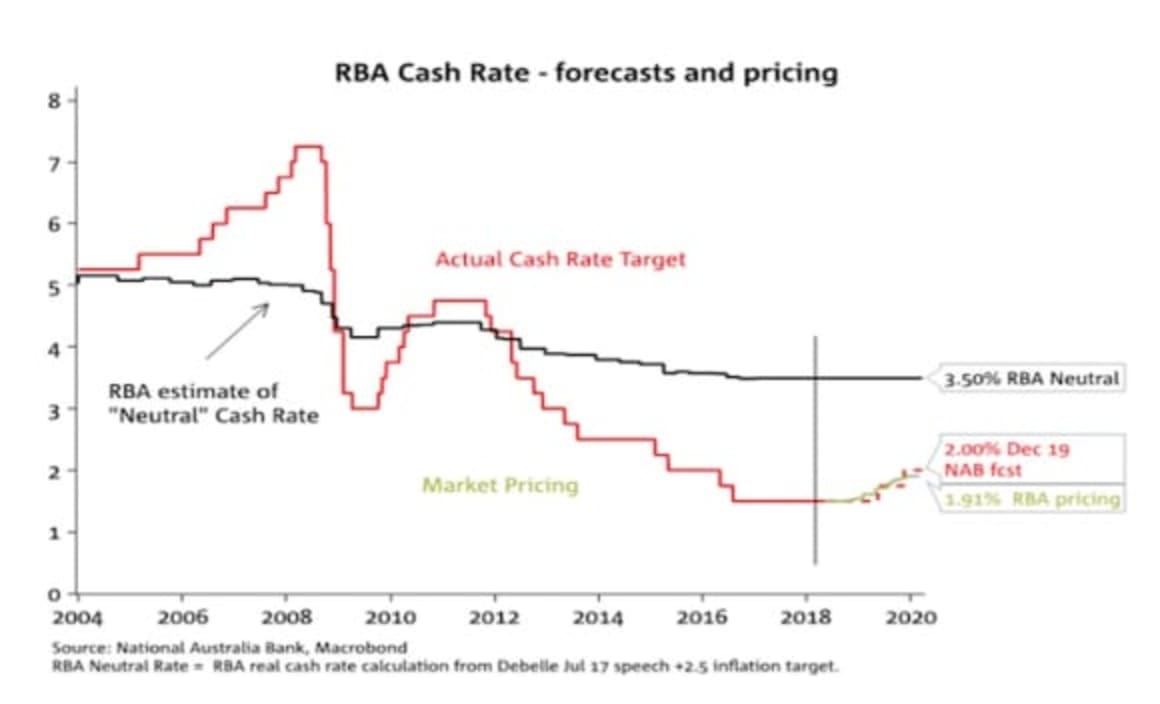

For some time NAB has been forecasting that if the economy were to improve as expected, then the RBA would at some point feel confident enough with the economic outlook to start the process of raising the cash rate from its current low level of 11⁄2%. In particular, our view has been that economic growth will strengthen over the coming year and that, with the pace of jobs growth already solid, this would lead to a declining unemployment rate and as a result upwards pressure on wages growth and inflation.

We still consider that this is the most likely trajectory for the economy and RBA policy. However, this week’s data on wages and the labour market indicate that November 2018, our previous forecast for the first rate rise, is too early and we now expect the RBA to be on hold through the rest of this year.

The unemployment rate ticked up 0.1ppt in April to 5.6%, and while the monthly data can bounce around, it adds to the evidence that progress in reducing the unemployment rate has stalled. The ABS measure of the trend unemployment rate has been at 5.5% since August last year; while jobs growth has been solid over this period, this has been offset by further increases in workforce participation. On the wages front, the Wage Price Index (WPI) for the March quarter 2018 was unchanged at 2.1% y/y, with private sector wages growth also unchanged at a slightly weaker 1.9% y/y and showing no signs of accelerating.

The RBA’s view on the outlook for the Australian economy is similar to NAB’s, in that it expects growth to strengthen, and for unemployment to decline leading to a pick-up in wages. The Bank continues to expect progress on unemployment, wages and inflation to be only gradual and has made clear that there is not a strong case for a near-term change in the cash rate. This week’s wage and unemployment data clearly will have done nothing to change this view. Quite reasonably, the RBA does not see 2% wages growth as consistent with 2.5% inflation over time and wants to see some pick-up in wages before lifting rates.

Click here to enlarge.

We still believe that conditions are in place for wages growth to rise in the future. Our modelling of factors that affect wages – inflation, labour market underutilisation, productivity and the terms of trade - suggest that we would already have expected to see stronger wages growth. Clearly this has not happened and may reflect the need for the unemployment rate to get closer to its long-term ‘neutral’ rate of 5% or lower, before sufficient wage pressures emerge. This has been the experience of other countries in recent years.

Click here to enlarge.

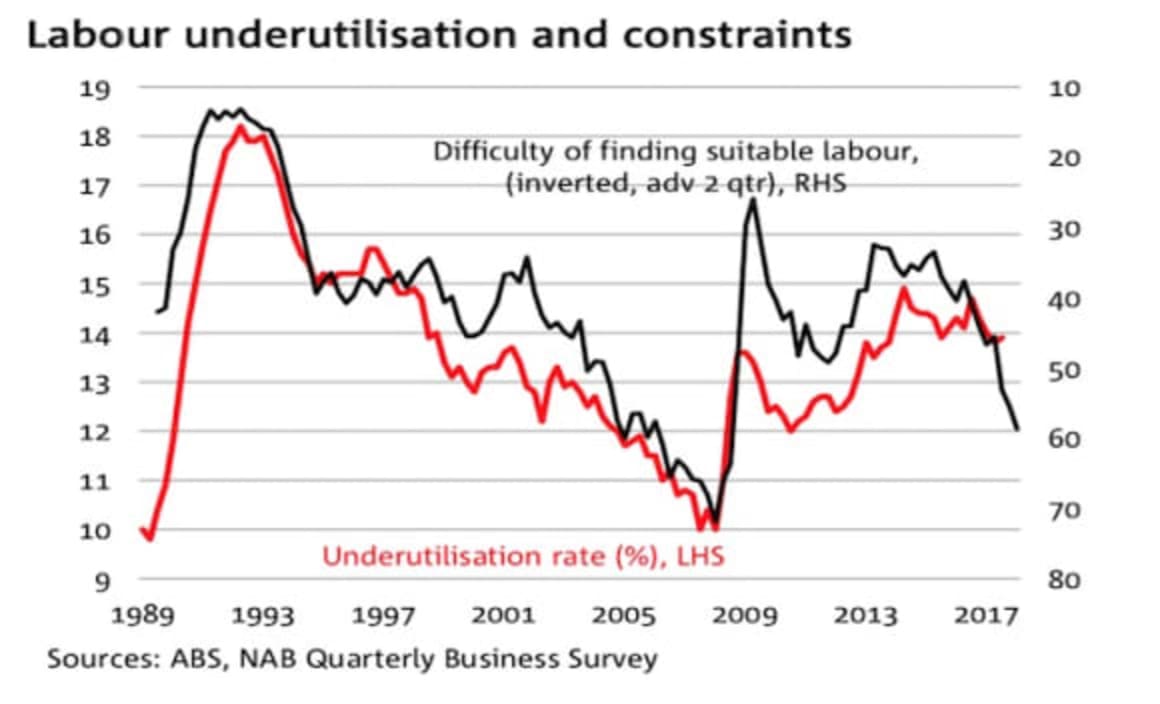

With the unemployment rate stuck around 5.5% recently, we now don’t expect the unemployment rate to get close to the 5% mark until mid-2019. That said, businesses continue to indicate – through our Quarterly Business Survey – that they are finding it increasingly difficult to find suitable labour; historically this has been associated with a decline in the unemployment rate, as well as the underutilisation rate and, ultimately, wages growth.

As a result our forecasts for WPI growth are more conservative than the model projections but we still expect to see some acceleration in wages growth. We are projecting that by mid-2019 WPI growth will reach the 21⁄2% y/y mark. At that time, with unemployment close to its full-employment level, growth above trend and wages growth gradually accelerating, we expect the RBA would have sufficient confidence that inflation will move back towards target and so start to gradually lift the cash rate off its current very low level.

We expect once the tightening cycle starts, further rate increases will be very gradual. We are now expecting the first move to be in mid (May) 2019, with the next move after that not until late in the year (November 2019).

Click here to enlarge.

However we acknowledge that there is considerable uncertainty around the timing of the RBA’s next move. The divergence of wages growth from what is suggested by the models makes this uncertainty greater than usual. The RBA will remain heavily data dependent and will want to see sustained signs of a pick-up in wages growth before moving, even if the rest of the economy moves in line with expectations.

Alan Oster is group chief economist, National Australia Bank, and can be contacted here.